The future of cryptocurrencies

With the most popular cryptocurrency Bitcoin losing value, its advocates are disheartened. But crypto is here to stay while regulation and taxation are likely coming.

In a nutshell

- Cryptocurrency is perceived as a speculative investment and a store of wealth

- It is not gaining popularity as a means of payment for ordinary transactions

- Ignore, ban or regulate? Governments will likely choose the third option

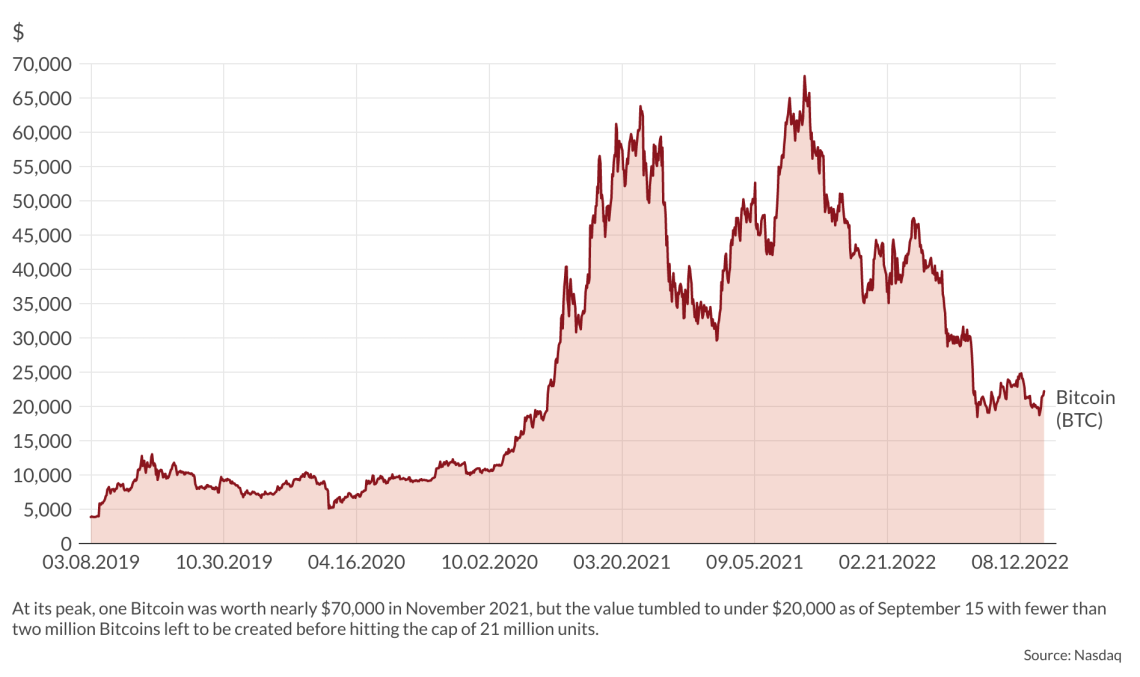

Cryptocurrencies have suffered a hard beating over recent months. For example, the U.S. dollar/Bitcoin exchange rate fell from almost $70,000 in early November 2021 to below $20,000 in late June and, despite ups and downs, dipped to $19,733 on September 15.

Historically, Bitcoin – by far the most popular form of cryptocurrency – has been a success story for those who bought it: the exchange rate versus the dollar was below $3,000 five years ago. Yet, many bitcoin advocates have been disappointed in two respects. This cryptocurrency has failed to become a widespread means of payment and has turned out to be a poor defense of purchasing power in periods of uncertainty and inflation. This is surprising. Bitcoin’s supply is limited to 21 million units. Since more than 19 million units, or 90 percent, have already been issued (“mined”), most people expected that the cap would have caused a constant rise in its dollar-denominated price.

What is the future?

To predict future scenarios for cryptocurrencies, it may be useful to consider what happened in the past and clarify a few key points. First, the world of blockchain consists of cryptocurrencies and crypto derivatives. For example, Bitcoin is a cryptocurrency while stablecoins Tether and TerraUSD are crypto derivatives. These are “derived” from cryptocurrencies and/or pegged to a widely recognized and centralized currency, like the dollar. Put simply, a financial investor hands out dollars to a company and receives a derivative in return. The company converts the dollars into cryptocurrencies and lends them to global borrowers. At the same time, the company promises the financial investor to exchange the derivatives on demand for a fixed amount of a given cryptocurrency, possibly pegged to the dollar, or backed by dollars.

The upshot is that if you have bought Bitcoins or other cryptocurrencies, you win/lose following the exchange rate of the cryptocurrency in your portfolio. If you have bought a derivative, however, you may find out that it is not really backed by an adequate quantity of cryptocurrencies or that the dollar-convertibility guarantee is porous, to say the least. If so, the derivative turns out to be all but worthless. This is what happened during the past few months with several crypto derivatives. Companies issuing such products are very active on the market and contribute to making the underlying assets volatile, especially if they promise stellar returns, which boost the demand for cryptocurrencies and crypto derivatives. If the derivatives products are poorly collateralized, investors are scared away in bad times.

The 2022 crash in the crypto market has hit the world of derivatives, possibly eliminating a major source of volatility.

A second key point is that cryptocurrencies are currently considered both a speculative instrument and a store of wealth, rather than a means of payment for ordinary transactions. For example, more than 60 percent of the total bitcoins in circulation are held in accounts (“wallets”) with more than 100 Bitcoins each, and are rarely traded on the market, other than to adjust portfolios: in late July 2022, only about 250,000 Bitcoins were traded daily and it is likely that just a small portion related to commercial transactions. Moreover, cryptocurrency holders seem to have a long-term view. For example, both “shrimps” and “whales” (accounts with less than 1 and over 1,000 Bitcoins each, respectively) have taken advantage of the recent sell-off to buy the dip in large amounts.

Three preliminary conclusions follow: (1) the long-run approach of the typical cryptocurrency holder suggests that the cryptocurrency project is not an easy kill, and survives dramatic volatility; (2) volatility has been driven by crypto derivatives, the activity of which has been magnified by the relatively small amount of cryptocurrencies traded on the market; (3) the 2022 crash in the crypto market has hit the world of derivatives, possibly eliminating a major source of volatility by killing some market movers, hitting short-run speculators and offering opportunities to long-run crypto investors.

Facts & figures

Bitcoin value tumbles

Based on ‘nothing’ but worth something

Of course, cryptocurrencies are not like stocks and bonds, which are backed by promises of future income streams, sometimes generated by a company’s successful market performance and sometimes by a governmental commitment to squeeze taxpayers. Instead, cryptocurrencies are monetary units backed by nothing and their value depends on their credibility as a future means of payment to buy goods, services and other means of payment.

In the end, regulation seems to be the safest strategy.

Central bankers and policymakers in general do not miss a chance to warn the public that cryptocurrencies are a scam. European Central Bank President Christine Lagarde recently declared that cryptocurrencies are “based on nothing” (correct) are “worth nothing” (incorrect) and that regulation is required to prevent inexperienced investors from losing all the money they put into cryptos (incorrect).

Ironically, central bankers offer digital currencies, which in President Lagarde’s view are “vastly different” from cryptocurrencies. Central bankers’ digital currencies are certainly different from blockchain-based cryptocurrencies, but not for the reason Ms. Lagarde probably has in mind. The key issue is that decentralized currencies with a supply cap would eliminate the very notion of monetary policy and transform central bankers into an agency regulating commercial banking and producing statistics. Understandably, the world of central banking is not pleased with the prospect.

In other words, central bankers are not hostile to cryptocurrencies because they are allegedly fraudulent. If fraud means “based on nothing,” then all central bankers should be taken to court. Rather, their hostility comes from the fact that widespread acceptance of cryptocurrencies will eventually undermine the privileges of central banking, with repercussions, say, on the financing of public indebtedness.

Scenarios

Policymakers and central bankers have three possibilities.

Ignore

They can ignore, outlaw or regulate cryptocurrencies. The first course of action is the easiest. Why should central bankers bother? After all, the world of cryptos is highly competitive and some currencies will disappear. Moreover, today they are not a real threat to money. Moving from dollars or euros to one or more cryptocurrencies is not easy: the cost of each transaction is still relatively high. As long as governments accept centralized currencies like dollars and euros as the only means of payment, a move to cryptos would actually be equivalent to switching to a cumbersome double-currency regime that many people would dislike. These regimes existed in the past, but for short periods of time.

Outlaw

Outlawing cryptocurrencies would make little sense unless the authorities feared that large transactions involving cryptos could destabilize the fiat-currency exchange rates. Besides, outlawing cryptocurrency must necessarily be a global move. It would lose credibility if some countries refused to comply. The fundamental problem with this approach is that the existence of cryptocurrencies and crypto derivatives is not a crime, and it is far from evident that those who buy them are acting against the public interest.

Regulate

In the end, regulation seems to be the safest strategy. Without any realistic short-term threat to fiat money as a means of payment or evidence of their use in money laundering, the only true concern of the authorities is taxation. This is the single item on which the regulator is likely to focus. It has little to do with the decentralized feature of cryptos, but rather the tax collector has no way to find out how much wealth the taxpayer has stored away, and it would be very hard even to know whether an individual has an account. Future regulatory efforts will go in the direction of forcing greater transparency with the aim of tracking and taxing this form of wealth.

In early July, the European Parliament approved the Market-in-Crypto-Assets proposal. If implemented on a global scale, crypto-asset providers will not be allowed to operate without authorization. This authorization will undoubtedly come with strings attached – in theory, to protect investors from fraud, in practice, to force them to make their accounts visible. This is only the beginning unless technology makes authorized dealers redundant.