Modern Monetary Theory is no cure for the savings-shortage illness

As the pandemic-induced crisis pushed the U.S. national savings rate into negative territory, the country has become even more dependent on capital inflows from abroad. Investors from China are no longer welcome on American shores. Where will all that money come from?

In a nutshell

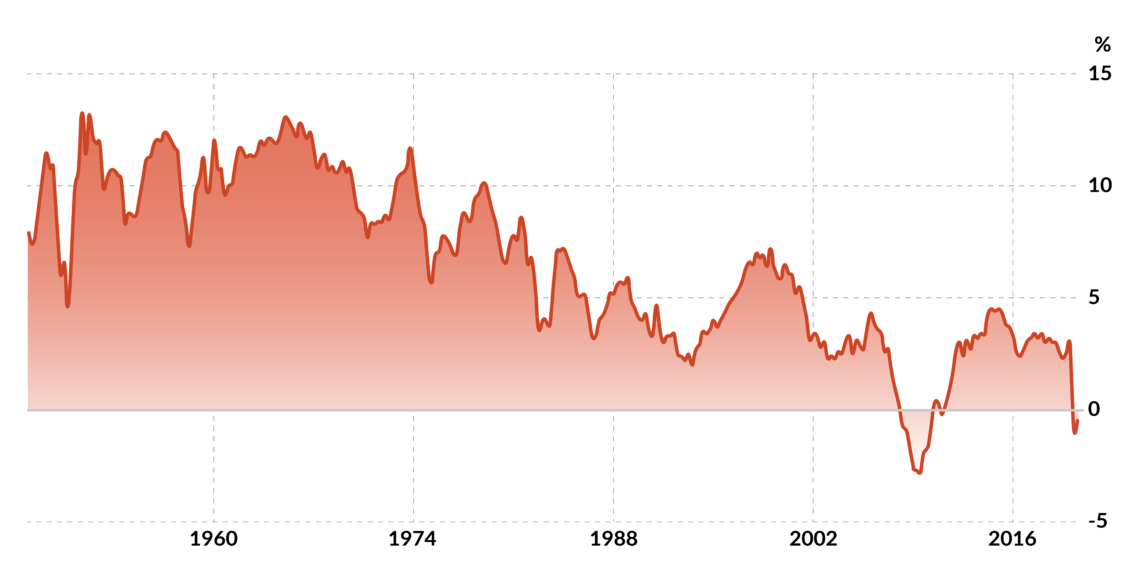

- The U.S. national savings rate sunk to -0.9% in the second quarter of 2020

- Capital from abroad used to compensate for low domestic savings

- At present, Europe lacks sufficient savings to replace Chinese investors

Prince Michael of Liechtenstein contributed to this opinion.

The turmoil brought on by the Covid-19 pandemic, which continues to rattle and confuse global markets, has camouflaged a cataclysmic problem that will wreak havoc on the United States economy for decades to come. The effects of historic deficit levels in 2020 will cause a further U.S. savings drop, to depths rarely seen before.

New data from the U.S. Federal Reserve shows that the rate of net national savings – the sum of domestic savings by households, businesses and government – was -0.9 percent in the second quarter of 2020, sinking an astonishing 131 percent from the previous quarter. The last time that the savings rate turned negative was back in 2009, when it fell to -2.7 percent. However, that happened when the global recession was at its zenith.

The problem does not lie solely in the dangers of recklessly amassing government debt. The drastic drop in national savings, too, carries severe implications for the U.S. economic landscape.

Unyielding macroeconomics

Soon, a steeper decline of the savings rate could accelerate the U.S. dollar’s weakening and trigger an even more prodigious expansion of the U.S. trade deficit. In a downward spiral, the potent, destructive combination of a weak dollar and massive trade deficits will only gain strength as net savings continue to sink into negative territory.

The critical question is, where is this additional foreign capital to come from?

International investors should be watching these developments very closely, as a new role for foreign capital is emerging. This is because any deficiency in net national savings must be filled by foreign capital to make up for the difference between net U.S. investment and net U.S. domestic savings.

When an economy lacks a sufficient domestic source of funding for investments and capital-stock upgrades, the money must come from larger net inflows from abroad. Consequently, the expanding negative U.S. savings rate creates a rising dependency on foreign capital inflows to fund U.S. investment.

The critical question is, where is this additional foreign capital to come from? The previous solutions, such as running high trade deficits to attract Chinese capital, contradict Washington’s new trade policies and national security priorities.

Washington’s bind

The Trump administration has been steadfast in trying to address its various grievances over China’s trading practices. The White House touts its “tough on trade” approach, epitomized by higher U.S. tariffs on more than $360 billion worth of Chinese goods. However, this policy reduces China’s trade surplus, which ballooned when the Americans welcomed capital from that country.

More importantly, Washington has imposed a plethora of restrictions hindering Chinese investment in the U.S. That geopolitical calculation has inherent economic ramifications. Over recent years, the U.S. government has decided that it can no longer accept how Beijing uses its trade profits. There is bipartisan consensus in Congress that China cannot be allowed to continue expanding its foreign influence and accelerating its military capabilities by rigging trade rules, capturing technologies and gaining access to sensitive Western industries.

The Covid-19 pandemic and the development of the ‘green’ economy serve as excuses for governments to accumulate limitless debt.

The negative U.S. attitude is not likely to shift with the arrival of President-elect Joe Biden’s administration. The Americans now perceive China’s enormous dollar reserves as a national security threat. They are actively working to restrict the scope and depth of Chinese investments in their country. From Treasury Secretary Steven Mnuchin invoking national security considerations to force TikTok (whose parent company is Chinese) to sell its U.S. business, to Congress drafting a rare bipartisan bill that would allow for removing Chinese companies from U.S. stock exchanges if they deny regulators access to their audits – evidence is plentiful that the Americans no longer welcome China’s capital inflow.

With China out of the picture for geopolitical reasons, the only viable alternative could be increased investments from Europe. However, the eurozone also has alarmingly low national savings rates. The problem is likely to increase as the European Central Bank deliberates unorthodox monetary tools and fiscal stimulus packages. On top of that, the European Union has its own quarrels with Washington over steel and aluminum duties and over American retaliatory tariffs on $7.5 billion worth of European goods imposed in response to allegedly illegal Airbus subsidies.

False solutions

There is no simple answer to where the U.S. can access the additional foreign capital it needs to meet its investment requirements as domestic savings drop at alarming rates. The system that worked for a long time – siphoning savings from abroad for investments in the U.S. – will eventually come to a stop. The U.S. faces a unique combination of headwinds not found in other countries. Making matters worse, the Congressional Budget Office estimates that the federal budget deficit reached 17.9 percent of GDP in 2020. This is a new peacetime record.

Yet policymakers from Washington to Brussels are debating more stimulus packages rather than exploring ways to increase national savings. The alarming attitude includes the recent spike in popularity of the so-called Modern Monetary Theory, which argues that governments issuing debt in their own currency do not have to worry about large deficits. Acceptance of this concept would swiftly lead to the evaporation net domestic savings. The Covid-19 pandemic and the development of the “green” economy serve as excuses for governments to accumulate limitless debt, financed by central banks.

Outlook

The problems emerging in the U.S cast light on the complex challenges that arise when governments adopt a reckless budgeting philosophy and abandon fiscal responsibility. Large government deficits cause national saving rates to plummet, expanding foreign capital’s role in bridging the country’s domestic investment needs. As net foreign inflows rise to make up for the drop in net savings, the trade deficit inevitably expands, reducing GDP by a corresponding amount.

The savings rate directly translates into economic strength. While such relationships may appear highly technical, they shed light on how a nation’s savings are connected to investment activity, trade policies and finally, economic prosperity.

Modern Monetary Theory is an intellectual travesty, fool’s gold. Embracing it might buy the profligate governments a bit more time, but that will inevitably create only a heavier liability burden for the future.