Hydrogen: Decarbonization’s silver bullet?

Germany is aiming to push a European Union-wide policy on hydrogen. The key question is which methods of production will gain traction – and what the geopolitical implications will be if Europe becomes a net hydrogen importer.

In a nutshell

- Germany is pushing a hydrogen strategy for the EU

- Europeans favor “renewable” hydrogen production

- Other countries may gain an advantage using fossil fuels

After a delay of more than five months, at the beginning of June the German government adopted its long-debated national hydrogen strategy and is now determined to push this for the EU. The delay had been a result of several disputes, primarily pitting Germany’s economic and energy ministry against its environment ministry.

At the core of the disagreement was whether Germany should only support “green hydrogen” (primarily “renewable hydrogen”) or be technologically neutral. The latter would entail research, development and pilot projects for hydrogen technologies also based on fossil fuels.

For its new hydrogen strategy, Berlin will provide 9 billion euros of funding for green hydrogen projects. The money will come from Germany’s 160 billion-euro Covid-19 economic recovery plan. The government hopes to make the country the world’s leading supplier of state-of-the-art hydrogen technology.

Facts & figures

Hydrogen push

The German government also plans to use its EU presidency, which began on July 1, to develop an ambitious hydrogen strategy for the entire bloc as part of several EU-wide initiatives. These include the European Green Deal, the new Industrial Strategy and its new Climate Law (both unveiled in March 2020), as well as the newly codified target for reducing CO2 emissions by 50-55 percent (instead of the previously envisioned 40 percent) by 2030.

Other EU member states, such as the Netherlands, Portugal and Austria, have also pushed forward with national hydrogen projects. Currently, hydrogen accounts for just 1 percent of EU energy consumption. The European Commission is considering including hydrogen as a central element in its energy system integration strategy. It has already announced that it aims to scale up clean hydrogen production to 1 million tons per year with support from its Innovation Fund and other programs, as part of its next trillion-euro budget for 2021-2027.

Facts & figures

Germany’s hydrogen strategy

- Total funding: 9 billion euros

- For domestic projects: 7 billion euros

- Projects in partner countries: 2 billion euros

- The plan covers the full hydrogen value chain, supporting the automobile, steel, power and agriculture sectors

- 38 concrete measures to support implementation

- Total hydrogen production in 2015: 57 TWh from oil (45%), gas (33%), coal (15%), electrolysis (7%)

- Goal for total hydrogen production by 2050: 2,500 TWh (Germany’s total final electric and non-electric energy consumption in 2018). That is, five times Germany’s entire electricity production in 2019 (511 TWh). The chemical sector alone accounts for some 600 TWh of hydrogen demand

- Expanding green hydrogen production (via electrolysis) to 5 gigawatts (GW) by 2030, 10 GW by 2035 and 15 GW by 2040

- German power company RWE and steelmaker ThyssenKrupp agreed to produce 50,000 tons of steel from green hydrogen

The Commission has also introduced a “carbon contracts for difference” pilot program. The initiative will pay renewable hydrogen producers the difference between the price of carbon permits in the EU Emissions Trading System and a predetermined amount, with the hopes of encouraging investment in such technologies. The EU hopes that a green hydrogen economy could create 1 million new jobs for highly qualified personnel in the EU by 2030 and up to 5.4 million by 2050 across the entire value chain. The Commission’s “Clean Hydrogen Alliance” is expected to be launched next summer.

Experts see hydrogen as a clean, secure, affordable energy carrier, like electricity – it is not an energy source. It is also an industrial raw material that can play a key role in future decarbonized energy systems. Over the last two years, hydrogen has quickly gained political and industry support around the world.

Storage problem

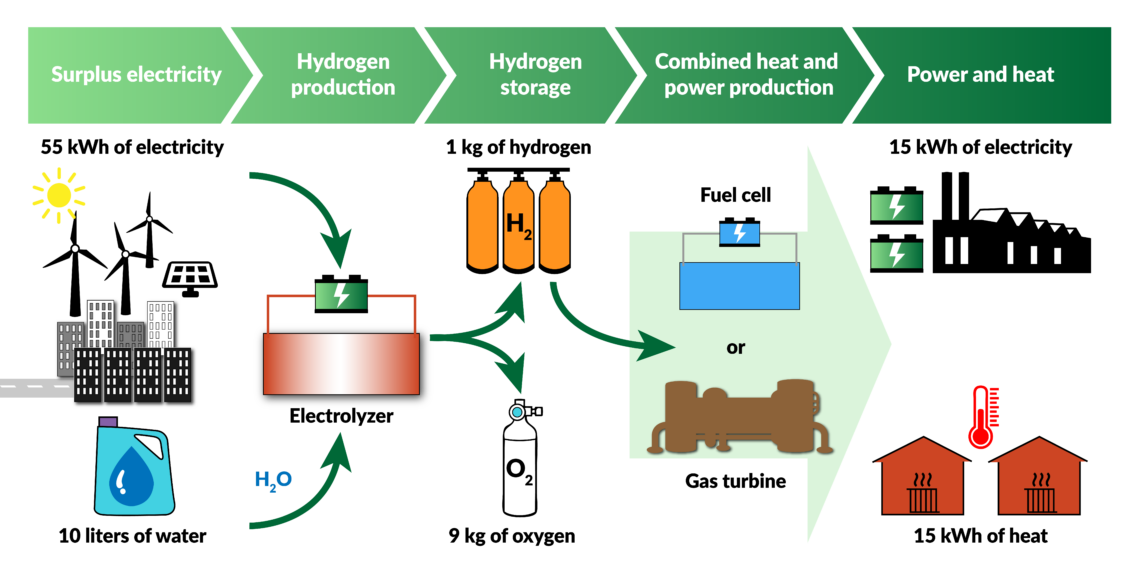

The German “Energiewende” (energy transformation) and other energy-transition programs have focused on generation but have not solved the challenge of storage for energy-intensive sectors like chemical, steel, iron and paper production, and long-haul transport. Existing technologies for storing hydrogen show promise, though. For now, hydrogen is the leading and currently only realistic option for long-term storage of renewable energy.

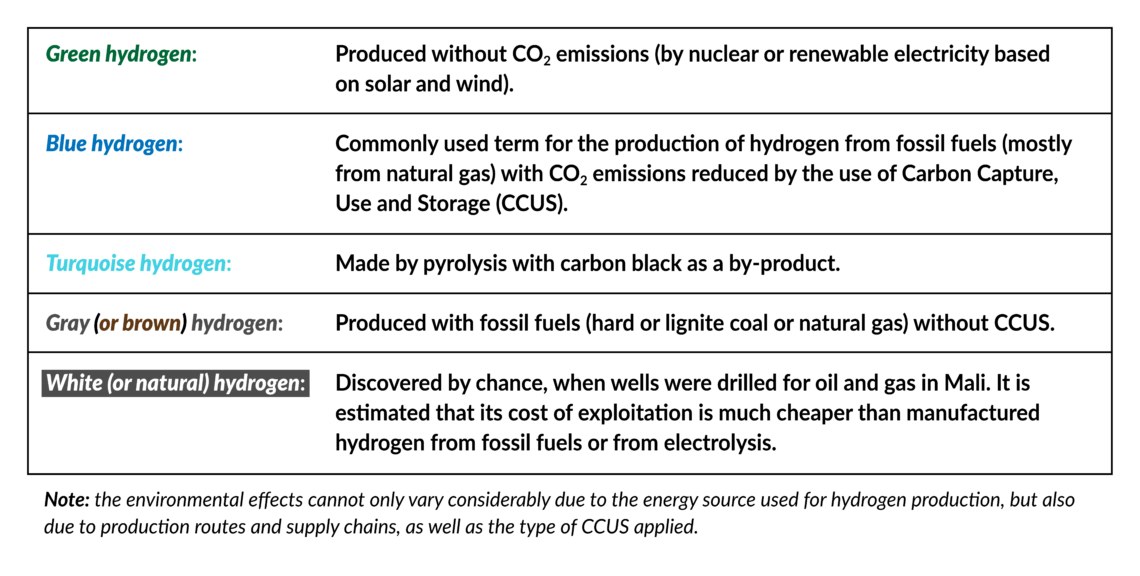

In the short term, blue (natural gas) and gray (fossil fuel) hydrogen could remain the most cost-competitive options for many countries (including China, India and parts of Southeast Asia) with larger coal and gas reserves, and cheaper production costs. At present, green (renewable) hydrogen is two to three times more costly than fossil fuel-based hydrogen. About 6 percent of global natural gas consumption accounts for some three-quarters of global hydrogen production – 70 million tons, or 205 billion cubic meters (bcm), per year.

Facts & figures

Coal currently accounts for 23 percent of global hydrogen production, or 107 million tons (from 2 percent of global coal consumption). Only 4 percent of hydrogen production in 2018 was based on renewable energy sources (RES). Producing hydrogen from electrolysis is extremely energy intensive. It would take some 3,600 terawatt-hours (TWh) – more than the EU generates in a year – to produce all the world’s hydrogen.

Hydrogen can also be transported as a gas (synthetic methane) by pipeline or in liquid forms by ship (as liquefied natural gas, or LNG). After being produced, it can be transformed into electricity and methane to power homes and industries, and into synthetic fuels such as methanol, diesel, gasoline, kerosene and jet fuel. With the costs of renewable energy rapidly declining and the development of new, innovative technologies, hydrogen has now become a real option for decarbonizing the areas of the economy that are hardest to wean off fossil fuels.

Four challenges

Since 1975, global hydrogen production has increased threefold, to 70 million tons (mt) per year or 330 mt of oil equivalent – more than Germany’s primary energy demand. Despite the growth, however, it still faces major challenges.

The first such challenge is energy efficiency. Producing hydrogen is still energy-intensive – particularly with costly renewable energy. An International Energy Agency analysis concluded that the cost to produce it could fall some 30 percent by 2030 thanks to the mass manufacture of fuel cells, refueling equipment and electrolyzers.

Most applications for low-carbon hydrogen are not cost-effective without direct government subsidies, however. Significant technological innovations, improvement of energy efficiency and other performance factors will therefore be needed and will require much more international cooperation.

The present policies do not support the growth of a clean hydrogen industry, and often constrain larger investments.

Energy efficiency is particularly difficult to achieve. Using more electricity to convert hydrogen into synthetic fuels and feedstocks exacerbates the problem. Some 45-60 percent of the electricity used to produce hydrogen is lost in the process. Likewise, the process of converting electricity into hydrogen for storage and shipping, and then converting it back to electricity in a fuel cell, can be highly inefficient. In some cases, the energy delivered falls below 30 percent of the initial electricity input.

The next challenge is the future of Carbon Capture, Utilization and Storage (CCUS). At present, the vast majority of hydrogen is produced using natural gas and coal. That accounts for 830 million tons of CO2 emissions worldwide. To keep it from adding significantly to climate change, fossil fuel-based hydrogen production is therefore only realistic with the use of CCUS – resulting in what is termed “blue hydrogen.” Yet in Germany and several other EU member states, the option is stalled as public has been reluctant to accept the use of CCUS, even though the technology had previously received government support.

Facts & figures

The third challenge is developing hydrogen infrastructure, such as refueling stations, which requires national or regional master plans for cooperation and coordination between industry, investors and governments. Here, Europe can benefit from its existing natural gas networks. In Germany, for example, only 100 km of the planned 1,200-kilometer hydrogen-transport pipeline network needs to be newly built. For the remainder, existing pipelines only have to be converted. Over longer distances – more than 1,500 kilometers – shipping is the more cost-efficient option. Currently, however, there are no liquefied hydrogen ships in operation.

The final challenge is hydrogen regulations. The present policies do not support the growth of a clean hydrogen industry, and often constrain larger investments. International standards for large-volume storage, environmental protection and transportation of hydrogen must be quickly developed and harmonized.

Geopolitical dimensions

Facts & figures

Global moves toward hydrogen

- 18 economies, comprising more than 75 percent of global GDP are implementing hydrogen strategies

- Some EU member states, as well as South Korea, Japan and others have included support for hydrogen in their post-Covid recovery programs

- The EU is expected to invest 300 billion euros over the next decade to meet its new climate goals

According to various forecasts, green hydrogen could capture up to 14 percent of the global energy market. This is the most expensive production method and currently accounts for less than 3 percent of global hydrogen output. A worldwide shift to hydrogen in the international energy system would inevitably produce new geopolitical winners and losers.

The German government knows that it will not be able to produce all the electricity it needs for the renewable hydrogen economy it envisions. With its high population density, Germany does not have the space to expand its renewable-based electricity production. So while making the switch to hydrogen could reduce the country’s dependence on natural gas imports, the EU will also become more dependent on hydrogen imports for its strategy.

The EU as a whole will likely become dependent on hydrogen imports for its strategy.

For that reason, Berlin is supporting the EU hydrogen strategy and various European hydrogen projects. Nevertheless, the EU as a whole will likely become dependent on hydrogen imports. Brussels and Berlin will have to consider the new energy security risks and vulnerabilities that will come with the move toward hydrogen. They will have to find ways to diversify import sources, making hydrogen partnerships with various players around the world.

Scenarios

For now, the cost of fuel for producing hydrogen is the biggest factor in the process, accounting for 45 to 75 percent of the final production cost. Countries with low gas prices therefore, like Russia, the United States and those in the Middle East, could be winners. Countries with higher gas prices – often those that must import LNG – like Japan, China, India and South Korea, could lose out. Yet this scenario hinges on several factors, like political support for hydrogen projects and a decline in overall costs on the back of technological innovation.

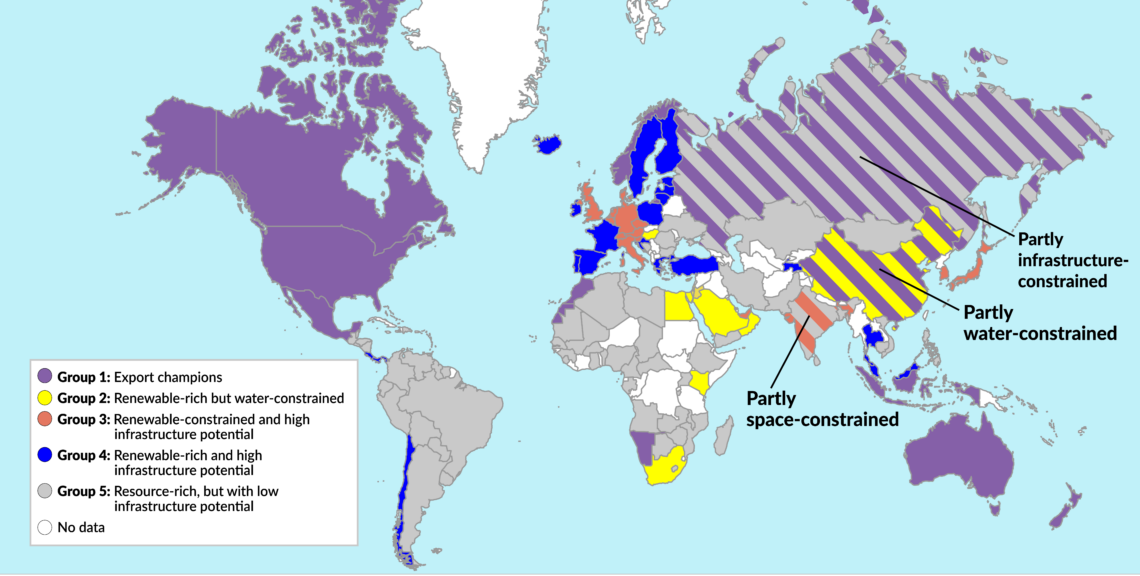

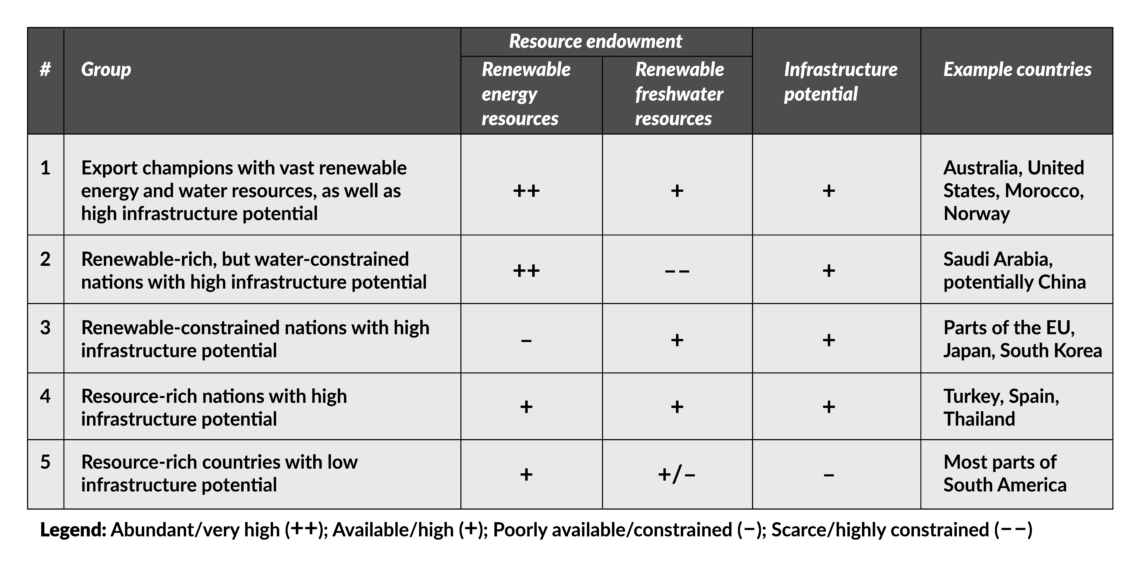

The prospects could look much different if hydrogen production is mainly based on renewable energy sources. Russia, for example, does not have the abundance of solar and wind power potential that the Middle East, Africa and Australia do. But whether renewable hydrogen will be concentrated in various regions (like today’s gas market) or more decentralized (as with renewable energy sources) depends on technology, infrastructure, market structures and political support.

The electrolysis process requires a sufficient supply of water and electricity. If it is based on renewable energy, population density (as in major European countries like Germany) could play a constraining role. Many places in Africa, the Middle East, South America and Asia (including parts of China) will not have enough water.

Other countries may have the ability and space to produce renewable energy, and the water for electrolysis, but may find themselves unable to build the infrastructure to produce, transmit and distribute that energy. The larger the country, the more expensive it is to build such infrastructure. Here, Russia and India are examples of countries that could be at a disadvantage.

In this light, the U.S., Australia, Morocco and Norway currently look best positioned to become hydrogen export powerhouses. The EU could play the role of leading technology supplier. Its infrastructure is advanced, but a scarcity of space and water in some member states will likely hold it back, making it dependent on imports.

Whether Germany and the EU develop a strategy to become leading hydrogen technology suppliers will largely depend on political support and investment conditions, and whether they implement “technology-neutral” policies that do not exclude any options from the beginning. Such policies face resistance in Germany and throughout the EU, as well as in the U.S., Australia and New Zealand. Critics claim that technology-neutral hydrogen programs would merely serve to underwrite fossil fuel projects with public funds.

However, countries like Russia, China, India, Japan and South Korea have no such qualms. They might favor the cheaper options for producing hydrogen that their energy systems provide. These include huge fossil fuel reserves, already enormous carbon-based energy imports or nuclear power plants. With these options at their disposal, their hydrogen industries will be more profitable from the start.