Stability, but for how long? China’s 2022 economic outlook

Chinese officials are pulling out all the stops to ensure growth and stability ahead of the 20th Communist Party Congress in October, where President Xi Jinping intends to solidify his position as he heads into a third term.

In a nutshell

- The Chinese economy’s performance has been disappointing

- President Xi wants to ensure a smooth transition to a third term

- Beijing will use all of its policy tools to maintain growth and stability this year

The health of China’s economy determines the fate of the Chinese Communist Party. Authoritarian regimes, like the one in China, base their legitimacy on economic performance. While governments in Western countries are often voted out of office when the economy slumps, the democratic structure typically remains intact. In China, a bad enough economic downturn could lead to a collapse of the entire system.

China also has an outsize impact on the global economy – a slowdown in the country puts a drag on worldwide growth and can bring recession to countries that depend heavily on trade with Chinese partners. For these reasons, it is worth examining the Chinese economy and analyzing its prospects.

Economic weakness

In 2021, Chinese authorities experimented with new regulatory measures. In January, high-profile businessman Jack Ma returned from a three-month disappearance after regulators canceled the initial public offering of Ant Group, the digital payment company he founded. In July, China’s digital regulators cracked down on ride-hailing giant Didi, after it listed on the New York Stock Exchange. Together, these events showed how aggressively the Chinese government was willing to act against private companies it thinks are becoming too powerful, and set the stage for a series of regulations targeting after-school education companies and video games.

Through these measures, President Xi Jinping is trying to cement the CCP as the world’s most powerful economic strongman. He is also working to put several of his own philosophies into practice, including “curbing the disorderly expansion of capital,” “no speculation on housing,” and “common prosperity.” These experiments have greatly undermined the business community’s confidence in the country.

Consumption has simply not been able to recover from the hit it took during the pandemic.

Consumption, investment and exports are the troika that drive the Chinese economy, and last year two out of those three – consumption and investment – performed poorly. Demand was weak. Food and beverage consumption saw annual declines in August, November and December 2021, mainly because of restrictions on dining out imposed to curb the Covid-19 pandemic. Due to issues like chip shortages, auto sales grew only 7.6 percent in 2021 – a disappointing result after the economic slump of 2020 – dragging down the overall growth rate of total consumer goods retail sales.

Per capita, consumption expenditure increased by 13.6 percent annually in nominal terms, but the two-year real growth average was only 4 percent. Consumption has simply not been able to recover from the hit it took during the pandemic. Retail sales, for example, fell short of expectations in December 2021, growing by only 1.7 percent against the same period the previous year, the slowest rate since August 2020.

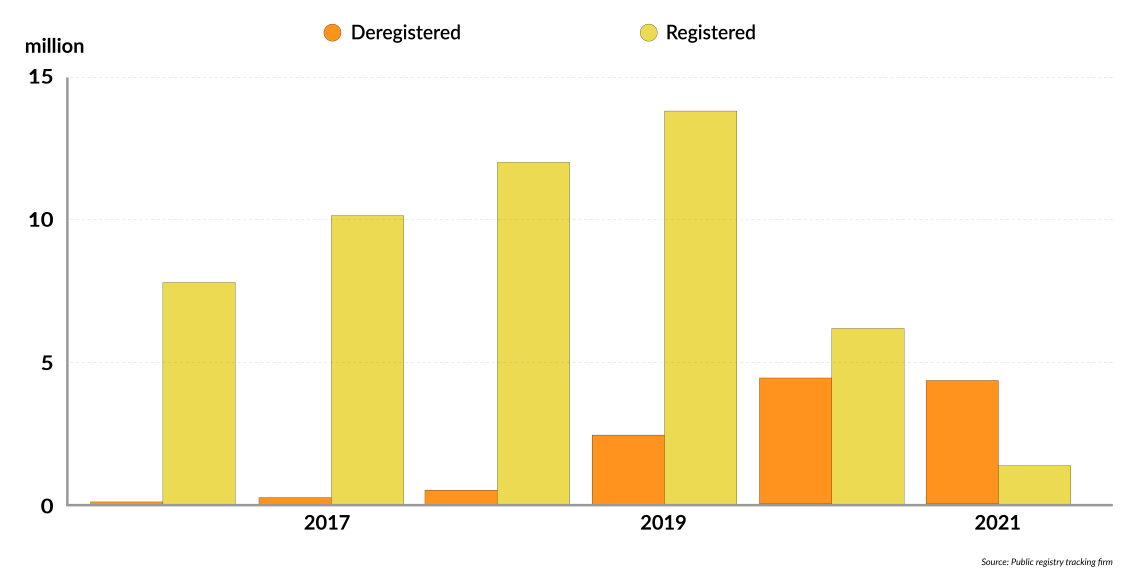

Manufacturers’ profits shrank in 2021, making them less willing to invest. Cumulative growth in fixed asset investment fell rapidly from 35 percent in February 2021 to 4.9 percent in December. In the first 11 months of 2021, 4.37 million small and medium-sized enterprises (SMEs) closed in China, marking the first time in 20 years when the number of businesses closing exceeded the number of businesses opening. Enterprises high up in the industrial value chain and high-tech firms were among the few sectors that saw increased rates of investment.

Facts & figures

Chinese small and micro business activity, 2016-2021

Investment in real estate and infrastructure accounted for less overall investment in 2021 than in years past. The difficulties in China’s real estate market have been well documented, and the weak property market is constraining local governments’ tax income, meaning they spend less on things like infrastructure.

Positive signs

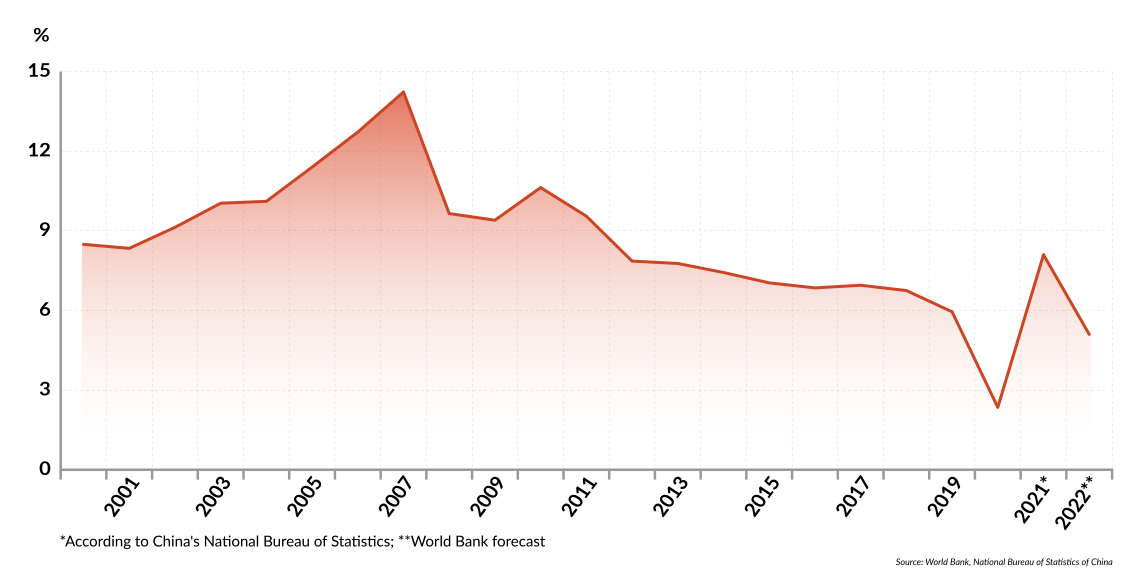

The news was not all bad for China’s economy last year. The country’s National Bureau of Statistics said gross domestic product (GDP) grew by 8.1 percent – slightly more than the 8 percent that had been expected. But even this good news belies a worrying trend. China’s economic growth is sinking rapidly. In the first quarter of 2021, GDP rose 18.3 percent in the same period the year before. In the second quarter, the figure was just 7.9 percent. In the third, it was 4.9 percent and in the fourth quarter of 2021, it was only 4 percent.

Another positive for China’s economy in 2021 was exports. Developed countries’ enormous stimulus policies increased demand for Chinese goods, especially since other suppliers in Southeast Asia were still struggling to fulfill orders due to Covid-19 restrictions. In 2021, Chinese exports exceeded imports by more than $676 billion – a $152 billion rise over 2020 and the highest value reached since officials began recording such statistics in 1950.

Even though investment as a whole was lower, foreign investment in actual use (a measure that excludes the banking, securities and insurance sectors) rose by nearly 15 percent in 2021 to 1.15 trillion yuan – another record. In high-tech industries, this figure grew at a rate of 17.1 percent in 2021, with investment in high-tech manufacturing growing by 10.7 percent and in high-tech services by 19.2 percent.

Overall, these results do not align well with President Xi’s dual circulation strategy, which aimed for growth based more on domestic consumption and less on exports.

Worrying prospects

Two politically charged events are guiding the CCP’s actions this year. The first is the recently concluded Winter Olympic Games in Beijing, which the party wanted to use to burnish its image at home and abroad at any cost. The financial gains the games brought in are sure to be much less than what Beijing had originally hoped for when it won the right to host them.

The most important event of the year is the 20th National Congress of the Chinese Communist Party, due to be held in October, where President Xi’s primary goal is to secure a smooth transition to his third term. He is eager to ensure that China’s economic engine does not stall, and the CCP will exhaust all of its policy tools to achieve that outcome.

Some institutions are not optimistic about China’s economic growth prospects. The World Bank predicts that China’s GDP will increase at a rate of just 5.1 percent in 2022. (Though Western societies would rejoice at such figures, China still needs much more rapid growth to improve living standards.) The Chinese leadership recognizes the difficult situation. In December last year, the Central Economic Work Conference concluded that the country’s economic development was facing “demand contraction, supply shock and weakening expectations.”

The Chinese government will likely deploy a variety of strategies to boost the economy for the 20th National Congress.

Take exports, which will almost certainly not be as strong as in 2021. As the global economy gradually recovers, governments will wind down their large-scale stimulus programs, weakening demand. And as restrictions are lifted, more and more orders will return to Southeast Asia and other regions.

China’s hot property market has cooled, as real estate companies like Evergrande fell on hard times. Local governments have become accustomed to obtaining a significant proportion of their revenue – 25 percent, on average – from land sales, and now they have to tighten their belts. As they spend and invest less, growth slows.

At the end of 2021, Hegang, a prefecture-level city, announced that it would implement fiscal restructuring – equivalent to bankruptcy in the West, while more and more third-tier cities have decided to implement more fines and fees to help address its financial problems. Even in the economically developed provinces of Guangdong and Zhejiang, civil servants’ salaries have been reduced and subsidies suspended.

Securing stability

The Chinese government will likely deploy a variety of strategies to boost the economy for the 20th National Congress.

Faced with domestic market pressure, China’s central bank cut borrowing rates for medium-term loans, hoping to cushion China’s slowing economic growth. Since December, it has increased support for small and micro businesses. Expect it to take more steps to loosen monetary policy and ease lending.

Banks will be urged to increase mortgage lending and scale back restrictions on property purchases in certain cities. Regulators’ tacit approval of Evergrande’s debt rollover program is a sign that officials are easing up on property market rules. Other cash-strapped Chinese developers are also expected to rush to negotiate new terms with bondholders to avoid default. While this does not eliminate risk in the sector, it does provide a breathing space. The message is clear: there must be no turmoil before the National Congress in October.

Facts & figures

Chinese GDP growth (%), 2000-2022

In addition, officials are implementing a set of proactive fiscal policies to secure infrastructure projects – including ones that are high-tech oriented – to boost the economy. The firms chosen to carry out these projects are, of course, state-owned enterprises, not private companies.

China is strongly encouraging foreign investment in the country. At the end of 2021, it reduced the items restricted or prohibited to foreign investors from 33 to 31. The central government is also encouraging local authorities to maximize the role of 21 pilot free trade zones and the Hainan free trade port to attract more foreign investment. Meanwhile, to keep foreign experts in the country, it extended preferential tax policies for foreigners until the end of 2023.

Beijing will also not pursue carbon reduction as aggressively this year. President Xi has no intention of abandoning his decarbonization goals – the country’s carbon emissions are to peak before 2030, and China should reach carbon neutrality by 2060. However, he will take care to make sure that economic development continues uninterrupted ahead of the National Congress in October. That means temporarily slowing the pace of decarbonization, at least to avoid the type of energy crunch and economic deceleration that happened in the second half of last year. Originally, China’s steel industry was supposed to reach peak carbon emissions by 2025. Now that has been pushed back to 2030.

The country’s zero-Covid strategy will likely be adjusted after October, and it is already trying to come up with better vaccines so that it can ease up on its draconian anti-pandemic measures. China is developing a more effective mRNA vaccine, expected to hit the market this year. Regulators are reviewing mRNA vaccines developed by Germany’s BioNTech and Shanghai-based Fosun Pharma. Another Shanghai-based firm, Everest Medicine, has partnered with Canadian biotechnology companies to manufacture and market its potential mRNA Covid-19 vaccine in China.

Scenarios

In one scenario, China continues its brutal zero-Covid policy as the Omicron variant of Covid-19 spreads, inevitably leading to supply chain disruptions. For example, the cobalt mine in Zhejiang Province was shut down in December, pushing up cobalt prices. Domestic consumption will remain weak. The status of 200 million young people in “flexible employment” with low pay, long hours and less social security will remain unchanged.

A proliferation of rigorous zero-Covid policies and weak domestic purchasing power would increase the chance that China’s economic growth will stall. If the global economy continues to sour due to the pandemic, then GDP could increase by just 4 percent or less this year.

In the second scenario, China’s exports remain relatively strong throughout the middle of this year. The Regional Comprehensive Economic Partnership (RCEP), which came into force on January 1, provides a strong boost to the Chinese economy. China expands trade to RCEP member countries, making up for the orders that go back to Southeast Asia. The trade deal could even increase demand for Chinese goods abroad and drive a resurgence of consumption at home.

Domestic consumption would also recover as soon as a more effective vaccine is introduced, allowing Chinese officials to adopt a more rational approach toward hindering the spread of Covid-19. A proactive fiscal policy will push down inflation while maintaining income and employment at acceptable levels. Due to these moves, economic growth in the second half of the year will look better than that of the first half. GDP growth for 2022 would come in at between 5 and 6 percent.

The second scenario is more likely. Although there is plenty of volatility and uncertainty in the global economy, and the Chinese economy faces a raft of challenges, the authorities in Beijing will use all of the tools at their disposal to keep the economy on track – at least until the start of President Xi’s third term. An economic collapse is unlikely, though supply chain disruptions pose a significant risk.

While the global economic and political environment remains chaotic, China will, for this year, hold stable. The big question mark surrounds the sustainability of the policies being implemented. When it comes to the many structural problems that should have been addressed long ago, officials are still just kicking the can down the road.