The energy revolution and its growing uncertainties

How fast the world moves toward cleaner energy hinges on several difficult-to-predict factors, the glut in oil and gas markets and disruptive technologies. What seems sure is that renewable energy sources won’t overtake fossil fuels in the medium term and that natural gas will loom larger in geopolitical conflicts.

In a nutshell

- The world is moving toward a decarbonized energy system

- Renewable energy is expanding dramatically

- So is demand for natural gas

- U.S. shale oil and gas supplies are putting pressure on OPEC and Russia

A shift toward reduced fossil fuel usage – known as decarbonization – is well under way. However, the speed of the transition to a cleaner global energy system depends on economic and geopolitical factors marked by increasing uncertainty. These include the oversupply in global oil and gas markets, worldwide climate mitigation policies, the movement toward investing in a rapid phaseout of fossil fuels, and new disruptive technologies.

As the expansion of renewable energy sources accelerates, Tight oil and shale gas exports from the United States will continue to grow, adding to the existing glut in the global oil and gas markets. In the short term, this could heat up the competition in Europe between U.S. and other suppliers of liquefied natural gas (LNG) and pipeline gas from Russia. However, this hinges on the demand for gas in Asia, especially China.

For most of the past decade, the world has experienced a parallel energy revolution with wide-ranging effects for global energy markets. In Europe, China, the U.S. and increasingly in many other regions of the world, renewables such as solar and wind power have expanded due to shrinking costs. Since 2010, the cost of photovoltaic (PV) capacity has decreased by 70 percent, wind power by 25 percent and battery costs for electric vehicles by 40 percent.

The U.S. has decreased greenhouse gas emissions more than in any other country.

Even more impressive has been the U.S. shale oil and gas revolution, which hastened the transition in the country’s energy market from coal to gas and transformed energy markets around the world. In the process, the U.S. has decreased greenhouse gas emissions more than any other country. These unprecedented changes may even speed up in the coming years, with digitization, automation, electric mobility, robotics and artificial intelligence transforming the entire energy sector. Geopolitically, accelerating decarbonization could even increase socioeconomic and political instability in many oil- and gas-producing countries, generating more regional volatility across the Middle East and Africa and threatening global security.

In its World Energy Outlook 2017 report, published last November, the International Energy Agency (IEA) identified four large-scale shifts, or “megatrends,” in international energy markets. The first of these was the rapid rise of clean energy technologies.

Facts & figures

Four ‘megatrends’ in the global energy system, 2017-2040

1. Rapid deployment and falling costs of clean energy technologies

Photovoltaic capacity has grown more than any other form of electricity generation

2. Growing electrification of energy

In 2016, consumers for the first time spent as much as on electricity as on oil products. Electricity is expanding in sectors previously confined to other fuels such as cars, heating and cooling

3. China’s shift toward a service-oriented economy and a cleaner energy mix

The country is undertaking new initiatives to decrease its heavy reliance on coal

4. Resilient U.S. shale gas and tight oil

The U.S. has remained the world’s largest oil and gas producer since 2014. Innovative and adaptable North American producers can sell these resources at highly competitive prices, leading to oversupply and dramatic price drops in world markets. The U.S. will continue to cement its leading position through 2040

Source: IEA

But despite the impressive expansion in renewables in recent years, they still account for just a fraction of global primary energy demand. For example, while solar power grew by 50 percent last year (and by some estimates could add another 660 gigawatts by 2022), the overall share of solar and wind power is just 2 percent of the world’s primary energy demand. In comparison, for biomass the figure is 10 percent, for hydropower it is 3 percent and for nuclear power it is 5 percent.

In the IEA’s main scenario, which calls for renewables to increase annually by 7 percent, their overall share in the world’s primary energy demand would only rise to 6 percent by 2040. Even under its more optimistic scenario, in which low-carbon energy sources (renewables, hydropower, bioenergy and nuclear) double their share in the energy mix to 40 percent and capture two-thirds of global investments in power plants to 2040, the world’s energy system would still be 60-percent based on fossil fuels (compared with 81 percent in 2016).

Demand picture

The IEA and many international oil experts concede that if electric vehicles (EVs) take off much faster than expected, their use could curb global oil demand more significantly. However, growing demand in other sectors – including the petrochemical industry (whose oil consumption could rise by 60 percent through 2040), freight shipping and aviation – might balance out any reductions. Even if the existing EV fleet grows spectacularly, from 2 million today to more than 300 million by 2040, there will still be 2 billion cars burning oil in their internal combustion engines.

In recent years, the Organization of the Petroleum Exporting Countries (OPEC) has had surprising success in curbing oil production. But the present rise in oil prices to $70 per barrel has depended on support from non-OPEC oil producers, especially Russia. Despite OPEC successfully negotiating an extension of its 1.8 million barrels per day production cut through the first half of 2018, it faces challenges on all fronts – both inside and outside the organization:

• U.S. tight oil: The recent return to a higher oil price has stimulated new, larger investments in U.S. shale oil projects. The industry’s continuing technological innovation and efficiency gains, leading to exponential production growth, have been repeatedly underestimated by international experts.

Facts & figures

Impacts of the U.S. shale oil revolution

- Between 2010 and 2015, the U.S.’s combined conventional and unconventional oil production nearly doubled from 5 million barrels per day (b/d) to 9.4 million b/d

- The number of countries importing U.S. oil has increased from just one (Canada) to 27, including countries in Latin America, Asia and Europe

- The IEA increased its growth estimates for U.S. crude oil production to 390,000 b/d for 2017 and 870,000 b/d for 2018

- The Energy Information Administration (EIA) raised its projections for total U.S. oil output to 10.34 million b/d by the end of 2018, up from 9.77 million b/d in December 2017

• Internal pressures: The OPEC producers that saw production drop and lost market share due to political instability and civil war (Iraq, Libya, Nigeria and Venezuela) or international sanctions (Iran) have a strategic interest in raising output to revive their economies. The last collective cuts were only possible at Saudi Arabia’s expense. The kingdom’s financial reserves have been shrinking rapidly – from $750 billion to less than $500 billion in just three years. The government’s efforts to diversify the economy away from dependence on oil and gas exports – its so-called “Vision 2030” strategy – needs huge investments to reach its goals. Any further extension of the output cut may result in a sustained loss of market share, particularly in oil-hungry Asia. For example, in November 2017, the U.S. exported a record amount of oil to China.

• Non-OPEC producers: Led by the U.S., non-OPEC producers expanded production by an estimated 630,000 barrels per day in 2017 and will add another 1.6 million barrels this year – 200,000 barrels per day more than previously forecasted. Russia has already questioned any new collectively agreed cut with OPEC, as skyrocketing U.S. oil exports eat away at their revenue and market share. But without a cut, oil prices in 2018 could fall to as low as $30 per barrel. Though Russia has based its state budget calculations on a breakeven price of $40, most other oil producers’ budgets are based on much higher prices.

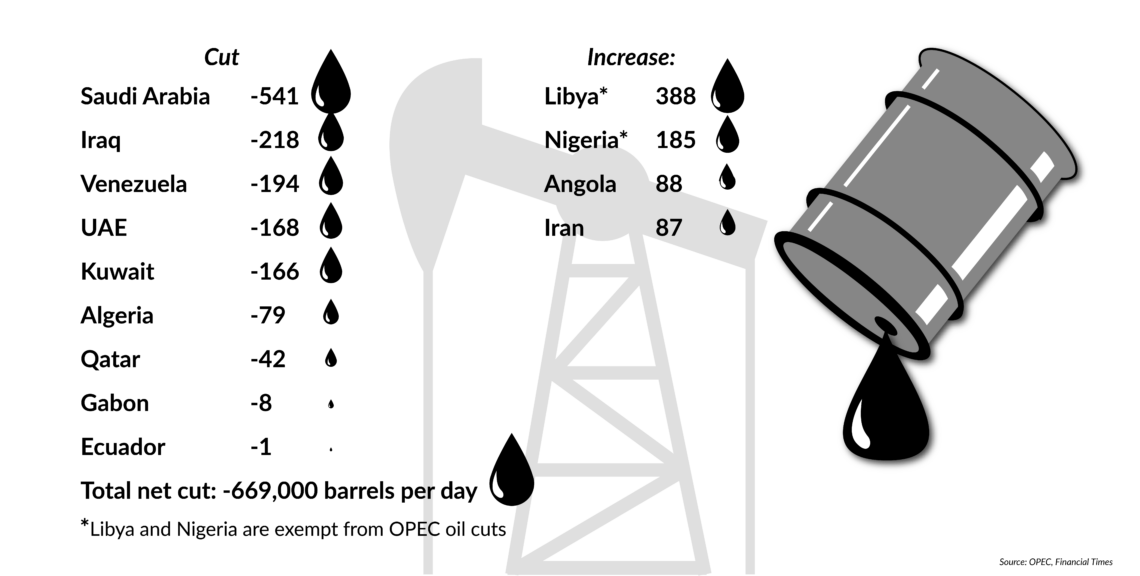

Facts & figures

OPEC's November 2017 output cut extension

Change in barrels per day (in thousands)

Natural gas

According to the IEA, natural gas is the only fossil fuel that will see substantial growth in demand (+45 percent) by 2040.

Facts & figures

Global gas and LNG demand by 2040

- 140 billion cubic meters (bcm) of LNG capacity is currently under construction

- Global demand is expected to increase by 45%

- U.S. demand is expected to rise by 300 bcm

- China’s demand is expected to rise by 200 bcm

- Russia’s demand is expected to rise by 145 bcm

- Iran’s demand is also expected to rise by 145 bcm

At present, Qatar – the world’s largest LNG exporter, ahead of Australia – is seeking to maintain its leading status and has lifted its self-imposed moratorium on developing the North Field. Nevertheless, by the mid-2020s, many experts expect the U.S. to become the leading global LNG exporter. By 2040, LNG’s global market share (versus that of gas pumped through pipelines) will increase from 39 percent in 2016 to around 60 percent.

LNG’s rising availability will help the European Union diversify its gas imports, though Russia will remain the bloc’s largest gas supplier. In 2040, the EU’s gas demand is expected to be about the same as it is today – 450 billion cubic meters a year. However, natural gas production within the EU is falling. By 2040, it is expected to decline by about 50 percent, to 65 billion cubic meters per year. That would trigger a corresponding increase in the demand for imports, to some 390 bcm per year.

Russia is seeking to maintain its economic and geopolitical influence in Europe by creating faits accomplis.

Amid a glut in the world’s gas markets and increasing competition from LNG producers in the U.S. and elsewhere, Russia is struggling to defend its market share, as well as its economic and geopolitical influence in Europe. It has done so mainly by creating faits accomplis. These include the construction of the Nord Stream 2 and the two TurkStream pipelines. Once these are built, Russia will no longer depend on Ukraine’s gas transit network and can undermine the EU’s intraregional gas interconnector projects, which may no longer be commercially viable for private European gas companies.

Some claim that U.S. opposition to Russia’s pipeline projects only serves its interest in expanding LNG exports to Europe. However, the U.S. government – in contrast to the Kremlin – is hardly able to dictate to its private LNG exporters where their supplies must be shipped (especially now that LNG exports to Asia have become much more profitable). But the EU must face the new challenge of how to balance “cheap” but heavily subsidized Russian gas exports against its gas diversification projects, including the much-desired U.S. LNG exports.

Strategic perspectives

Given rapid changes in the global energy markets and the introduction of new, disruptive technologies, the decarbonization of the worldwide energy system could occur faster than anticipated. This is highlighted by the following recent developments: 20 countries and two U.S. states have joined the “Powering Past Coal” alliance to phase out coal; France plans to end oil and gas production by 2040 and may be joined by other countries; the world’s largest listed oil and gas group, ExxonMobil, has bowed to shareholder demands to publish reports on the possible impact of climate policies on its business models and profits; and the World Bank will stop lending to any oil and gas projects after 2019. The bank will only make exceptions for gas projects in poor, developing countries where the fuel is needed to provide energy to local communities. The World Bank already began limiting financing for coal-fired power plants in 2013.

However, global electricity demand is predicted to grow much faster (IEA: 60 percent by 2040) than the overall growth of energy demand (30 percent). And this may even be an underestimation due to the increasing electrification of the transport and heating sectors, as well as the revolutionary effects of digitization, robotics and artificial intelligence on the world economy.