An oil giant with a chronic disease

Iraq has managed to bring its oil production back to pre-war levels, but its aging infrastructure is in dire need of investment – which might not materialize in the current economic climate. The country’s economy remains dangerously dependent on oil.

In a nutshell

- The Iraqi oil industry has overcome several major setbacks

- Other economic sectors remain critically underdeveloped

- Any upheaval in oil prices could cripple Iraq’s fragile state

Iraq has a major success story in its oil industry. It is one of the very few oil-rich countries in the world to have experienced devastating wars and still managed not only to exceed prewar production levels but also to maintain impressive growth momentum.

Iraq is also expected to be the third-largest contributor to oil supply growth by 2024. What Baghdad has accomplished in the oil sector, however, it has failed to replicate elsewhere. The economy remains substantially dependent on oil revenues and is therefore vulnerable to the vagaries of global oil markets.

With some of the largest proven oil reserves in the world, Iraq’s potential as a major producer and exporter is unquestionable. Unlike most of its neighbors, though, the country has failed to channel some of its oil revenues into a sovereign wealth fund; oil money has largely sponsored wasteful government habits. The oil sector has flourished thanks to the involvement of international oil companies. Meanwhile the private sector in other industries is anemic and the public sector remains bloated and inefficient.

Facts & figures

Oil in Iraq

- Iraq sits on the fifth-largest proven oil reserves in the world after Venezuela, Saudi Arabia, Canada and Iran. These reserves also account for 14% and 12% of proven oil reserves in the Middle East and OPEC, respectively

- 60% of the country’s proven oil reserves are located in Southern Iraq

- Almost 90% of Iraq oil exports are shipped from the southern terminals in the Gulf, and pass through the Strait of Hormuz

- Asia is the top importer of Iraqi crude oil, capturing more than 50% of the country’s total crude exports

- Iraq is the only major oil producer in the Middle East that relies heavily on substantial volumes of imported diesel and gasoline due to underperforming refineries and an underdeveloped onshore pipeline system

- Iraq is the second-largest gas flaring nation in the world after Russia

- Iraq imports 7 gigawatts of electricity from Iran to meet domestic needs as it struggles to achieve self-sufficiency

Roller coaster

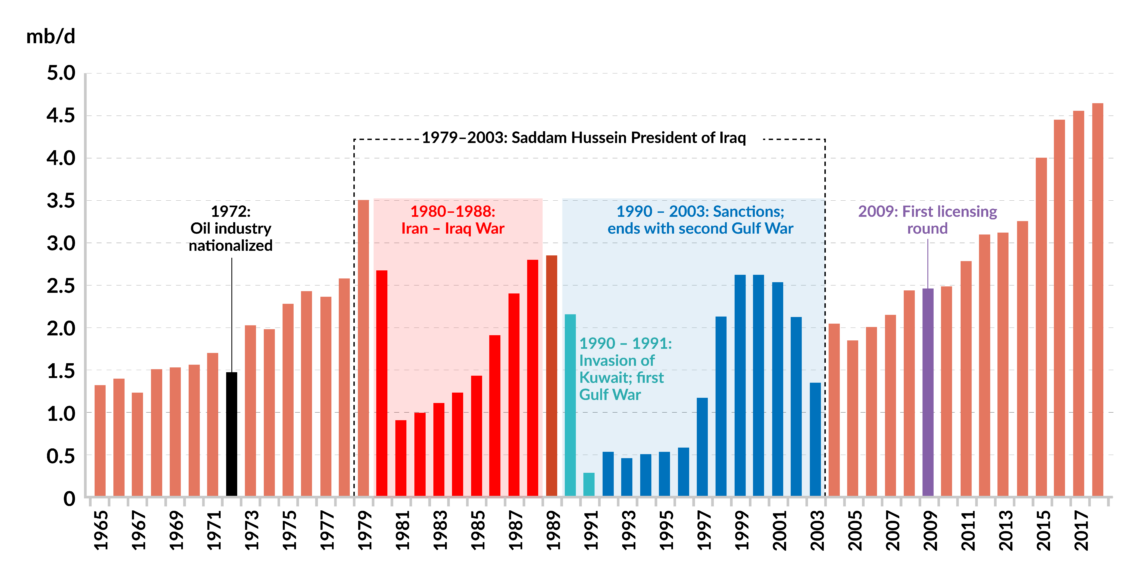

For years, Iraq’s oil potential was constrained by exogenous factors. For four decades, whenever Iraq’s oil production started to take off, it soon suffered a major setback, primarily because of war. Oil production first peaked in 1979 but it took more than 35 years for the country to return to that level.

The opening of the oil sector to international capital, after the Second Gulf War, marked the beginning of a rapid growth phase that still lasts to this day. In 2009, Iraq was producing 2.4 million barrels a day (mb/d), the same level as in 1976. Five years later, Iraq exceeded its previous oil production peak. By the end of 2019, production hit 4.6 mb/d – a new record, nearly doubling in 10 years and gaining significant market share both globally and within OPEC.

For years, Iraq’s oil potential was constrained by exogenous factors.

Most of the growth comes from oil fields awarded during the first two licensing rounds in 2009 and 2010. Currently, Iraq provides nearly 6 percent of global oil supply and is the fifth-largest oil producer in the world, after the United States, Saudi Arabia, Russia and Canada. In 2009, it was the ninth-largest producer after Russia, Saudi Arabia, the U.S., Iran, China, Canada, Mexico and the United Arab Emirates. Iraq exports 60 percent of its production and has become the world’s third-largest crude oil exporter, after Saudi Arabia and Russia.

The International Energy Agency (IEA) expects the third-largest growth in oil supply by 2024 to come from Iraq (0.94 mb/d), after Brazil (1.17 mb/d) and the U.S. (4.08 mb/d). The agency further projects production to increase by around 1.2 mb/d over the next 10 years, reaching nearly 6 mb/d of production in 2030, and overtaking Canada as the world’s fourth-largest producer. Iraq plans to boost its oil production to 8 mb/d in the next two decades.

Iraq and OPEC

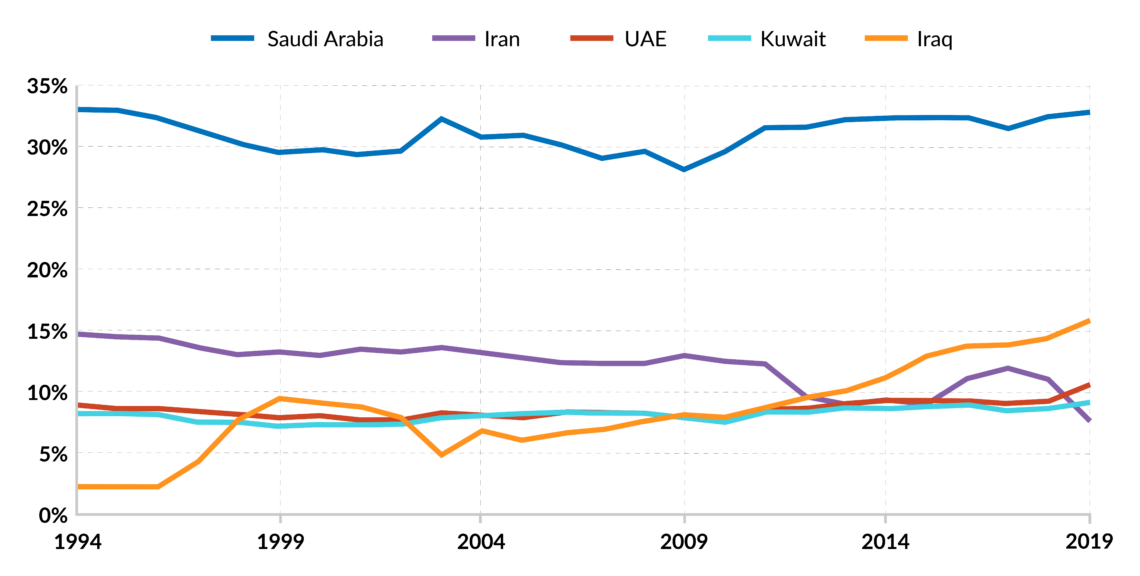

Iraq is a founding member of OPEC, but it has given the organization – particularly its de facto leader, Saudi Arabia – many headaches in recent years. It is the only OPEC country to have significantly expanded its production over the last 10 years, gaining market share within the organization at the expense of other members. In 2009, Iraq’s share surpassed that of both the UAE and Kuwait, then Iran in 2013, finally becoming the organization’s second-largest producer after Saudi Arabia. The structure of Iraq’s oil industry differs from those of other major OPEC producers.

Facts & figures

After the invasion of Kuwait in 1990 and up until 2016, the OPEC quota did not apply to Iraq. That changed with the OPEC+ deal of December 2016, when it reluctantly accepted to shoulder the second-largest production cut within OPEC, after Saudi Arabia. Baghdad had been misbehaving and was continuously accused of cheating – not to imply that all other members were well-behaved.

Unlike other noncompliant members however, given the scale of its production, if Iraq does not adhere to the organization’s production targets, the outcome of any collective production-cut strategy is severely affected. The low compliance of Iraq (and other members of OPEC) may have contributed to Saudi Arabia’s decision, in March 2020, to flood the market and sell its oil at a discounted price in a move to reinstate discipline within the organization.

Several reasons can explain Iraq’s poor adherence to OPEC production cuts. First, Iraqi officials have repeatedly requested that their country be compensated for the loss of market share during years of conflict, including the recent struggle with Islamic State. At current production levels, Iraq’s 150 billion barrels of proven oil reserves (9 percent of the world’s total) are expected to last another 87 years, just a few years behind Kuwait and 30 years ahead of Saudi Arabia. It is therefore crucial for Iraq to monetize those resources as quickly as possible before oil falls out of favor.

Secondly, Iraq’s economy is extremely dependent on oil revenues, particularly when compared to its Gulf peers in OPEC. Any production cuts would translate into shrinking revenues – especially if oil prices increase only moderately or not at all. The economic pain would be disproportionate for Iraq.

The structure of Iraq’s oil industry differs from those of other major OPEC producers.

Finally, the structure of Iraq’s oil industry differs from those of other major OPEC producers. Unlike the Gulf countries, Iraq’s oil sector is run by international companies rather than the state. The Iraq National Oil Company (INOC) was founded in 1966, then broken up in 1987, only to be reestablished in 2018. It is difficult for the government to impose production restrictions on international companies, especially given the existing contract structure. The contracts awarded in the first two licensing rounds commit companies to reach a certain production plateau target – one of the two bidding parameters, the other being the service fee.

The bidder with the highest plateau target and the lowest fee won the round. If production falls below target, investors have to wait longer to recover their costs and in some cases penalties apply. Although the plateau targets for several contracts were later revised downward, companies still have to meet certain expansion plans.

Structural weaknesses

According to the International Monetary Fund (2019), Iraq’s oil sector generated more than $850 billion between 2003 and 2018. With such sums, Iraq should have transformed its economy, substantially improved the living standards of its people and accumulated financial assets that could have contributed to the welfare of future generations. This scenario, however, could not be further from reality.

Iraq is resource-rich but economically poor. Its economy is one of the most oil-dependent in the world. The oil sector provides nearly half of the gross domestic product (GDP) and more than 92 percent of total export earnings. In some years the figure was as high as 100 percent, according to World Bank data. The sector also generates more than 92 percent of government revenues. The economy is therefore fully exposed to the volatility of global oil markets, doing well when prices are high and suffering when they fall.

Worst of all is that Iraq has not invested its oil money in a stabilization fund. Doing so would have sustained key macroeconomic variables and public finances, helping to shield the economy from the negative effects of unexpected drops in government revenue as a result of fluctuations in oil prices.

Facts & figures

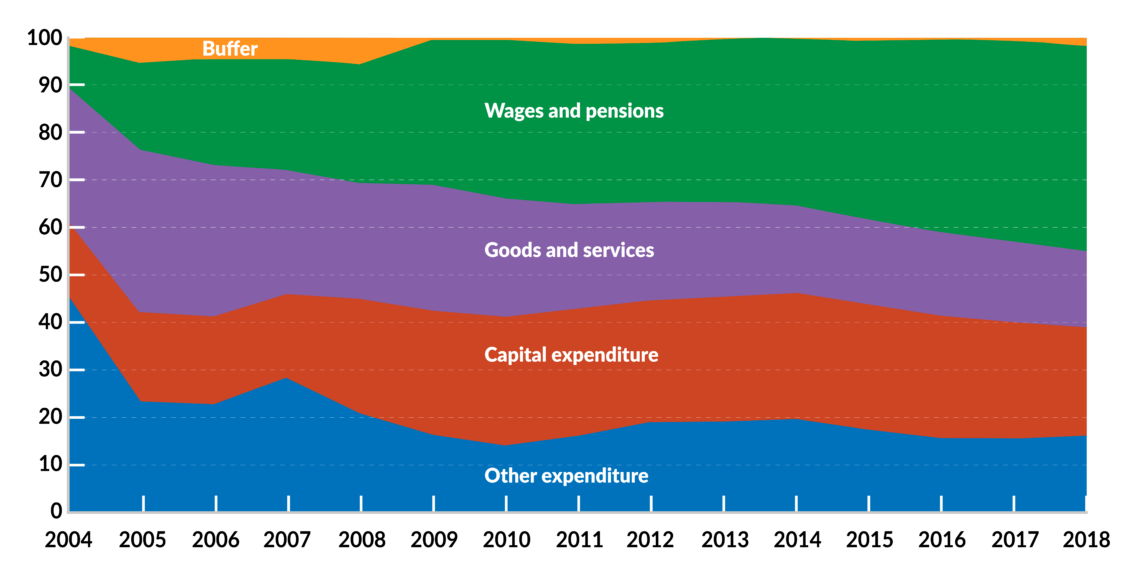

The public sector is massively bloated, accounting for nearly half of total employment. Its spending amounts to more than 61 percent of GDP. Public sector wages absorb the lion’s share of those expenditures, with little left to be invested in financial assets or essential human and physical capital. Oil revenues have been used to safeguard political support, establish a system of patronage and centralize power – a long tradition in Iraq.

Beyond oil, the private sector is lifeless. Iraq remains a challenging place to conduct business, ranking 172 out of 190 countries on the World Bank’s Ease of Doing Business for 2019. Corruption is rampant. The country ranks 162 out of 180 countries on Transparency International’s 2019 Corruption Perceptions Index. Iraq also suffers from chronic fragility, ranking 13 out of 178 countries on the Fragile States Index.

In October 2019, people took to the streets to express their anger at endemic corruption, high unemployment, inefficient administration and foreign interference. The protest soon turned violent; over 500 people were killed and tens of thousands wounded, leading to the resignation of Prime Minister Adel Abdul-Mahdi.

Although the war on Islamic State is officially over, the related security risk remains high. The relationship between the Kurdish Regional Government (KRG) and the Federal Government is mercurial. Meanwhile, Iranian influence in Iraq continues to grow, much to Washington’s frustration. The killing of Iranian General Qassem Soleimani earlier this year in a U.S. air strike near Baghdad International Airport led to tit-for-tat attacks, albeit on a small scale, between the U.S. and Iran, on Iraqi soil.

Scenarios

There is no doubt that few countries can compete with Iraq’s oil potential. However, outside the oil sector, there is little to envy Iraq. The expansion of oil production and subsequent revenues have not resulted in a stronger economy. On the contrary, Iraq, perhaps more than any of its Middle Eastern OPEC peers (except for Iran), is at the mercy of fluctuations in oil prices. Even modest swings in oil prices will have an impact on the economy. According to the IMF, every $1 decline per barrel in oil prices lowers Iraq’s annual oil revenue by 0.6 percent of GDP.

The recent oil price crash, mostly caused by Saudi Arabia and the coronavirus, will weigh substantially on Iraq from an economic, political and security standpoint. After all, everything revolves around oil in Baghdad. The longer the current price environment lasts, the higher the risks. Even oil production growth is threatened.

To support future output, Iraq needs to undertake substantial investment in upgrading and expanding existing production, processing and export infrastructure. International investors are already wary of the difficult investment climate in the country, even more so today under the prevailing low oil prices. No wonder the IEA describes Iraq as a “vulnerable supplier.” “In the medium term, heightened security concerns might make it more difficult for Iraq to build production capacity,” the agency adds.

Besides, what is the point of expanding production if the population’s living standards do not improve? Without drastic economic reforms, Iraq will remain a wild card for global oil markets and OPEC and its own citizens – a giant with a chronic disease.