Global Outlook 2018: Dangerous waters ahead for the world economy

All around, the wind seems to have filled the sails of the world economy. From consumer spending to investment to stock market indices, the sailing seems smooth. But some dangerous currents, including debt-fueled liquidity and low productivity, are converging below the surface.

In a nutshell

- High levels of debt-fueled liquidity are powering the global economy

- Productivity does not match the levels of investment

- When interest rates rise and investors pull back, it could cause a crisis

Will it be smooth sailing for the global economy in 2018? At a first glance, it seems so. Finally, the world’s regional economies all seem to be in sync. Financial markets are soaring. Consumer spending is on the rise. Companies are buying back their own shares. However, beneath the surface, dangerous currents are converging.

Pleasure cruise

For the moment, the wind is in the world economy’s sails. The International Monetary Fund (IMF) estimates worldwide gross domestic product (GDP) growth for 2017 at about 3.6 percent. For 2018, the forecast is 3.7 percent. These rates are only slightly below the global average ahead of the 2008 crisis. Other data are positive, too. Consumer confidence keeps mounting, and there is more private investment.

Take a look around. In China, fears of a “hard landing” have vanished. There is no landing at all – the projected and reported economic output match the planning bureau’s predictions. In Japan, deficit spending seems to be showing results. Expansive monetary policies worked so well in the European Union and the United States that central bankers openly allow themselves to think about restoring normalcy. The U.S. is tentatively attempting to do so. Even South Africa, Russia, Brazil and Argentina are recuperating from the gloom of past years.

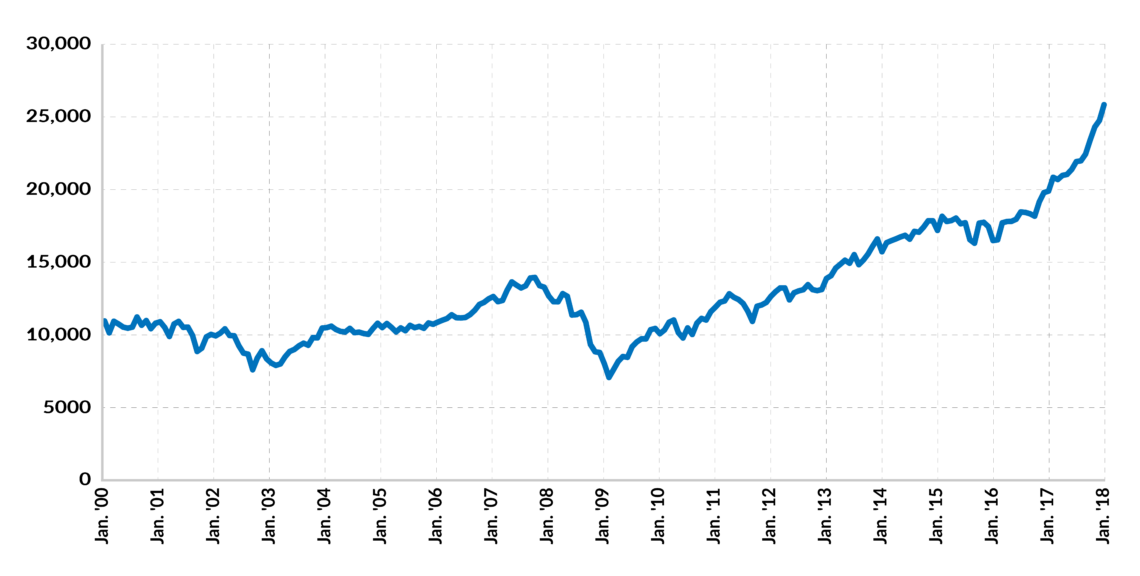

Many stock market indices are now higher than they have ever been.

Financial markets are happy all around. Before the 2007 meltdown, the Dow Jones Industrial Average was barely above 14,000 points; today, it has passed the 25,000 mark. Stock market indices like London’s FTSE, Frankfurt’s DAX and Tokyo’s Nikkei, among others, are now far higher than they have ever been. Granted, there are fewer structured products around, but newer products have emerged instead. Exchange-traded funds, indexed vehicles, futures and blockchains are among them. They are not less complex than their structured siblings were. In the financial sector, imagination is still alive and well.

In a word, the world economy is not a tight ship, but a pleasure cruise on calm waters. But is that the whole story?

Trouble brewing

Beneath the surface, dangerous currents are gathering. Viewed from above, it might even seem simple to navigate around them. But once the ship gets caught in these currents, it is very hard to break loose. In fact, it is even more probable that it could be dragged down by these forces from below. What are these nefarious underwater tides? Three main factors should preoccupy the captains of the world economy:

Liquidity

In recent years, governments have been flooding economies with discretionary spending, which central banks have been bankrolling. On top of that, banks have continually been expanding the global economy’s total debt. Apparently, these liquidity flows into the system have been working well. But what happens when the flow is curbed or even reversed?

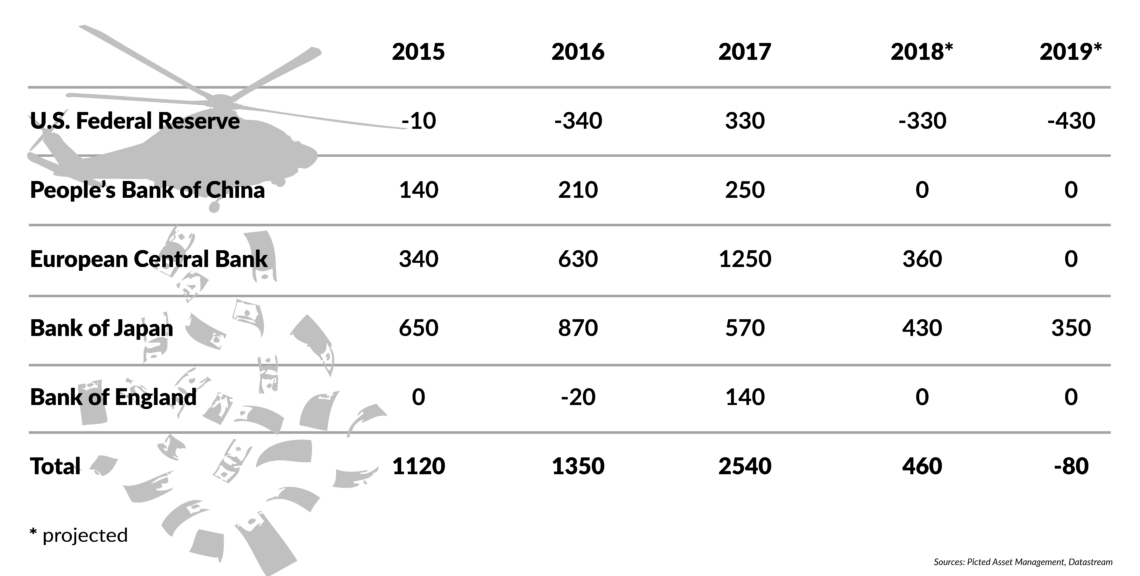

In 2017, the five largest central banks on the planet – the U.S. Federal Reserve, the European Central Bank, the People’s Bank of China, the Bank of Japan and the Bank of England – injected some $2.5 trillion into the world economy. But in 2018, they are planning to curb the flow to “only” an additional $460 billion. And for 2019, a reversal has been announced. They forecast taking some $80 billion out of the economy.

Facts & figures

Liquidity: high tide, low tide

Liquidity pumped into the economy by the five largest central banks

On one hand, those who favor fiscal and monetary discipline should applaud this move. But on the other, there is the question of how the global economy will fare with reduced or no additional liquidity. When central banks reverse their policies, interest rates are bound to rise. Markets will be faced with more expensive capital. This will lead to a general reevaluation of consumption and investment. Pressure will rise on holders of capital, on debtors and on the objects of investment.

This pressure will most probably lead to a reevaluation of the productivity of investments, as seems only logical. But the problem is: worldwide, labor and capital productivity have slowed down significantly over the past decade, according to the Organisation for Economic Co-operation and Development (OECD).

There are several explanations for this. It might be that the world economy’s structural shift away from manufacturing and toward services allows for economic growth without an increase in productivity growth. It could also be that continuing automation and digitization have lessened the need for labor efficiency.

Investments are being measured more by how much money they absorb than by the returns they produce.

But there is also a more worrying explanation. With near-zero interest rates and a massive inflow of liquidity into the economy, investments are not being measured by the yields they produce. See, for example, the massive financing of some “sharing economy” businesses or the corporate share buyback programs. The returns on these ventures are even lower than average productivity growth. However, they are higher than interest rates. In other words, investments are being measured more by how much money they absorb than by the returns they produce.

This leads to bad investments. And with rising interest rates and monetary tightening, investors will reevaluate their interests and direct their capital into the (few) projects that yield a decent return. They will leave behind companies depleted of money (think the dot-coms of the early 2000s) and unfinished projects (think of the ghost towns in the U.S. and China: never finished, never inhabited). And since interest rates climb more quickly than productivity can catch up, the process frequently results in economic crisis.

Adjustment from bad investments occurs through the reduction of capital stock, that is: investors lose money. It is problematic enough to lose one’s own money, but losing capital that has been built up by debt is even worse. Not only the investor’s capital is diminished, but also the creditor’s, creating risks of contagion and default.

Defaults, by the way, are far from uncommon. They are tacitly happening in many economies. In the U.S. and Switzerland, pension plans cannot keep up with the demography; they devalue their liabilities. Greece, Italy and Japan operate without honoring the full coupon on their public debts and without paying back the borrowed money in full. Argentina and Brazil had “haircuts” on several of their internal and external debts. China forces its state-owned banks to roll over the debt of municipalities and provinces. In some financial markets, there is considerable asset-price inflation. These are all examples of default.

In 2017 the global debt burden shot up to 320 percent of its economic output.

The size of the debt – and potential default – is impressive. In 2016, the world’s debt burden equaled 170 percent of its economic output. By 2017, that proportion shot up to 320 percent. These numbers do not include the financial agents, who are, with a grain of salt, net debt.

Currents converge

These three factors are set to converge. The massive inflow of liquidity into the world economy has been driving economic growth. It is, however, largely financed by debt. Without productivity being able to catch up with the rate of debt-driven liquidity inflow, there is a considerable risk of bad investment. When this flow stops or reverses, investors will readjust their allocation of capital. Capital stocks will diminish and, if they were based on debt, contagion and default will occur. The global economy’s ship will get caught in the currents and will be pulled under.

At first glance, the world economy is doing fine. The underlying problems it faces have not, however, been addressed in the last decade. If anything, they have worsened. So far, there have only been tentative attempts to address some of them. One worst-case scenario would be for the effects of easy money to wane, without the structural imbalances being contained.

A last remark for all officers on deck: even if one does not believe in capital theory, the global economy has been growing for seven consecutive years. Eventually this cycle will come to an end. After all, even the most splendid sun on the south seas must occasionally make room for a monsoon.