Prospects for the yuan unseating the dollar

China has made significant progress in strengthening the yuan’s status, but it will not soon become the dominant global reserve currency.

In a nutshell

- The Russia-Ukraine war has put new scrutiny on the dollar’s role

- A diversification of global currencies is ongoing, but won’t displace the dollar

- The yuan’s rise hinges on China’s economic growth

When leaders of the BRICS group of emerging economies – Brazil, Russia, India, China and South Africa – convene at a summit in Johannesburg this week, de-dollarization and the establishment of a common currency will be at the top of the agenda.

Across Southeast Asia, Africa and the Middle East, there are now concerted efforts to diminish the influence of the United States dollar. As the world’s largest trading nation, China has championed the internationalization of the yuan for several years. The Russia-Ukraine conflict appears to have elevated the status of the Chinese currency. Does this all signal a major challenge to the global order predominantly led by the U.S., especially in the economic and financial spheres?

Answering this question requires examining the roots of the U.S. dollar’s dominance, how members of the so-called Global South perceive it, and the dynamics of international currencies. One must also look at the motivations for de-dollarization for different countries, and assess the potential of the yuan to replace the dollar.

What makes a global currency

An international currency must have three features: a valuation function, to settle trade based on transaction demand; a payment function; and a storage function, to serve as a reserve asset for global central banks and a dependable asset for private investors, banks and other institutions.

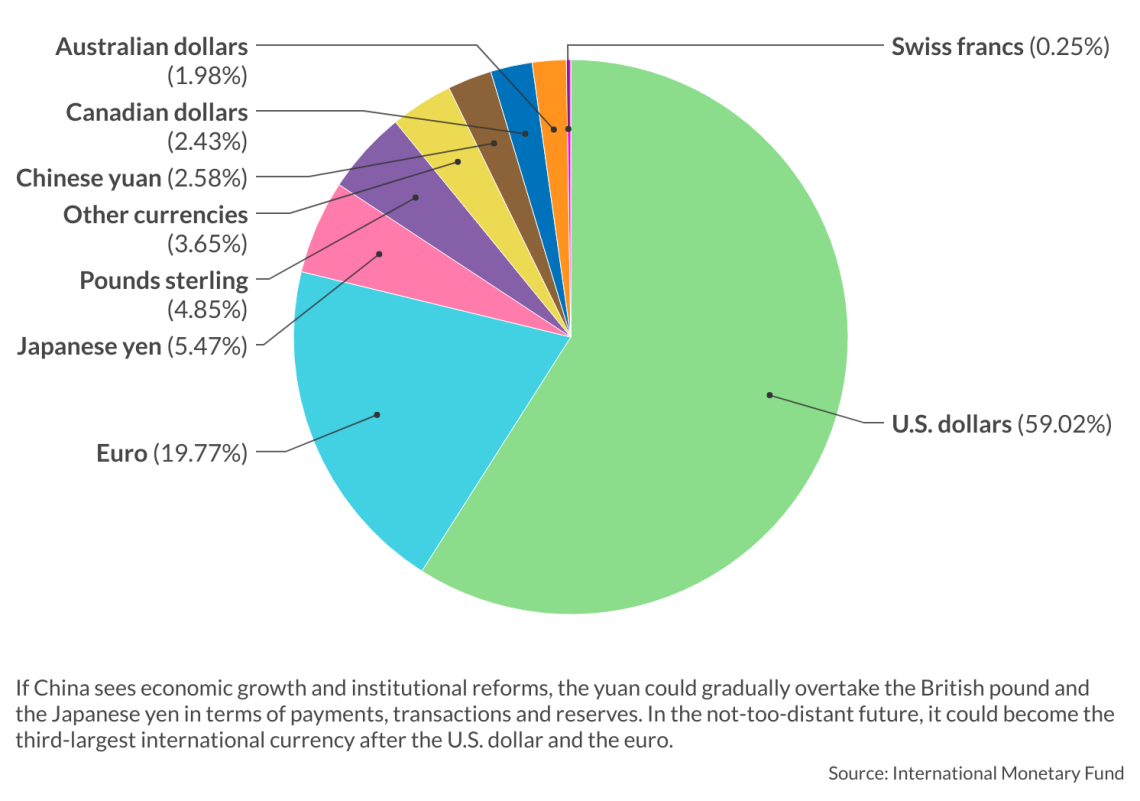

The dollar achieved supremacy by embodying these three functions – especially the asset storage role, which is more important than the trade role. In terms of safety, the dollar has no rivals. According to the International Monetary Fund (IMF), at the end of 2022, the dollar accounted for 58.36 percent of global foreign exchange reserves. This was followed by the euro at 20 percent, the yen at 5.5 percent, and the pound at 4.9 percent. The yuan occupied the fifth spot, accounting for 2.7 percent. With regard to global trade in 2022, 88 percent was transacted in U.S. dollars, 31 percent in euros and a mere 7 percent in yuan.

Historically, the dollar’s supremacy has also been backed by its economic strength and military power. The U.S. accounted for 50 percent of global gross domestic product (GDP) in the post-World War II period (a share now down to 20-25 percent). When President Richard Nixon announced the decoupling of the dollar from gold in 1971, the dollar went in search of a new peg. The White House dispatched Secretary of State Henry Kissinger to the Middle East to secure a deal, with two objectives: that oil transactions be settled in dollars, and that the dollars flowing to oil producers be deposited in American banks, to buy American bonds. In return, Washington would provide Saudi Arabia with military protection and would not require the kingdom to democratize. This is how the so-called petrodollar was born; since then, several commodities around the world have been settled in U.S. dollars.

More on the dollar

Reassessing the dollar’s global status

So far, the dollar has managed to maintain its dominance, with a relatively high rate of return on investment and unmatched liquidity in terms of storage. The U.S. remains the world’s largest economy, and global payment systems employ the American payment system.

Of course, the greenback is not without its problems. Other countries have complained about the tendency to “weaponize” the dollar, undermining their confidence in it. This is partly responsible for its share among global reserves falling from 70 percent to 58 percent over the past 20 years. To punish Russian aggression in Ukraine, the Biden administration suspended Russia’s use of the SWIFT international payment network, preventing its central bank from using its foreign exchange reserves. Amid trade friction with China, and bipartisan bickering in Washington over fiscal issues and other factors, Fitch Ratings recently downgraded the U.S. long-term credit rating. Nevertheless, as long as the American economy is strong, the dollar’s dominant position will be difficult to shake.

Motivations for de-dollarization

Calls for de-dollarization have been heard for decades. As early as 1965, then-French finance minister Valery Giscard d’Estaing denounced the “exorbitant privileges” of the dollar. The global financial crisis of 2007-08 further questioned the hegemony of the dollar, as well as the monetary and fiscal discipline of the U.S., and these concerns have reemerged with the Russia-Ukraine conflict.

In fact, there are currently two distinct types of efforts toward de-dollarization. After the outbreak of war in Ukraine, in addition to the weaponization of the dollar, the freezing of Russia’s currency reserves was seen as an unprecedented tool of extraterritoriality. In response, Russia has sought to unchain its ability to trade – as has China, to avoid the possibility of being similarly trapped. Both countries have tried to use their economic clout and resources to dethrone the dollar, and fundamentally revise the global financial system. This is the first type; Russia and China are a minority, but a powerful one.

The question for Beijing is how to increase the internationalization of the yuan, rather than simply trying to promote de-dollarization.

The second group of countries are pursuing a broader concept of economic independence. When a country uses the dollar, it effectively surrenders part of its economic sovereignty to Washington, which alone enjoys the right to print dollars and set U.S. monetary policy. This second kind of effort includes a number of members of the Global South.

Yet these countries are largely not ready to abandon the dollar altogether. For example, Brazil – which has reached an agreement with China to use the yuan for trade – transacts with China in dollars before trading in both currencies. In other words, Brazil still relies on the dollar as a benchmark, because it does not believe that the yuan is the more stable currency.

How the yuan measures up

Today, the yuan is the world’s fifth-largest payment currency, the third-largest trade financing currency, and the fifth-largest international reserve currency. Yuan foreign exchange transactions have increased to 7 percent of the global market share, making it the fastest-rising currency in the past three years. But the low proportion of yuan used in trade settlements does not fully reflect China’s status as the top trading nation.

To promote the internationalization of the currency, through 2022 the People’s Bank of China had authorized 31 yuan clearing banks in 29 countries and regions. In 2018, it set up its own commodities exchange, the Shanghai International Energy Exchange (INE), for oil deliveries from countries like Iran, Venezuela and Russia. Contracts traded on the INE use only yuan. Major oil exporter Saudi Arabia recently expressed openness to the idea of trading in currencies other than the dollar. And this March, France struck a deal to trade liquefied natural gas with China and settle cross-border payments in yuan rather than dollars. The move set a precedent for U.S. allies in Europe to pay in a different local currency. With Russia’s invasion of Ukraine, the yuan greatly increased its role in Sino-Russian trade.

China has developed its own international payment platform – the Cross-Border Interbank Payment System (CIPS) – that is independent of SWIFT and accepted not only in Russia but by banks in Brazil and elsewhere. As of January, yuan savings accounted for 11 percent of Russia’s total deposits, making it the most traded currency in the country. Of course, CIPS and SWIFT do not play the same role in international finance. SWIFT is a secure global messaging system that provides banks with efficient, low-cost communications and does not transfer funds; while CIPS is a yuan-denominated clearing and settlement mechanism that usually requires SWIFT messaging for cross-border transactions.

However, the yuan has many drawbacks. Lack of convertibility remains an obstacle for many global investors. The ability to control capital flows remains extremely important for Chinese authorities. Without it, large amounts of capital will flow out of China in search of safety. A fully internationalized yuan is unlikely to happen unless Beijing allows greater currency freedom and both inward and outward investment, and fully establishes the rule of law.

Today’s yuan is not ultimately free from the shadow of the dollar. The key to its internationalization is how much foreign exchange reserves Beijing has in hand: being bound to the U.S. dollar is the most powerful force making China’s currency global. Without this premise, the yuan could become wastepaper in the international arena.

Scenarios

The primacy of the dollar has remained largely unchallenged. But recent developments, like economic sanctions imposed by the U.S., are contributing to ongoing de-dollarization efforts, which in turn may lead to a prolonged depreciation of the dollar.

The dollar’s dominance will slowly begin to erode, but it is unlikely to end overnight. There is currently no real global alternative, and both the euro and the yuan face their own problems. Neither China nor the BRICS group will be able to snatch the dollar’s crown, but they can shrink the territorial scope of its domain.

The question for Beijing is how to increase the internationalization of the yuan in a substantial way, rather than simply trying to promote de-dollarization. To do the former, it will have to enact a thorough overhaul of its economic system and turn China into a genuine rule-of-law state.

One possible catalyst for de-dollarization lies in emerging technologies such as blockchain and digital currencies. Blockchain tools and digital currencies have key attributes such as neutrality, efficiency and programmability, which can support new financial applications outside the traditional financial system. Using these technologies, countries attempting to build alternatives to U.S.-controlled financial infrastructure can offer advantages in terms of cost, efficiency, ease of use and utility. At the same time, supplanting the dollar would still require building a robust legal environment, economic strength, military power, technological prowess, and a whole new set of global financial systems. It is hard to imagine this happening within the next 10 or 20 years.

Still, the diversification of international currencies is ongoing. According to the IMF, by the end of 2020, 46 economies had allocated more than 5 percent of foreign exchange reserve assets to the yuan or to those outside the basket of “special drawing rights” currencies (the dollar, yuan, euro, yen and pound sterling).

The yuan is undoubtedly among the best of the nontraditional currencies. If China’s economy manages to improve after the second half of this year, and progress is made with institutional reform, the yuan is expected to gradually overtake the British pound and the Japanese yen in terms of payments, transactions, and reserves. In the not-too-distant future, it could become the third-largest international currency after the U.S. dollar and the euro, and a key element in a three-pronged international monetary system.

For now, however, no one can guarantee stable growth of the Chinese economy. If Chinese growth keeps decelerating, the pace of yuan internationalization and de-dollarization will also be greatly slowed.

Sign up for our newsletter

Receive insights from our experts every week in your inbox.