Bureaucrats crack under pressure

After decades of generous monetary policy, China announced it would take a more moderate approach – but policymakers have now realized that future growth will be lower than needed. A more rigorous monetary policy may be a source of tensions and possible crisis.

In a nutshell

- China is increasingly concerned about economic performance

- Its grand geopolitical ambitions require faster growth

- A recent reversal on monetary policy shows their worry

China boosted its economic performance for decades through heavy government intervention, notably by manipulating credit and banking and engaging in large, state-directed investment programs. The political sphere routinely encouraged or carried out questionable projects, and then transformed them into success stories by covering the losses through transfers of newly printed money, or by “inviting” commercial banks to hand out easy credit and rescue ailing companies.

One may rightly argue that China’s impressive economic performance is also rooted in other causes: partial privatization of the economy, increasing openness to foreign trade, and large inflows of foreign investment and technology. Nonetheless, and despite open criticism by alleged free-market supporters, China’s manipulation of money and banking has been a crucial component of Beijing’s policymaking, and has found plenty of enthusiastic followers – including the major Western central banks. However, some cracks in the Chinese financial architecture are now coming to the surface and causing concern.

Insufficient growth

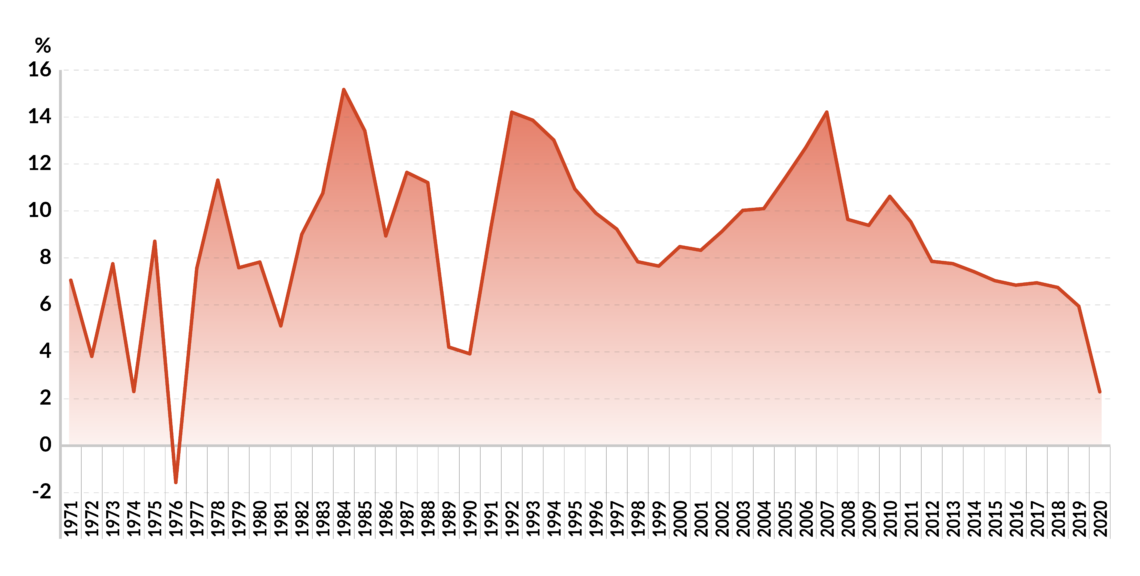

Though annual growth rates measured by gross domestic product (GDP) have been around 10 percent between 1978 and 2012, for the last decade the Chinese economy has been heading toward the 5 percent line. This is still an amazing performance, especially compared to Western countries and most developing economies. But it may not be enough.

First, a large portion of the population has expectations about its future, and seeks more for themselves. The high rate of savings – well above 40 percent of GDP during the past ten years, as opposed to about 8 percent in the United States and 12 percent in the EU in the pre-Covid-19 decade – means that, so far, domestic demand for consumer goods has been relatively weak and has contributed to absorbing inflationary pressures. At the same time, those very savings reflect an eagerness to consume more in the coming years, as well as possible fear about the future.

China’s manipulation of money and banking has been a crucial component of Beijing’s policymaking.

The only way Chinese policymakers can respond and defuse possible tensions is by delivering high enough growth rates. Of course, it is impossible to define what “high enough” means; but the fact that early this year, authorities failed for the first time to give growth figures in the 2021-2025 plan reveals that this has now become a delicate issue.

Expensive plans

A second question relates to Beijing’s grand geopolitical ambitions. These translate into gigantic transnational infrastructural programs, easy credit handed to selected private and public debtors, and a drive to acquire control of key companies around the world. Hegemonic designs are expensive, and they must be sustained with significant and possibly ever-more resources year after year. Once again, this means that growth must stay high.

To summarize the overall picture, it seems that the Chinese authorities have realized that growth in the next few years is unlikely to be much above 5 percent, and that tensions are perhaps around the corner. For example, China claims it intends to stimulate consumer demand – but what happens if additional aggregate demand meets supply bottlenecks, i.e., if production does not grow fast enough? Would the Chinese accept lower exports, at the risk of letting the yuan appreciate, thus losing foreign investors and making sitting targets of profitable, domestic export-oriented companies?

Facts & figures

In a similar vein, the five-year plan promises that substantial funds will be channeled to high-tech industries, meaning large corporations. At the same time, however, these are seen as a threat to the power of the party, as recent efforts to rein in selected domestic high-tech giants have shown. But the crackdown on the high-tech giants has been a blunder; it has alarmed Western financial investors along with many current and prospective industrial partners. China still needs to attract funds and companies from advanced countries, and unexpected regulatory moves are ill-advised for a recipient country. Will those high-tech funds in fact be used to create state champions, run by party bureaucrats, to compensate for the shortfall in Western investments?

Flip flop

The Chinese leadership must take strategic decisions that cannot be further delayed. Yet those in charge are hesitating, and their resolve is weakening – mostly in the monetary sphere. Early this year, the authorities announced they would take a new and more restrained monetary approach. In July, however, they did the opposite, once again engaging in generous money printing. What happened?

The Chinese economy has sailed through the pandemic months much better than most other countries. Yet the relentless rise in investment-led aggregate demand – encouraged by easy money and orders from the central authorities, combined with disruptions in global supply chains – has generated a rise in producer prices that in early 2021 became worrisome. It will not take much time before that translates into consumer price inflation.

Of course, a large increase in the money supply is not so harmful if the economy grows quickly and thus generates a rise in the demand for money: imbalances are modest, and prices remain more or less stable. Things take a different turn, however, if the economy slows down and the demand for money weakens. This is exactly the kind of scenario that worries Beijing.

China still needs to attract funds from advanced countries, making unexpected regulatory moves ill-advised.

A few months ago, policymakers felt they needed to react and had two possibilities. They could choose to ignore the inflationary threat; or, to cut wasteful investments, prevent inefficient companies from absorbing inputs that could be better employed elsewhere and make room for domestic consumption

Early this year, Beijing opted for the latter solution. A less generous monetary policy would have meant fewer or no subsidies for bad investments. Companies running wasteful (unprofitable) businesses would be allowed to go bankrupt. Of course, overall productivity would improve, even if the official growth figures would deteriorate. The downside, however, is that the bad companies would be shut down and create millions of unemployed workers, while many banks that handed out easy credit in the past would end up with large losses, possibly triggering a banking crisis.

China’s current rate of unemployment is about 5 percent, which may already be problematic, since the official statistics only consider urban areas. Unemployment in the rest of the country may be substantially higher. Unless the economy rises fast enough, killing bad projects and bad companies might take the rate of unemployment to intolerable levels. Moreover, a banking crisis may turn out to be another, possibly much worse headache. It would generate direct unemployment (in the banking industry) and lead to a credit crisis that might put out of business innumerable companies that are financially vulnerable but not necessarily inefficient.

Beijing’s grand geopolitical ambitions call for expensive infrastructure and easy credit handed to selected debtors.

More importantly, a banking crisis might trigger a bank run, with unimaginable economic and political consequences. The fallout of a monetary strategy designed to deal with inflation would pale in comparison with the consequences of banking panic.

Scenarios

The above helps us understand what we can expect going forward. Chinese policymakers have indeed acknowledged the presence of excessive liquidity and of too many bad projects and poorly managed companies. In early 2021, this led them to start fixing the imbalances accumulated through decades of fast growth and generous money printing. But, as mentioned, they recently backtracked and injected large amounts of cash into the system.

This can mean that Beijing believes growth is slowing down more rapidly than anticipated (or than is desirable); or that the banking industry is more fragile than had been originally estimated, or that uncertainty among the population is rising and that consumer price inflation is, after all, the lesser evil. Of course, all of these phenomena may be at work.

To be sure, unease in Beijing’s economic circles is rising – more than today’s current statistics reveal. As the recent regulatory blunder has shown, things tend to go awry when bureaucrats are under pressure. More erratic behavior is likely around the corner.