Geopolitics affirms gold as a key strategic asset

Surging precious metal prices are not mere market fluctuations, but a fundamental repricing of long-term risk and strategic value in an increasingly fragmented world.

In a nutshell

- States are hedging risk by increasing their holdings of gold

- Ballooning industrial demand is straining silver’s supply chains

- Producer countries are limiting exports of unrefined ores

- For comprehensive insights, tune into our AI-powered podcast here

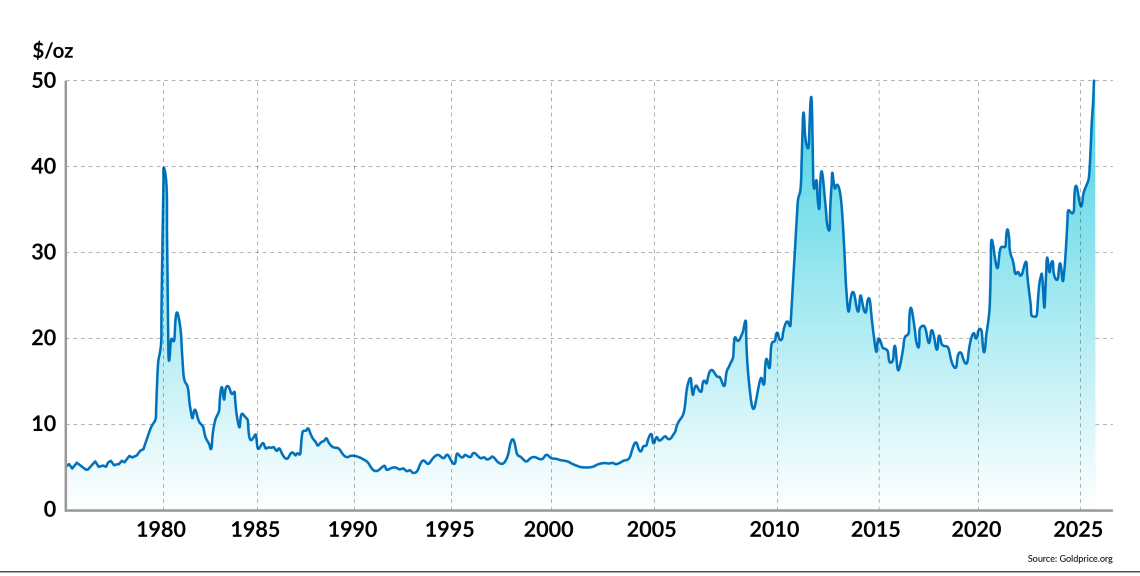

This year has proven to be a watershed moment for the precious metals market. Since January, gold, silver and platinum prices are up by roughly 60 percent, 75 percent and 80 percent, respectively, trading at unprecedented and persistent record highs. This is in addition to the price of gold having quadrupled, silver tripling and platinum doubling over the last decade.

The price of gold has been particularly noteworthy, breaching $4,000 per troy ounce in early October and rising to an all-time peak of $4,381, albeit retreating due to profit-taking, in the second half of the same month. Still, the recent series of record price levels has further boosted its status as the world’s most valuable individual asset, with a current market capitalization of around $28 trillion.

This places the metal far ahead of the global economy’s most valued company and second-most valuable single asset, Nvidia, with a market capitalization of around $4.5 trillion, not to mention the most popular cryptocurrency, Bitcoin, at $2.5 trillion. Even silver comes in as the world’s sixth-most valuable single asset at $2.7 trillion.

Arguably, traditional financial frameworks for valuing assets have proven inadequate to explain the surge in precious metals’ prices this year, following a steady yet relentless rise in prices ever since the gold standard was abandoned in 1971 when prices were fixed at $35 per ounce.

While conventional economic drivers like inflation and interest rates remain relevant in explaining some of the recent hikes in precious metals prices, their influence has become increasingly interconnected with a complex cocktail of geopolitical factors.

In short, this can be characterized by the decline of unipolar American hegemony and the economic and institutional stability it promoted, in contrast to the more contentious and politically volatile rise of a multipolar world order, exacerbated by U.S. President Donald Trump’s second administration.

The emerging nexus of economic security and strategic resources

In this evolving multipolar environment, gold, silver and platinum have transcended their traditional roles as hedges against inflation and economic uncertainty. These precious metals have adopted new geopolitical significance as safe havens at a time of elevated instability in respect to national security concerns and as anchors amid mounting sovereign and financial market risks.

Unlike other safe haven assets such as government bonds, which carry counterparty risk or fiat currencies that can be printed at will, the value of gold and other precious metals is not dependent on any single nation’s increasingly unreliable promises or self-serving policymaking.

Consequently, the most significant driver of precious metals purchases so far this year has been the accelerated and coordinated move − mainly by non-Western central banks, along with some from Western nations – away from the U.S. dollar and other major currencies toward increased holdings in gold and other precious metals.

This trend has been compounded by elevated private investor concerns over an increasing lack of global liquidity. This has fueled their demand for gold- and silver-based mutual funds to the extent that several finance houses have had to suspend inflows into their precious metals’ investment schemes.

Central banks have therefore become prominent actors in this trend. In 2025, some of the most strategic reserve managers have intensified their accumulation of gold as part of deliberate diversification and de-dollarization efforts.

Facts & figures

The price of gold has skyrocketed

This behavior arises not only from conventional portfolio risk management, but from geopolitical calculus. The symbolic and structural role of gold within sovereign balance sheets elevates its status beyond that of a mere commodity. Such purchases are less reactive to short-term price swings and more anchored in long-term reserve security.

The persistent use of Western currencies as a tool of foreign policy through sanctions has also instilled a deep-seated fear among non-Western countries, making vast dollar reserves now appear as a strategic vulnerability.

In response, central banks in the BRICS+ group, led by China and Russia, have embarked on the most aggressive period of gold accumulation in modern history. This is not merely diversification; it is a deliberate strategy to back potential new currency mechanisms.

The speculation throughout 2025 about a BRICS+ trade settlement system, partially backed by gold, among a basket of commodities, therefore partly explains the strategic buying by non-Western central banks and private investors.

A significant outcome of this state-level demand for precious metals has been the creation of an informal price floor that is sucking vast quantities of physical gold into state vaults. In turn, this is reinforcing the institutionalization of gold and precious metals as strategic assets. Trade policy volatility has also played a significant role, especially for metals like silver and platinum whose supply chains and production are more globally integrated and sensitive.

Gold and precious metals are being perceived as the foundation for a new global financial and multipolar political architecture by an increasing array of central banks and private investors.

The reactivation of aggressive U.S. tariffs under the Trump administration, particularly on metals and inputs, has introduced fragmentation in sourcing networks. Countries reliant on export or import flows for silver or platinum intermediates now face tariff risks and more dispersed supply chains.

As trade blocs coalesce and tariffs rise, the cost and complexity of moving metals globally increase. This fragmentation further contributes to upward pressure on precious metal prices, while exacerbating supply tightness.

The end result is that countries are implicitly linking their economic security to their holdings of critical or strategic commodities, of which gold, silver and platinum are the most sought after as a neutral medium of exchange and trusted store of value.

At its most extreme incarnation is Russia, where gold has become a core component of its financial defense, in the form of a liquid, universally accepted asset that exists outside the Western-controlled banking system.

In short, gold and precious metals are being perceived as the foundation for a new global financial and multipolar political architecture by an increasing array of central banks and private investors. This order is based on linking economic security to holdings of a diverse set of strategic commodities, not controlled or dominated by any single nation state.

Industrial supply constraints

In the silver space, political volatilities in mining jurisdictions have compounded geopolitical pressures. Peru, a key silver producer, experienced labor strikes and social unrest in 2024, which curtailed output and sowed further risk into 2025.

In China, proposals to raise mining royalties have injected tension between foreign capital and state regulation, threatening new investments. Meanwhile, Russia’s pivot into blocs free of direct Western influence has disrupted silver’s traditional pricing linkages and export pathways.

Because much of silver is a byproduct of base metal mining, producers have limited flexibility to ramp up output purely to satisfy silver demand. These geopolitical, regulatory and practical headwinds have further exacerbated issues surrounding the metal’s surging industrial demand. This, in turn, leads to deeper supply deficits, drawing down inventories and intensifying speculative interest.

Facts & figures

Silver benefits from geopolitics and industrial demand

Platinum’s rally represents perhaps the most intriguing intersection of geopolitical fragility and industrial resurgence. The metal has long been overshadowed by gold and palladium, but in 2025 it has reemerged in force.

A crucial underlying driver is the fragility of supply, particularly in South Africa, which accounts for a large share of global platinum production. The country faces chronic structural risks: rolling power blackouts, aging infrastructure, regulatory unpredictability, labor tensions and investment stagnation.

In 2025, these effects have deepened and production declines have become more pronounced. As investors internalize the geo-operational risk within the supply base, the notion that platinum could be a “scarcity play” has gained traction.

Simultaneously, with rising industrial demand from the automotive sector, catalysts, chemical applications and nascent hydrogen/fuel-cell uses, platinum’s skyrocketing price has benefitted from both scarcity fear and forward-looking industrial demand.

Another dimension is the geopolitics of the energy transition. The global push for net-zero carbon emissions has collided with a supply side constrained by years of underinvestment, creating a severe structural deficit. This has been exacerbated by nations competing in the green transition, increasingly considering control over upstream inputs, such as silver and platinum, as vital strategic assets.

Silver, given its unparalleled electrical conductivity, has become an indispensable component for photovoltaic solar cells, electric vehicles and 5G infrastructure.

Platinum, as the essential catalyst in electrolyzers and fuel cells, has acquired critical status in the race for green hydrogen, with major economies committing billions of dollars to its infrastructure.

The interplay between supply constraints and strategic resource control thus adds a further geopolitical premium into precious metal valuations.

Resource nationalism

One of the more under-appreciated geopolitical themes playing out in 2025 is strategic resource nationalism. Governments in key producing jurisdictions have grown reluctant to allow unfettered export of precious metal resources.

Administrations in countries with significant mining industries have increasingly deployed geopolitical leverage in exploiting their metal reserves, often leading to discretionary export policies aimed at influencing the global supply.

Read more on central bank reserve strategies

- The old developed world is in denial

- Reassessing the dollar’s global status

- What is really fueling the new gold rush?

This phenomenon has been exacerbated by the concentration of supply in Global Majority states with developing economies. For instance, as a significant portion of platinum comes from infrastructurally unstable South Africa, silver markets rely on mines in regions like Mexico and China, two countries which have come under significant pressure from American tariffs, creating a constant resource-nationalism risk.

Control over mining concessions, export restrictions, royalty hikes and local beneficiation rules have also emerged as levers in broader economic and geopolitical strategies.

When export caps or stricter regulations loom, markets interpret such moves as latent supply squeezes and pricing begins to internalize “optional supply risk.” This dynamic is particularly relevant for platinum and silver, where production is more geographically concentrated.

Looking through geopolitical volatility

Geopolitics is not always linear, as periods of geopolitical de-escalation or resolution can trigger sharp reversals. Indeed, in 2025 there have already been moments where easing tensions – say, diplomatic thawing or ceasefires – have prompted temporary softening in gold and silver prices.

However, given the structural nature of many risk vectors – debt stress, regional military tensions, trade bloc divides or supply chain reorganization – the default state of affairs has been one of heightened stress rather than calm equilibrium.

Facts & figures

Implications of the precious metals’ rally

The precious metals rally in 2025 has not merely been a speculative breakout – it is embedded in a deeper transformation of the global financial and geopolitical architecture. The surge in demand for gold, silver and platinum reflects more than portfolio repositioning: It reveals a long-term transition toward a risk-conscious, fragmentation-aware global regime in which real, non-counterparty assets have gained new strategic weight.

Another geopolitical tailwind has been the effect of precious metals’ ranking in foreign exchange reserves among nations. As relative power shifts, reserve managers in smaller or peripheral states may feel compelled to emulate the reserve strategies of their counterparts in major economies.

If the leading central banks accentuate gold in their reserves, smaller or allied central banks may follow suit for signaling purposes and strategic posture. This “reserve convergence” dynamic is likely to have amplified demand from emerging markets as geopolitical blocs or actors have realigned, and that is likely to continue.

Scenarios

More likely: Entrenched multipolarity and managed rivalry sustains high gold demand

The world continues its gradual but irreversible consolidation into a multipolar order. The strategic competition between the U.S.-European bloc and certain members of the expanded BRICS+ coalition persists as a defining feature, characterized by managed rivalry rather than direct, open conflict.

This environment sustains a methodical and persistent drive towards de-dollarization. Several BRICS+ nations, along with other non-aligned Global Majority states, continue to accumulate gold and precious metals as a core component of their monetary reserves, not for a single explosive challenge to the dollar, but to build strategic autonomy and reduce their vulnerability to Western financial sanctions and other geopolitical measures. This creates a steady, structural demand for gold at the state level.

Concurrently, the green energy transition and the race for technological supremacy continue to fuel a form of resource nationalism. Nations will increasingly view secure supplies of strategic metals like silver and platinum as a matter of economic and national security. This will lead to policies that prioritize domestic supply chains and secure foreign sources, thereby keeping geopolitical risk premiums firmly embedded in these markets.

Less likely: Gold valuations plateau amid a thaw in geopolitical tensions

The price of gold stabilizing involves a partial, though significant, reversal of current trends. A combination of war fatigue, economic necessity and diplomatic breakthroughs lead to a de-escalation in key flashpoints like Ukraine and the Taiwan Strait.

A renewed, albeit fragile, commitment to multilateralism and global trade cooperation emerges. In this environment, the urgent imperative for de-dollarization loses its immediate momentum. The perception of the U.S.-led financial system as a direct tool of geopolitical coercion diminishes, reducing the frantic, strategic motivation behind state-level gold accumulation.

Furthermore, a thaw in relations would ease the pressure of resource nationalism, allowing for a more cooperative and globalized approach to sourcing industrial metals like silver and platinum. While the long-term trends of the energy transition remain, the specific geopolitical risk premiums attached to these metals would notably erode, refocusing market attention more squarely on their pure supply-demand fundamentals.

Least likely: Acute fractures result in gold becoming the centerpiece of a new financial system

This is a tail-risk scenario involving a rapid and disorderly unravelling of the current international order. A trigger event – such as a catastrophic military confrontation or the formal establishment of a rival, gold-backed financial bloc by an adversarial coalition – shatters the existing framework.

This would lead to a full-scale financial and technological decoupling between competing geopolitical spheres. In this paradigm, precious metals would undergo a fundamental repricing not as commodities, but as foundational monetary and strategic assets.

Gold would be thrust into the role of a neutral, non-sovereign monetary anchor in a period of extreme currency instability and a collapse in trust between major powers. Simultaneously, silver and platinum would transition from being traded industrial commodities to critically scarce strategic resources.

Precious metals’ supply chains would be weaponized or severed by export controls and access to them would be treated as a vital national security interest on par with energy or food security, leading to a frantic, state-driven scramble that would transcend traditional market dynamics.

Contact us today for tailored geopolitical insights and industry-specific advisory services.

Sign up for our newsletter

Receive insights from our experts every week in your inbox.