ASEAN’s energy transition: Risks and opportunities

While energy developments in Southeast Asia are often overlooked for other global trends, the region’s continued industrialization will increasingly drive worldwide economic growth and energy demand. The region is set to become a net importer of fossil fuels.

In a nutshell

- Southeast Asia’s energy mix is based mainly on fossil fuels

- Industrialization will put ASEAN center stage on climate policy

- A faster green transition is needed to meet goals

Given global energy trends and climate policies, energy developments in the Association of Southeast Asian Nations (ASEAN) are too often overlooked. The regional shift from agriculture to industrialization is expected to become one of the drivers for worldwide economic growth and energy demand.

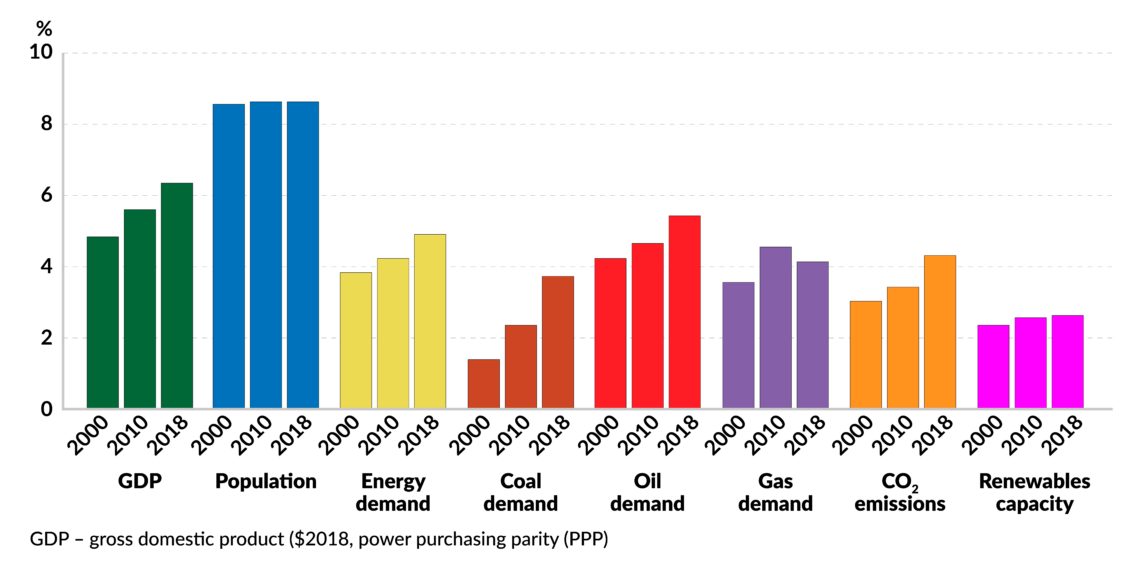

ASEAN’s rapid economic growth is based on a population increase of almost 120 million, up to 770 million – with a regional GDP reaching $20 trillion by 2040, rising living standards, and an annual average GDP growth of 5 percent. The resulting rapid growth of total primary energy supply by as much as 80 to 250 percent, and 10 to 100 percent more emissions by 2040, will transform ASEAN into a net importer of fossil fuels with higher energy security risks, increased energy (import) costs and accelerated climate changes.

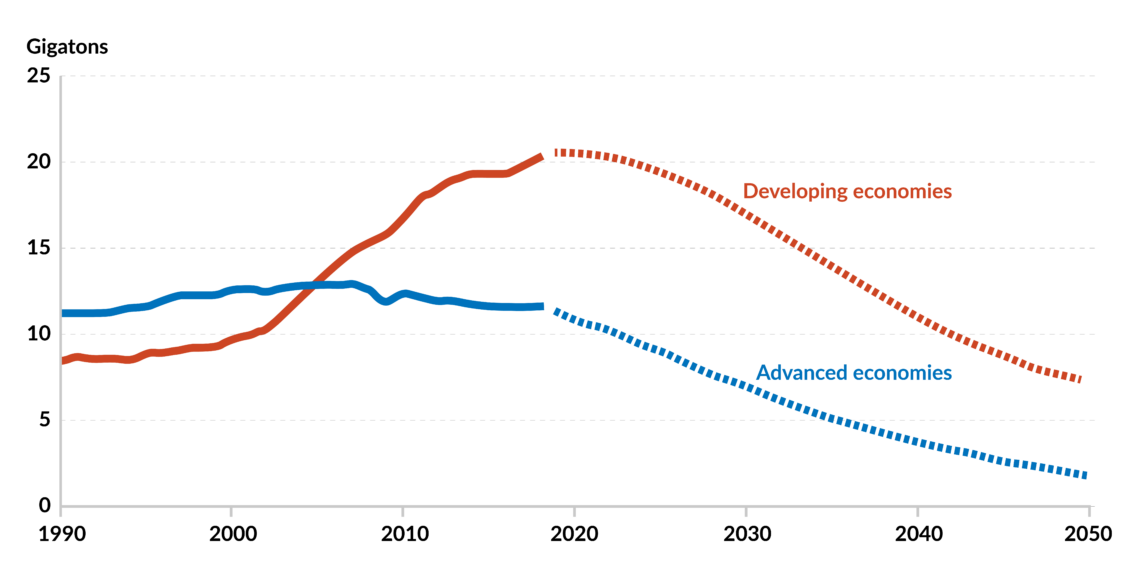

While advanced economies have to move ahead with a faster decarbonization and energy transition, the emission reduction target of 1.5 to 2 degrees Celsius cannot be realistically achieved without a more rapid change by emerging economies and developing countries. The broader Asia region accounts for some 60 percent of the global total CO2 emissions; almost two-thirds of those emissions are from the energy sector, heavily reliant on fossil fuel consumption. The region was responsible for 80 percent of the world’s total coal consumption in 2018.

The ASEAN primary energy mix is still based on fossil fuels, with a regional electricity demand of 6 percent annually – one of the highest in the world. The ASEAN Plan of Action for Energy Cooperation (APAEC) 2010-2025 includes short-term targets with a 23 percent share of renewable energy in the total primary energy supply. By 2025, it will also increase its share in power capacity to 35 percent and reduce energy intensity by 32 percent from 2005 levels. Solar photovoltaic capacity needs to increase from 32 gigawatts (GW) to 83 GW, and hydropower capacity from 59 GW in 2020 to 77 GW by 2025. As ASEAN becomes a net importer of fossil fuels in the next decade, its net energy trade deficit could run to more than $300 billion a year.

Facts & figures

Association of Southeast Asian Nations (ASEAN)

- Founded on August 8, 1967 with five members: Indonesia, Malaysia, the Philippines, Singapore and Thailand

- Now comprising 10 member countries, including Brunei, Cambodia, Laos, Myanmar, and Vietnam

- Headquartered in Jakarta

- Total population in 2019 of 650 million, with a combined GDP of $9.34 trillion

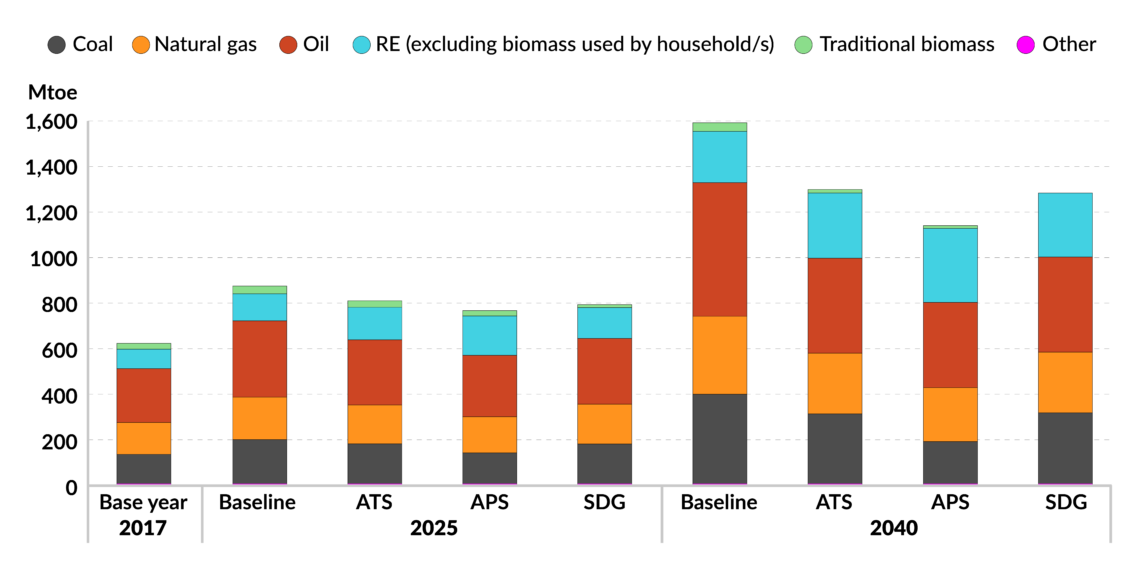

Although ASEAN presently accounts for around 6 percent of global energy demand, its energy consumption is projected to increase by as much as 60 to 146 percent (depending on scenarios), while its electricity consumption will at least double by 2040, compared to 2017. The per-capita energy demand in the poorer ASEAN member states is still relatively low internationally.

The region’s rising demand is also propelled by rapid urbanization. Less than 50 percent of the population living in the cities today will climb up to more than 60 percent in 2040, bringing a tremendous increase in air conditioning. Today only 15 percent of the regional households have air conditioning, compared with 80 percent in advanced economies such as Singapore and Malaysia. The overall number of air conditioning units has been forecasted to skyrocket from 40 million today up to 350 million (60 percent of households) in 2040.

Hydropower is still the most important renewable energy source, and its capacities have quadrupled since 2000. But even with hydropower, renewables presently meet only 15 percent of the regional energy demand. Globally, renewables may overtake coal to become the largest source of electricity generation in 2025, supplying one-third of the worldwide total. Developing countries in Asia accounted already for over half of the global growth in electricity generation from renewables during recent years.

The Covid-19 impact on ASEAN

Asia represented three-quarters of the 570 million people worldwide that had electricity access between 2011 and 2017. But half of the population in the Asia-Pacific region – almost 2 billion people – still rely on traditional biomass, coal and kerosene for cooking and heating.

The Covid-19 pandemic has caused a global, multifaceted crisis (a so-called “polypandemic”) and undermined development progress, exacerbating state fragility and eroding existing international cooperation. The pandemic has also threatened the progress that the developing countries of ASEAN and other regions in Asia and Africa have made during the last decade in improving access to electricity and modern energy sources, and the Sustainable Development Goals (SDGs), agreed by member countries of the United Nations. These include energy-related goals: achieving universal energy access (SDG 7), reducing the impacts of air pollution (SDG 3.9) and tackling climate change (SDG 13).

The emerging and developing countries in Asia are responsible for about 30 percent of worldwide CO2 emissions. In Indonesia, the destruction of carbon sinks in forests and carbon-rich peatlands are the biggest CO2 emitters.

Facts & figures

ASEAN’s energy transition is also complicated by the uncertainty of how long the worldwide pandemic (with its new variants) will last and when a full economic recovery will occur. Last spring, a group of developed countries accounting for just 16 percent of the world’s population secured 60 percent of the global vaccine supplies for themselves. Only a fifth of the targeted population will receive a vaccine this year, while the bulk of the needed vaccinations will take place only in 2022 and 2023. In the meantime, the risks of much more mutations of Covid-19 could increase, resulting in even more dangerous pandemic dynamics, as highlighted by the Delta variant.

Financial fragility has increased in already highly indebted sectors, especially in emerging and developing countries, complicating any faster green energy transition. Two mutually reinforcing risks present since 2020 could further increase energy inequality. One risk is that the economic slowdown will increase poverty by making energy less affordable for already struggling populations or even cause reversals in recent progress on energy access. The second is that countries with the greatest need to improve access to energy and clean cooking will face even more problems with financing any new energy access projects, hampering their ability to improve their short-term situations. Many other vulnerable households that currently have access to electricity have been increasingly unable to pay their bills since 2020.

A failing coal-to-gas shift?

Over the past 20 years, Asia accounted for 90 percent of all coal-fired electricity generation capacity built worldwide – led by China (880 GW) and followed by India (173 GW) and Southeast Asia (63 GW). Coal-fired power plants have operational lifetimes of 30 to 40 years. In Asia’s developing economies, existing coal plants were an average age of only 12 years in 2019 and are likely to operate for three to four decades to come.

The three-way race among coal, natural gas, and renewables to provide power and heat has intensified in Asia’s fast-growing economies. In most developing Asian countries, “king coal” has remained the incumbent energy source. It has been affordable with high price stability and is abundant in many member states (with about 12-14 billion tons of reserves in 2035) for sustaining regional economic growth. But even in Asia, new investments in coal-using infrastructure have slowed since 2016. The CO2 emissions of the large set of global coal-fired power plants can be more than halved by 2030 by retrofitting, repurposing, or cost-effectively retiring them.

Developing Asian economies will drive half of the global growth in natural gas demand.

In 2019, ASEAN coal accounted for some 89 GW of installed power capacity, projected to almost double up to 163 GW by 2040. The share of coal could further climb from 33 percent in 2015 to 53 percent by 2040 to meet the region’s growing electricity demand – rising up to 2,000 terawatt-hours (TWh) over the next 20 years. Eighty percent of the existing power plants are still using subcritical technology. Shifting and retrofitting ASEAN’s projected coal capacity in 2035 to 100 percent ultra-supercritical coal-power plants could reduce emissions by 1.3 billion tons – equivalent to 25,000 installed wind turbines or removing 157 million cars from the road.

However, several ASEAN countries have maximized their coal production amid the pandemic to ensure national energy resilience and guarantee baseload electricity supply. ASEAN still favors new emission standards and improving the efficiency of coal-fired plants by moving from subcritical to supercritical and ultra-supercritical technologies rather than considering a long-term coal phaseout.

Facts & figures

Rising concerns around energy supply security also hamper a faster coal-to-gas shift in ASEAN member states. Developing Asian economies will account for half of the global growth in natural gas demand and almost all increases in traded volumes. By 2040, they will consume some 25 percent of the world’s gas production – much of it sourced from other regions. LNG has been expected to overtake pipeline gas supplies in the global gas trade by the late 2020s, growing from 39 percent in 2016 to around 60 percent by 2040. Rising LNG supplies and trading opportunities will transform ASEAN into a net importer of LNG, with a need to diversify its gas imports. The regional gas demand growth will outpace the production increase from 201 billion cubic meters (bcm) in 2019 up to 250 bcm by 2040.

A faster green transition

Despite the region’s coal addiction, the region’s states have started paying more attention to expanding renewables, electromobility and a green energy transition. Indonesia is considering adopting a net-zero emissions target for 2070. Its biggest utility company, Perusahaan Listrik Negara (PLN), aims to phase out fossil fuels by 2060 to achieve carbon neutrality.

Singapore unveiled a “Green Plan 2030,” outlining green targets for 2030 and introducing a circular economy focused on reducing, reusing, and recycling. It also seeks to halve its peak emissions by 2050 to achieve zero emissions “as soon as viable” in the second half of the century. Vietnam is considering halving its planned coal power plants in favor of gas, wind and solar, as new investments in coal-fired plants have become a riskier choice (though its share for power supply will remain at 31 percent of its energy mix by 2045).

The region has paid more attention to expanding renewables, electromobility and a green energy transition.

The Philippines, Vietnam, Indonesia and Bangladesh plan to decrease up to 62 GW of planned coal power in 2020 – an 80 percent reduction from the 125 GW planned five years ago. According to industry forecasts, building new solar and onshore wind to develop power will become cheaper (even factoring in battery backup storage) than operating coal plants in the region between 2027 and 2029. Since 2019, Vietnam and other ASEAN countries have already spurred the development of solar capacity in particular.

The regional progress can also be seen in the fact that several ASEAN countries have achieved 100 percent electrification. Energy efficiency is being enhanced in the industrial, construction and transports sectors. The regional energy intensity remains one of the lowest worldwide. Several countries have realized the failures of inadequate regulatory frameworks, unattractive price schemes and multiple failed policies and instruments. At present, international pressure to reduce coal consumption and prevent investments in new coal power plants –together with high and volatile gas and LNG prices – will also boost the further expansion of renewables in the forthcoming years.

Strategic perspectives

For achieving regional energy security and sustainability over the coming decades, the big question for the region is how climate change will determine governments’ and industries’ policies, as ASEAN stands at the front line of climate change. It will force the area to adopt costly mitigation measures for enhancing resilience across all economic and energy sectors.

Despite ASEAN’s progress in investing in clean energy, it will still not do enough to even achieve even the SDG 7 target. For faster decarbonization of ASEAN’s energy mix, a long-term coal phaseout, developing more market mechanisms (such as electricity trading among the states in ASEAN’s Power Grid), and more comprehensive planning with robust policy and regulatory frameworks need to be introduced. Additionally, finding new financing options – particularly for emerging economies and developing countries – to access cheaper investments in clean energy futures will be most critical in the years to come. The longer the worldwide and regional Covid-19 pandemic lasts and the longer the economic recovery will be postponed into the future, the bigger the financial constraints for the state to fund a faster energy transition and sustainable development.

In ASEAN, Indonesia – with its more than 270 million population spreading across 17,000 islands – will play the most critical role in the coming years. By mid-century, it might become the world’s fourth-largest economy and has a young population, abundant natural resources, a vast untapped renewable potential, and an ambition to become a major actor in the future global energy system. By holding the presidency of the G20 in 2022 and assuming the Chair of ASEAN a year later, Indonesia’s policies and leadership will be crucial for defining future energy and climate policies, not only for itself.