The ‘Big Rethink’ in macroeconomics

The 2008 financial crisis threw the discipline of macroeconomics into turmoil. Since then, some of the world’s most respected economists have advocated a ‘big rethink’. Yet a troubling trend is growing stronger: basing macroeconomics on ideological, not scientific, grounds.

In a nutshell

- The Great Recession upended much of economic theory

- New ideas are mostly Keynesian with a modern twist

- Many economists want to focus on eliminating inequality

One of the many frustrating lessons the global financial crisis taught anyone who studied macroeconomics before 2008 is: “Forget everything you have learned.” Not only had the discipline failed to predict such a huge debacle, but its overly abstract models appeared to have ignored the complex and potentially destabilizing role of the financial system.

A decade later, it is worth asking if macroeconomics has managed to reinvent itself and if it is better equipped now to address such severe economic shocks.

Moments of rupture

Twelve years ago, policymakers and academic researchers alike were suddenly propelled into a new, radically uncertain, world. Overtaken by dramatic turns of events, the former had to react quickly and pragmatically, often forced to take error-prone leaps in the dark. The latter were urged to rework their basic theories, to provide more useful guidance for policymakers on how to manage the effects of crises on a global and national level.

Many began to posit that what might be needed after the Great Recession of the 2010s is a complete overthrow of prevailing macroeconomic thinking. It should be a paradigm shift of the same caliber as the Keynesian Revolution of the 1930s or the monetarist alternative of the 1970s. The first was a response to the Great Depression which held that only the firm hand of government can secure stability, full employment and economic prosperity.

The Great Inflation of the 1970s and the ensuing stagflation revealed the failure of Keynesian interventionism.

The second emerged some 40 years later when the Great Inflation and the ensuing stagflation revealed the failure of Keynesian interventionism, especially its inflationary prescriptions for unemployment. The monetarist approach focused on predictable monetary policy rules (instead of discretionary action) to combat the tenacious inflationary pressures and market volatility that had undermined the global economy in the 1970s and 1980s.

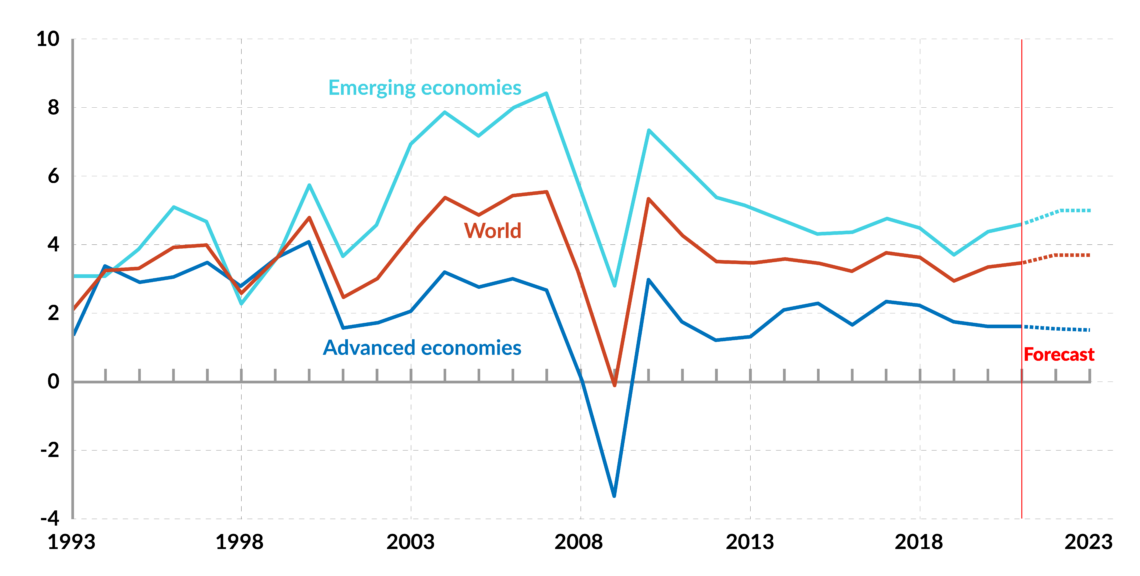

The new generation of macroeconomists ushered in a 30-year era of Great Moderation, in which central bank action was largely freed from fiscal pressures. The assumption underlying the new theoretical stance was that market economies, naturally prone to fluctuations, are largely capable of self-stabilizing, provided the institutional framework allows them to do so effectively. The 2008 crisis called this view into question.

Facts & figures

Fog of war

In the aftermath of the crash, a group of elite economists took on the challenge of sketching the contours of a new macroeconomic paradigm that would draw the right lessons from the crisis. They are mostly professors at prestigious American universities, many of them going back and forth between academic and policy circles. They include Olivier Blanchard, Ben Bernanke, Gregory Mankiw, Kenneth Rogoff, Joseph Stiglitz, Lawrence Summers and Paul Volcker, to name just a few.

The experts gathered for the first time in 2010 for a conference entitled “Rethinking Macroeconomic Policy,” hosted by the International Monetary Fund (IMF), under the leadership of Olivier Blanchard, the institution’s chief economist between 2008 and 2015.

At the time, the financial crisis was at its peak in Europe, where the resulting recession and sovereign debt crisis raised major concerns for the safety of the eurozone’s common currency. The broad consensus on which the economic science community had agreed over the previous decades – about what macroeconomics can understand and what normative recommendations it should make – had been shattered. Much of the profession was bewildered and divided.

The goal of the IMF’s new discussion was to identify where economic theory had gone wrong and what parts of the precrisis framework remained valid. However, no consensus emerged from the first round of talks. Later, Mr. Blanchard would say that the consultations had taken place in “the fog of war.”

In the trenches

Four more conferences followed, two under the auspices of the IMF (held in 2013 and 2015) and two (in 2017 and 2019) under those of the Washington-based Peterson Institute for International Economics (PIIE), which Mr. Blanchard had joined after leaving the IMF. A book was published after each of these events.

In the 2013 edition, a change in the direction of macroeconomic policy was clearly in the air, but without anybody really knowing what the destination was, then-IMF Managing Director Christine Lagarde recalled. Governments were experimenting with a myriad of new policy responses at the time. Some proved successful, others were huge failures with far-reaching consequences.

The 2015 meeting (which Mr. Blanchard was tempted to subtitle “in the trenches”) came up with more questions than answers. Is monetary policy’s current objective (guaranteeing medium-term price stability) too narrowly defined, or should central banks’ mandates be extended to include financial stability? What additional tools and regulations are needed to mitigate system-wide risks? Should there be more control over international capital flows? How could the explosive public debt ratios in many countries be stabilized? Is fiscal austerity the right answer? If not, what would be the alternative?

There were fragmented and sometimes paradoxical insights gained from the relatively recent cascade of crises, and there was more doubt than ever on how to incorporate them into macroeconomic theory. Many experts doggedly stuck to their positions. It seemed that reaching an agreement over the issues would be nearly impossible.

Grasping the nettle

Fundamental questions, especially regarding the respective roles of monetary policy and fiscal policy, still had to be addressed when Mr. Blanchard opened the fourth “Rethinking” seminar in October 2017. This time, the economists at the event were determined to face up to the problem. They started by bringing in a set of presumptions that can be summarized as follows.

First, economies are not “linear” or “self-stabilizing” systems. They may well “implode,” as the 2008 crisis had shown. Hoping for markets’ alleged self-regulatory capacities to overcome deep downturns is vain and perilous.

Second, market participants’ expectations are not as “rational” as standard macroeconomic models assume. Professor Blanchard, for his part, is interested in the role so-called “extrapolative” expectations may have played in the 2008 global panic. The “irrational” part in investor decision-making is key to understanding what had happened, many of these economists argued. In the blink of an eye, investors can go from being overly optimistic to overly pessimistic about the safety of an asset.

In the blink of an eye, investors can go from being overly optimistic to overly pessimistic about the safety of an asset.

Third, crises do not appear out of the blue. Like heart attacks, they build up long before the shock hits. The strong growth rates observable in the late 1990s and early 2000s had been propelled by euphoric stock markets that, in retrospect, were speculative bubbles. Prior to the crisis, a long-term financial expansion (in this case the dot-com bubble), had lifted the global economy, but much of it was hot air. As Lawrence Summers remarked, it has been a long time since our economies have grown in a “healthy” way, with “sustainable financial conditions.”

Fourth, the effects of crises may last much longer than is usually predicted. Economists use the term “hysteresis” to describe events in the economy whose effects will persist into the future, even after the factors that had led to them have been removed. For instance, high unemployment rates may persist for a long time after growth and investment have recovered.

The 2008 crash is a textbook case. For the foreseeable future, we will operate in an environment that is very different than the one that prevailed before the crisis – this is one of the main lessons the experts at PIIE drew from the global recession. For them, it is a mistake to think we can ever go back to precrisis ways.

Secular stagnation

These experts caution us that we have entered a “new normal” of deflationary pressures, persistently low interest rates and sluggish growth. Globally, real (inflation-adjusted) interest rates can be expected to stay at record lows (under 1 percent) over the next 30 years, they argue. Average growth rates will probably remain low as well – though slightly higher than interest rates, according to Mr. Blanchard. If these economists are right, it is possible that economies could get locked into what Ms. Lagarde once called the “new mediocre.”

However, according to Professors Blanchard and Summers, our current low-growth, low-rate environment is not a direct legacy of the 2008 crisis, as is frequently claimed. The Great Recession only precipitated our descent into what Mr. Summers calls “secular stagnation,” but did not cause it.

In fact, the problems of our industrial world run much deeper than just dysfunctional financial markets, Mr. Summers insists. The decline of real safe rates started in the 1980s, due to a progressive deceleration of total-factor productivity growth, among other things. This phenomenon can be explained by a persistently weak demand for capital, a lack of public investment, insufficient technological innovation and, most importantly, aging populations.

The biggest danger for economies, in this view, is people’s rising propensity to save, exacerbated by their increasing preference for safe assets in times of uncertainty. This might mean that many countries could be stuck in what Maynard Keynes called a “liquidity trap” for a long time to come.

Back to the future

“Insufficient demand” has led to a “chronic excess of saving over investment,” Mr. Summers asserted. This “global savings glut,” in his view, is the real culprit of the low-for-long situation.

This interpretation could explain why today, monetary policy appears to be at the end of its rope, including in advanced economies such as the eurozone. Since 2015, the European Central Bank (ECB) has pushed its use of conventional and unconventional policy tools to the breaking point, without ever hitting its inflation target: below but close to 2 percent. Policy rates have long remained at the “zero-lower-bound” (in September 2019, they fell to -0.50 percent in the euro area), considerably reducing monetary policy’s margin of maneuver.

At the end of his mandate as ECB president, Mario Draghi said that he regretted that the burden of macroeconomic adjustment had fallen disproportionately on monetary policy. To bring investment and growth back on track, he urged governments to offer strong fiscal support: more public spending and redistribution, more public debt and deficits and, ultimately, greater penalization of savers.

There are circumstances in which central banks should not mind working with governments, Former Fed Chair Ben Bernanke, also a “Rethinking” conference attendee, conceded. He argues that monetary and fiscal policy should go hand in hand in the future, even if this means surrendering some of the sacrosanct central bank independence.

“Rethinking macro stabilization: Back to the future” – the title alone of the presentation given by Mr. Blanchard and Mr. Summers in 2017 reflects the new macroeconomic paradigm. Essentially, it means reenacting, in modern terms, the old Keynesian revolution.

Ideological takeover

The fifth and most recent edition of the “Rethinking” cycle, held at PIIE in October 2019, included a distinctly 21st century-Marxist tone. The title of the conference was: “Combating Inequality: Rethinking Policies to Reduce Inequality in Advanced Economies.”

At this stage, rethinking macroeconomics appears to amount to a debate on moral, rather than scientific grounds.

The speakers who were invited also made the new approach clear. Among them were Emmanuel Saez and Gabriel Zucman, prominent French professors at the University of California, Berkeley. Both are disciples of Thomas Piketty and are convinced that we should “tax our way back to justice.”

At this stage, rethinking macroeconomics appears to amount to a debate on moral, rather than scientific grounds. The questions include, for instance, whether a wealth tax would help reduce inequality, considered by many as one of the most harmful economic maladies of our time. That issue, again, deeply divides the profession. What seems to be at stake is the future of macroeconomics against a reappropriation of the discipline to ideological ends.

Unthinking macroeconomic policy

Before a sixth edition of the “Rethinking” cycle was even being planned, a new global crisis took us by surprise in early 2020, putting macroeconomics to a new, difficult test.

Within a few weeks, the COVID-19 pandemic led to a lockdown of entire countries, paralyzing economic activity and squeezing both supply and demand worldwide. Experts agree that the impacts of this health emergency will be profound and long-lasting. Some already predict that the economic threat of this unusual and unexpected situation, which many have compared to a “war,” could be significantly bigger than the 2008 financial crisis.

Rather than sparking yet another dramatic change in the way macroeconomists think about their field, this new crisis rapidly rallied policymakers and their economic advisors around the justification of coordinated fiscal stimulus, massive state intervention, and control over populations and national economies.

Mssrs. Saez and Zucman were among the first to call for a socialization of the direct output losses induced by the pandemic. Governments should act as “payers of last resort,” so that hibernating businesses can keep paying their workers and bills, they insist. Following this line of argument, most advanced countries have already announced multibillion-dollar bailout plans.

We might have to deal with the defects of increasingly intrusive governments that try to reinvent central planning.

Also, the ECB promised to make available up to 3 trillion euros in liquidity through its refinancing operations, at the lowest interest rates ever offered, -0.75 percent. Ms. Lagarde, the bank’s new chief, declared that her institution is “fully prepared” to increase the size of its asset purchase programs and adjust their composition “as much and for as long as necessary.”

In March, two generous spending programs, mobilized under the ECB’s newly created Temporary Pandemic Emergency Purchase Program, were announced in one week. The first of these was worth 120 billion euros and the second, 750 billion euros. Together, they amount to some 7.3 percent of the eurozone’s gross domestic product. The European Commission, for its part, suspended the Stability and Growth Pact.

The “intravenous cash flow,” financed mostly via public debt, might, as Mssrs. Zucman and Saez hope, alleviate economic hardship in the short run, eventually preventing our economies and public health systems from collapsing.

The long-term consequences, though, are being ignored by many in the heat of the moment. Above all, we might have to deal with the defects of all-encompassing, technology-empowered and increasingly intrusive governments that try to reinvent central planning, forgetful of fundamental historical debates on the matter in early 20th century macroeconomics.

At the heart of that old debate is the insight that big government comes at a cost: ineffective bureaucracies, a misallocation of resources, social conflict and last but not least, the confiscation of individual liberties.