Blockchain and its potential for economic disruption

Blockchain – a decentralized ledger of transactions that uses computer technology to link, secure and encrypt records – has the potential to become a hugely disruptive technology, rendering financial intermediaries unnecessary and making money transfers nearly instantaneous.

In a nutshell

- Blockchain has the potential to revolutionize the global economy

- It could destroy many industries that provide “intermediary” services

- There are several challenges, including the huge amounts of energy and data required

- These difficulties are already spurring innovation

Austrian economist Joseph Schumpeter made the term “creative destruction” famous with his vision of capitalism as an evolutionary process in which disruptive innovations lead to the replacement of old industries and structural change in the economy. For example, digital cameras replaced film photography, online streaming replaced mp3 players, which had replaced compact discs, and so on, while Amazon has (partly) replaced our traditional bookstores. In the digital age, innovations occur faster. One recent innovation with the potential to disrupt old “structures” and create new services is the blockchain.

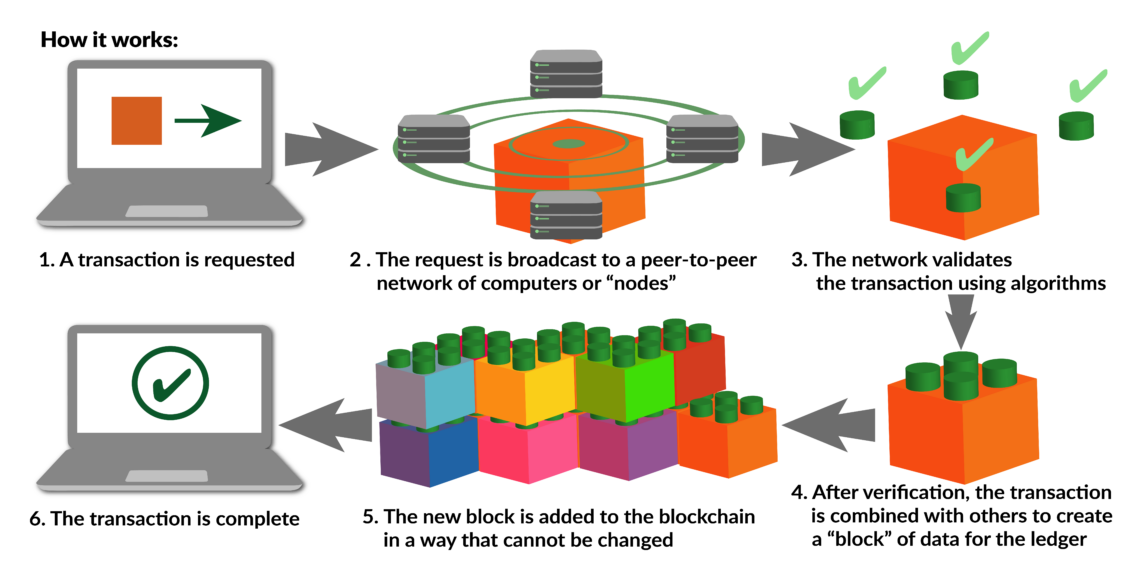

The blockchain emerged with Bitcoin, the cryptocurrency, as its system of recording transactions. Unlike a centralized shareable database, it is not merely decentralized but a public, distributed ledger: the members (computers) or “nodes” of the blockchain network each have a regularly updated copy of the ledger and therefore “the truth.”

Cryptography helps ensure that the system is secure. Any change in one copy will be signaled to other nodes, and a mechanism for a consensus of the majority of nodes validates the change. Given the number of nodes, this means the system is theoretically tamperproof and its history “immutable.” Combined with automated “smart contracts,” blockchain technology has the potential to create economic value in many fields.

Decentralizing force

To understand how, a short detour into economic theory is useful. Nobel Prize-winning economist Ronald Coase famously explained the emergence of the “firm” as a mechanism to reduce transaction costs associated with market exchanges: the costs of searching for information on suppliers or distributors on the market, negotiating with them, monitoring and enforcing deals, facing uncertainty, and so on. To avoid those costs, entrepreneurs hire staff on a longer-term basis for in-house production. Of course, as a company’s size increases, so do other, organizational costs. The firm, a kind of island of command and control within markets, finds its optimal size in the trade-off between these two sorts of costs.

Blockchain can make financial intermediaries redundant.

Another way to reduce transaction costs in the market is to have specialists – intermediaries or “middlemen” – who guarantee transactions and bring trust. A large chunk of economic activity is just this. Back in the 1970s, the economist Douglass North, another Nobel laureate in economics, showed that some 45 percent of the United States’ gross national product was devoted to the “transaction sector.” Banks are an obvious example of such intermediaries: they guarantee payments. Now, in the internet age, we have “centralized” platforms such as eBay or Airbnb that guarantee transactions between buyers and sellers within their own marketplaces.

Blockchain technology can make such intermediaries redundant, shortening the channel between two parties to a transaction while generating “automated trust.” This would reduce transaction costs even further and significantly disrupt many industries that perform the role of centralized middlemen. This process of decentralization would translate into a wave of “disintermediation.”

Shortening the chain

Bitcoin’s successes so far raise questions about the future of the banking industry, and even money itself. Under the current system, payment latency is a huge issue: it can take days for the money in a transaction to “flow” between the various intermediaries, generating delays in settlements. The capital is immobilized and therefore unproductive, hindering the economy. Blockchain technology could, in theory, eliminate the chain of intermediaries and reduce payment latency to a few minutes.

Banks have anticipated the possible disruption and are developing their own blockchain projects, often breaking the paradigm of a public ledger by creating “private” blockchains. In developing countries with very low banking rates, the potential is probably even greater – think of the first success of M-Pesa in some Eastern African countries (see box). This would occur not because it would save costs by eliminating middlemen, but because demand for inexpensive banking is strong – access to banking services in these countries is low, though growing rapidly.

Facts & figures

M-Pesa

M-Pesa (which is not based on blockchain technology) is a service that allows users to transfer money via mobile phone. The “M” stands for “mobile” and “Pesa” means “money” in Swahili. It was launched in 2007 by Vodafone for Safaricom in Kenya and Vodacom in Tanzania.

Users can deposit money into an account stored on their mobile phones, send money transfers via text message and redeem deposits for regular money. Sending and withdrawing money incurs a small fee.

The service has spread quickly, with operations in Afghanistan, South Africa, India and Romania. By 2012, there were 17 million M-Pesa accounts in Kenya, and 7 million in Tanzania.

Another promising application is for land titling in poor countries. In his famous book The Mystery of Capital, Peruvian economist Hernando De Soto explained how the extralegality of the poor’s possessions – the absence of formal titles over assets like land and houses – created uncertainty that discouraged investing in them, and hindered their use, for example, as collateral for bank loans. The absence of a formal title renders capital unproductive and correlates to bureaucratic inefficiency and corruption. The introduction of a new type of record-keeping based on blockchain technology could solve the problem. In 2017, the country of Georgia decided to implement such a system.

Many other fields could be disrupted by blockchain technology applications. The list goes from car-hire services like Uber or music streaming services like Deezer or Spotify, to better controlling how money is donated to charities (reducing corruption), or even voting (securing fairer election processes). The Internet of Things (connected objects), crowdfunding, managing welfare benefits, supply-chain management and many more would also benefit.

Will blockchain change the many industries based on intermediary services? The potential is huge, but despite the technology’s promises, several challenges must be overcome to ensure broad, stable and secure usability.

Power hungry

The first challenge of distributed ledger technology is that none of the nodes in the chain – that is, computers – are specialized in one task. On the contrary, they all do the same operations: transaction verification and storing. That is a lot of power to do the same thing, especially as maintaining the blockchain requires “mining” (creating blocks) on extremely power-hungry computers.

Second, with the “history” of the ledger constantly growing over time, at a faster pace as the number of transactions increases, computer hardware storage (hard disks) will have to keep pace to store the blockchain. The size of the Ethereum blockchain, for example, has reached several hundred gigabytes in a little more than three years.

Third is the problem of scalability – notably the ability to process a certain amount of transactions. The Bitcoin network, for example, with a few transactions per second, still lags far behind Visa, which processes several thousand per second. Its storing (every 10 minutes) and verifying (50 minutes) process time is slow – and only amounts to a tiny fraction of the usage volume of Visa cards.

Some also worry about the security of the system itself. Aside from hacks in the coding, which have happened in the past, the very validation process could be problematic. After all, it is based on a form of consensus. What if a “consensus” of nodes makes the wrong decision? This is the so-called “51-percent attack” scenario: by gaining mining capacity greater than that of the existing network, someone could take control of the system and alter the ledger. While the high cost of such an operation would make this impossible for an individual or even a group of individuals, for very large entities – like governments – it seems well within the realm of possibility.

Ensuring that various blockchains can exchange information involves developing standards to enable interfacing.

Another type of hurdle is interoperability: for the technology to create value, blockchains need to communicate with other systems and with each other. On the one hand, this involves “translating” the existing legacy system, which would probably take a few years. On the other, ensuring that various blockchains can exchange information involves developing standards to enable interfacing. Such developments will take time.

Emerging competition

These obstacles represent opportunities for the many entrepreneurs who have jumped on the bandwagon and have already begun to address them. As with many other innovations, the blockchain will be incrementally improved thanks to competition to deliver the best solution. Many “crypto entrepreneurs” have benefited from the hype about blockchain and token sales – and certainly from the 2017 surge in the price of Bitcoin. It is interesting to see such people transition from the status of small, lonely “geeks” to entrepreneurs at the head of businesses hiring dozens of employees. This funding has created a significant new market.

Given this new market scale, innovations will unfold in a “discovery procedure” led by entrepreneurs. And innovations from other fields – such as quantum computers upstream and new “apps” downstream – will no doubt coalesce with innovations in blockchain technology to push the Schumpeterian process forward. Just like with the internet and the cascade of innovations it both fed upon and spurred, the process promises to be “restless.” There will be plenty of hype and mistakes, but genuine, impressive progress as well. It will all be fascinating to watch.