Charting the course of Africa’s aviation sector

A growing middle class, increasing continental integration and huge economic potential all provide reason to be optimistic about the future of Africa’s aviation sector. Yet many governments still see the industry as a cash cow or point of national pride.

In a nutshell

- The African aviation market has significant potential

- Liberalization would benefit African passengers and economies

- Airlines that do not embrace liberalization will struggle

While Africa accounts for 20 percent of the world’s landmass and is home to nearly 17 percent of its population, its aviation industry represents only 3 percent of the global market. In 2018, the sector contributed $80 billion to the continent’s gross domestic product (GDP), supporting 6.9 million jobs. Yet compared with other continents, aviation in Africa lags in terms of traffic, capacity and connectivity. Globally, the industry is entering what is expected to be its 11th consecutive year of growth. African airlines, however, together registered losses of around $200 million in 2019.

Given current economic, demographic and geographic trends, Africa stands as the last frontier of commercial aviation, and the market there is set to expand over the next several years. A combination of political and economic decisions, changes to policy and regulatory frameworks, and global factors will shape this growth.

Growth drivers

The African aviation industry has gained substantial momentum of late, even despite the financial losses. After the overall failure of the 1999 Yamoussoukro Decision (when 44 African countries agreed to remove regulatory barriers), the Single African Air Transport Market (SAATM) was launched in 2018, bringing a new commitment to liberalization of the sector. A flagship project of the African Union, the SAATM aims to create a single unified air transport market on the continent. So far, 28 countries have committed to the agreement (representing more than 80 percent of Africa’s aviation market); 10 of these have already implemented all of the concrete measures envisaged by the SAATM.

While the liberalization of air markets does not come without collateral damage, it has an overall positive impact.

However, important players – including countries like Uganda and Tanzania, as well as some Nigerian airline operators – have been resisting liberalization, claiming that increased competition on what they consider an uneven playing field would benefit consolidated airlines, to the detriment of other carriers.

Experience suggests that while the liberalization of air markets does not come without collateral damage, it has an overall positive impact for the industry, the economy in general and passengers in particular. Factors specific to Africa could accelerate the positive effects: the implementation of the African Continental Free Trade Agreement (AfCFTA); the ongoing adoption by several countries of less restrictive visa policies; the possible creation of an African Union passport, aimed at facilitating the free movement of people across the continent; and Africa’s fast-growing tourism market. In 2018, the African tourism industry grew by 5.6 percent, the second-fastest rate in the world. For comparison, the global average growth rate was 3.9 percent.

Facts & figures

African aviation market data

- With 92 million passengers, in 2018, Africa accounted for just 2.1 percent of global passenger traffic (IATA, 2019)

- International tourist arrivals into Africa increased by 7 percent in 2018, totaling 67 million

- The continent is home to about 731 airports (320 of which international) and 419 airlines

- Africans can afford around 1.1 air tickets per year on average, significantly fewer than in Latin America (5.4) and North America (33) (AfDB, 2019)

- Passenger distribution in African airlines: 51.05 percent intercontinental; 27.62 percent intra-African and 22.41 percent domestic (AFRAA, 2019)

- Ten airlines (including global carriers) that operate to and from seven African cities account for 80 percent of the African aviation market

- Out of Africa’s 10 most lucrative air routes, only two are operated by African airlines (South African Airlines Johannesburg-Cape Town and TAAG Luanda-Lisbon)

- The most profitable route ($837 million) is Johannesburg-Dubai, operated by Emirates

- Africa’s busiest airports by passenger flow are Johannesburg; Cairo; Cape Town; Addis Ababa; Casablanca; Algiers; Nairobi; Lagos; Tunis and Durban

- Ethiopia’s travel and tourism market grew by 48.6 percent in 2018, the largest increase of any country in the world that year (World Travel and Tourism Council, 2019)

- Ethiopia recently became the biggest transfer hub for long-haul travel to Africa, overtaking Dubai

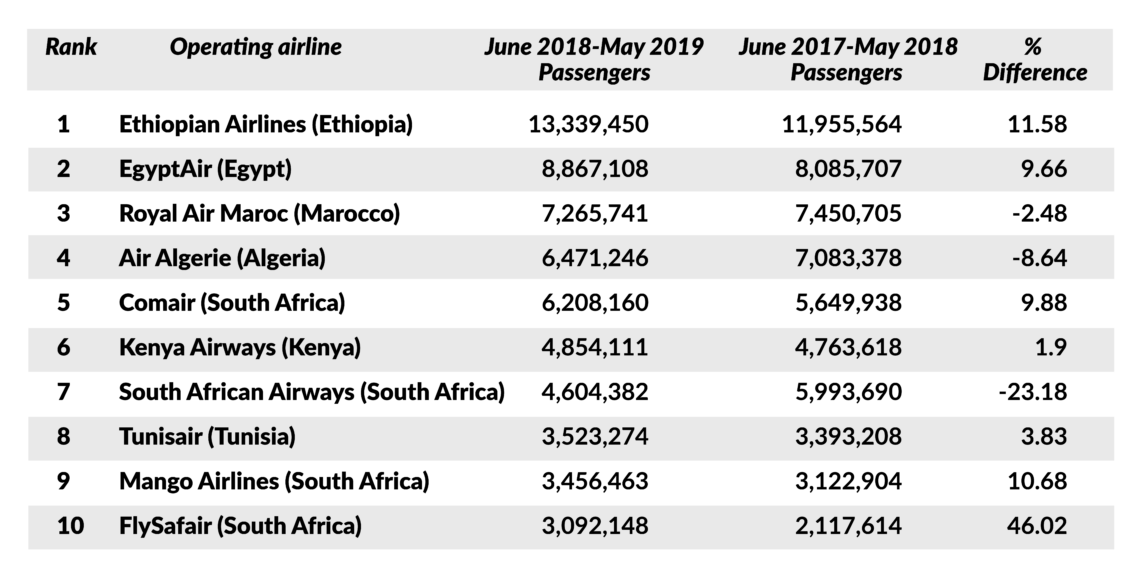

- Ethiopian Airlines flies to 58 destinations in Africa

- By 2035, the new Bugesera International Airport in Rwanda is expected to serve more than 14 million passengers annually

- Benin, Burkina Faso, Cape Verde, Ghana, Mozambique, Niger, the Republic of Congo, Rwanda, Gambia and Togo have already implemented the SAATM’s eight concrete measures

Headwinds

However, the prospect for open skies and a thriving aviation industry remains both distant and fragile. Many African countries’ aviation sectors are characterized by protectionist policies, infrastructural gaps, financing constraints and regulatory restrictions. Several governments consider the protection of national airlines a political priority, while other states see aviation more as a source tax revenue than an engine of economic growth. Moreover, African companies face specific competitive disadvantages that prevent them from expanding their market access, including safety bans imposed by external regulators, inadequate infrastructure and high operating costs. Furthermore, African countries are particularly vulnerable to the potential effects of unexpected economic or political shocks.

According to the African Development Bank’s figures from 2019, fuel (which accounts for 20 to 40 percent of airlines’ operating costs) and airport fees in Africa are 20 percent more expensive than in Europe, while maintenance and commercial costs are twice as high on average. Indirect operating costs such as leasing charges are often higher too, reflecting perceived security risks.

Facts & figures

Despite the sector’s potential, there is significant uncertainty surrounding the demand for air travel in Africa, which may scare off potential investors. According to data from the International Air Transport Association (IATA), African airlines have an average load factor (percentage of seats filled) of 71 percent, well below the global figure of 81.2 percent. For most Africans, flying remains too expensive, while many countries have high risk profiles due to the potential for security shocks and political instability.

Providing lift

With the exception of Ethiopian Airlines, African national flag carriers are not profitable. South African Airways (SAA) has not generated a profit since 2011 and is set to receive a $1 billion bailout. In 2019, Kenya Airways registered net losses estimated at more than $75 million and is undergoing a painful restructuring process. However, several countries – including Uganda, Tanzania, Zambia, Senegal and Ivory Coast – are reviving or expanding their national flag carriers.

The rising star of African aviation is the state-owned Ethiopian Airlines. The company has made an extraordinary comeback, becoming the continent’s largest carrier by passengers, fleet and revenue. This growth was spurred by Ethiopia’s Vision 2025 plan, which included huge investments, several bilateral deals with other carriers, visa relaxation policies and the expansion of the Bole International Airport.

Large global players may determine the future of the African aviation market.

Considering the challenges and investments required, Ethiopian Airlines and large global players – especially the three Gulf carriers and Turkish Airlines – may determine the future of the African aviation market, either by action or inaction.

Ethiopian Airlines expanded its footprint across Africa through strategic partnerships, partial acquisitions and opening hubs throughout the continent. The company has stakes in several smaller African carriers, including Malawi Airlines, Zambia Airways and ASKY Airlines (a West African carrier with headquarters in Lome, Togo).

Turkish Airlines, which benefits from its home country’s geography and diplomatic relations, has also established a significant network on the continent. It flies to more than 56 destinations in Africa and is the only non-African airline that flies to Somalia. The Gulf carriers (Emirates, Qatar Airlines and Etihad Airways) have all expanded their presence in Africa in recent years through more flights and new routes.

Facts & figures

Emirates, for example, generates the most revenue of any company in Africa’s airspace, operating four of the 10 most profitable routes to and from the continent. In 2019, Emirates established an agreement with Ghana-based Africa World Airlines (AWA) to increase connectivity in West Africa. Qatar Airways, which flies to 21 destinations in Africa, is also expanding its footprint on the continent, albeit more cautiously. The company will not venture into start-ups and has declared that it will only invest in stable countries and in markets that guarantee a return on investment. It recently signed a deal with the Rwandan government to acquire a 60 percent stake in the under-construction Bugesera International Airport south of Kigali and is in talks to buy a 49-percent stake in RwandAir.

Scenarios

In the coming years, governments will further liberalize Africa’s aviation sector, leading to increased capacity, new routes and novel partnerships. The process will generate winners and losers, but – as happened in Asia and Latin America – it will benefit Africans and the African economy.

The continent has 16 landlocked countries, the lowest levels of road and rail connectivity in the world, a series of emerging markets and strong ambitions for regional economic integration. Estimates that air traffic in Africa will increase by 4.8 percent a year through 2038 (Airbus, 2019) may be too optimistic, but in the long term the sector will likely expand quickly on the back of economic growth, tourism, trade and the slow but steady rise of the middle class. This growth trajectory, however, will be compromised by overall low resilience to external shocks. Even under a best-case scenario, the coronavirus is expected to negatively affect the sector in the short to medium term, as Chinese routes – vital for key companies operating in Africa – are suspended and tourist flows are expected to decline.

Open skies and win-win synergies

Under this less likely scenario, liberalization would take place through a smooth and effective transition, leading to a mixed picture where gains would clearly outweigh losses. The successful implementation of AfCFTA, increasing integration of regional markets and rising demand for air connectivity would all contribute to this scenario.

Though some companies would not survive, some national carriers would enter into strategic partnerships with global players following the Rwanda-Qatar model. Others would establish or expand codeshare agreements or forge regional alliances to improve efficiency. In several countries, increased competitiveness would result in significant efficiency gains and higher penetration of low-cost carriers. These developments would generate positive outcomes in the form of lower tariffs, increased connectivity, job creation, expansion of aviation support services and investment in infrastructure.

Turbulence, winners and losers

Under this more likely scenario, the liberalization of the aviation sector would be a long, messy process, leading to large gains and heavy losses. Some African governments will refuse to give up control over the sector, keeping protectionist regulations and heavy taxes in place. Others will struggle to find investment.

Two regions would stand out. In West Africa, due to its growth potential and widespread compliance with the SAATM implementation measures, there would be fierce competition for market position. Due to geography, African carriers in this region may have an advantage over the Gulf carriers and other global companies. In East Africa, and despite Ethiopian Airlines’ strong position, Rwanda would emerge as a regional hub and RwandAir’s gains would be the losses of national flag carriers in Kenya, Uganda and Tanzania.

In the medium to long term, this scenario of big winners and big losers could be reinforced by a difficult market worldwide. Slowing economies, weakening global trade, tougher restrictions on travel (dictated by environmental and health concerns) and higher fuel prices would all have a significant impact on the sector.