Still waiting for peak coal

Declining coal consumption in the United States and Europe is expected to be offset by continued demand growth in China and the rest of Asia, blunting hopes for the energy transition.

In a nutshell

- Worldwide coal capacity and consumption continue to climb

- Asian demand growth is outpacing cuts in Western economies

- China’s appetite for transitioning from coal will set the global pace

Despite the climate pledges struck at the COP28 summit last December, global coal has not yet seen peak demand. While coal demand is declining in the United States and might decrease in the European Union this year, global coal consumption still rose by 1.4 percent in 2023, up to a record 8.5 billion metric tons. Capacity for coal power plants currently in development increased by 16 percent.

Even in Europe, Russia’s disruption of gas supplies sent its coal consumption up by 0.9 percent last year, to 448 million tons. For 2023, the EU’s coal consumption had been forecasted to grow by up to 2 percent. And in Asia, coal consumption could still grow for some years, with its rising demand outpacing the combined structural declines of European and American consumption thanks to their phaseout policies.

Reality check

Worldwide, more than 107 countries and 2,000 entities are using coal across roughly 13,800 coal units. Some 204 new coal power plants are currently under construction, another 93 such projects have been announced and 260 new ones are in the pre-construction stage. Worldwide coal use still generates 36 percent of global electricity production, reaching a new record of 10,440 terawatt hours (TWh) in 2022.

It is the primary energy source in China, India, Indonesia and many other countries. China, India and Indonesia combined account for about 70 percent of worldwide coal demand. Together with ASEAN, the figure rises to 76 percent of global consumption – contrasting the U.S. and EU, whose share of global consumption is projected at 8 percent in 2024 (down from 40 percent 30 years ago).

Facts & figures

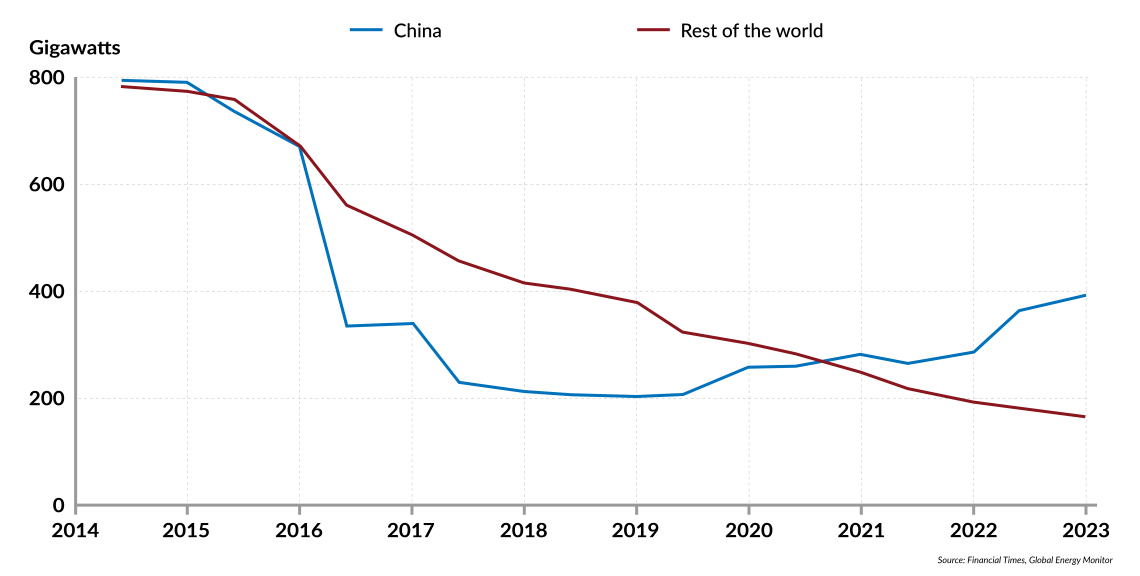

Coal plant capacity in development

The U.S. and Europe are at the forefront of efforts to phase out coal in the medium term. Between 2000 and 2020, U.S. electricity generation from coal declined steadily from 2,000 to 770 TWh, due to the American shale gas revolution and the expansion of renewables. With added weakness in electricity demand, U.S. coal consumption fell a further 7 percent in 2022 to 457 million tons (mt).

The EU aims to cut its emissions 55 percent from 1990 levels by 2030 and seeks to speed up a coal phaseout in some member states. For 2023, its coal production has been estimated to decline by some 8 percent to 321 mt.

However, Asia’s coal market is forecasted to continue expanding for at least several years. Although China has pledged to stop building new coal power plants abroad as part of its Belt and Road Initiative (BRI), domestic coal demand is still rising. It has increased its coal imports during the last two years and has decided to build new plants.

China’s role

China alone accounts for more than 50 percent of global coal demand. It is the world’s largest coal producer, at 4.66 billion tons in 2023 (up 2.9 percent from 2022) and the largest coal importer, with a record high of 474.42 mt last year. Coal accounted for 56.2 percent of its primary energy consumption mix in 2022. From 2000 to 2020, China’s electricity generation from coal soared from 1,000 TWh up to 4,775 TWh.

According to some observers, China could achieve peak national carbon dioxide emissions by 2030, a few years earlier than officially planned some years ago, due to the rapid expansion of renewables. But its coal consumption – the largest source of CO2 emissions by far – is still rising. In 2022, Chinese coal demand grew by 4.6 percent to a record high of 4.52 billion tons, mirrored by coal production and coal imports. With heatwaves and drought decreasing hydropower generation in recent years, and a greater policy emphasis on energy supply security and the goals of autonomy and self-reliance, Beijing has accelerated coal power generation.

Since President Xi Jinping pledged to “strictly control” coal power projects in April 2021, China has approved 182 new projects with a capacity of 131 gigawatts (GW). In 2022, China approved for construction six times more coal power projects than the rest of the world combined. As of last November, 209 new coal power projects with a total capacity of 243 GW were either under construction or permitted by the government. Authorities have also revived 8 GW worth of previously shelved coal initiatives.

Several Asian countries are seeking to reduce their geopolitical dependence on costly, uncertain oil and LNG imports from the Gulf region and OPEC+ exporters.

In all, China accounts for 72 percent of worldwide planned, not yet built capacity. Its additional coal capacity might further grow up to 270 GW by 2025, before any potential decline begins in 2026, as promised by President Xi. With both the newly planned but not yet approved plants and those already being built, China has 394 gigawatts of new coal power capacity awaiting realization.

According to a survey of Chinese officials and executives, China has a five-year window of opportunity to add carbon-intensive capacity. State-owned enterprises prioritize market share over profitability. Coal is still seen as the cheapest energy source to ensure that the electricity supply is guaranteed and not disrupted, coming after years of repeated power blackouts in factories and electricity shortages, particularly in the southwestern provinces. For provincial leaders, a power blackout of just one or two hours is much more costly than billions of dollars of investment in “stranded assets.” Chinese state planners have also assured coal power producers of guaranteed payments based on installed capacity.

Replacing older coal power plants with new and more efficient ones contributes to lower emissions, but it also leads to longer-term consumption of coal and thus high emissions, albeit at lower rates. China and India also raised their coal imports in 2022, with both countries accounting for around 50 percent of all worldwide imports. Beijing even ended its unofficial coal ban on Australian imports last year.

More Asian consumption

Beyond China, 41 other countries have coal projects in the pipeline, many of them in Asia. India, Pakistan, Indonesia and Kazakhstan hit new records in coal production and consumption levels in 2022. All are expected to increase coal consumption and build new coal power plants, which could add several hundred gigawatts of new coal capacity.

These countries have relied heavily on coal for power generation. They are confronted with old, inefficient coal power plants, some built 40 years ago or more. They have reached the end of their useful operating age and need replacing for an era in which electricity demand is anticipated to surge.

For these and other traditional coal producers, domestic reserves remain widely available at relatively cheap prices. They guarantee baseload security as they operate 24 hours a day – in contrast to solar and wind, which need expensive backup systems using fossil fuels or nuclear power.

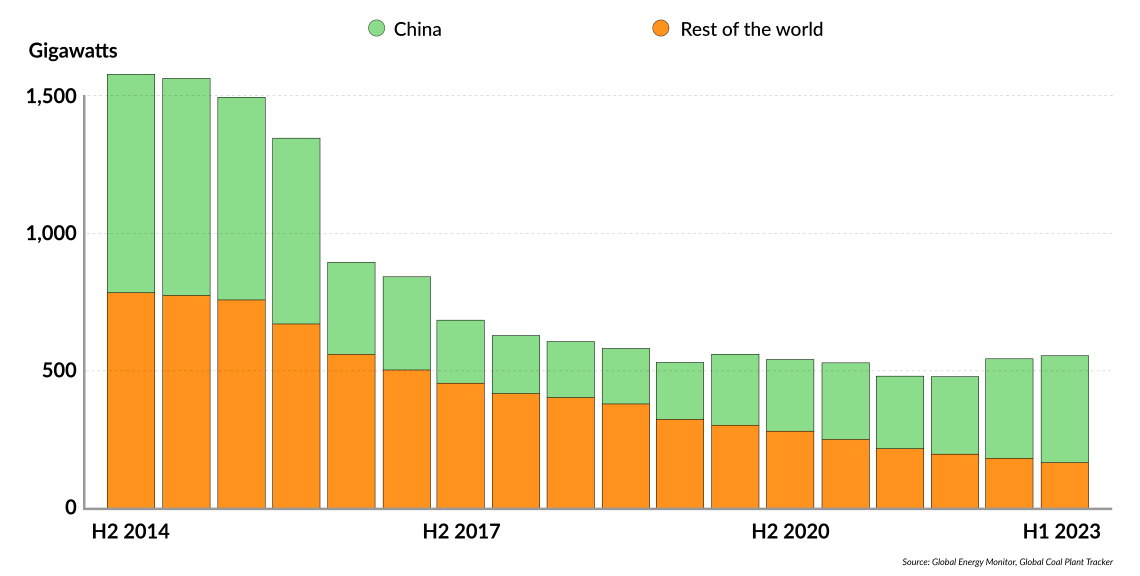

Facts & figures

Coal plant capacity under development

Besides China, India is the most important country for the coal outlook. India is facing a 30 GW capacity deficit in the face of rapidly rising electricity demand through 2030. Despite international pressure, New Delhi has asked private companies to mobilize investments into new coal plants. As much as 58 GW of new coal capacity is already coming to the market. Coal consumption grew by more than 8 percent in 2022, to a total of 1.155 TWh. Other than China, it is the only country worldwide to have crossed the 1-billion-ton mark. By 2027, India plans to boost coal production to more than 1.4 billion tons, and further to over 1.5 billion tons by 2030.

Pakistan plans to quadruple domestic coal power capacity, as building new gas-fired power plants and importing costly liquefied natural gas (LNG) have become too expensive amid geopolitical shocks. At the same time, it will also boost solar, hydro and nuclear capacities. As in India, the government is being forced to cope with a gap between installed generation capacity and exploding demand. Due to robust economic growth, Indonesia’s coal demand is also increasing, up 36 percent in 2022. Bangladesh nearly tripled its coal-fired power output at the expense of cleaner fuels, due to economic problems and the weakening of its currency.

These Asian countries are also seeking to reduce their geopolitical dependence on costly, uncertain oil and LNG imports from the Gulf region and OPEC+ exporters. This benefits Russia, as Moscow seeks to become the world’s largest coal exporter (as outlined in a 2021 coal strategy) in addition to its planned expansion of oil and gas supplies.

Phasing out King Coal?

Between 2014 and 2020, the number of planned coal projects in the world’s 10 leading coal-powered countries – excluding China – had already shrunk by around two-thirds.

The G7 has promised to help developing countries stop new coal plant construction (even if some members still plan to rely on them in the future and to introduce “clean coal” technologies). Many global financial institutions and insurance companies have committed themselves to coal divestment by 2030 or 2040, a group that has doubled in the last three years since capital markets have redefined coal as a risky investment.

Even China has ended plans to build 15 coal power plants abroad, though most of these projects have been canceled for domestic policy reasons. By doing so, Beijing fulfilled a September 2021 promise, alongside similar pledges by Japan and South Korea, which had also financed and built coal power plants abroad. While Japanese coal demand remained rather stable in 2022, it was expected to decline by 1.9 percent in 2023 – similar to the estimate for South Korea, of a 2.8 percent fall.

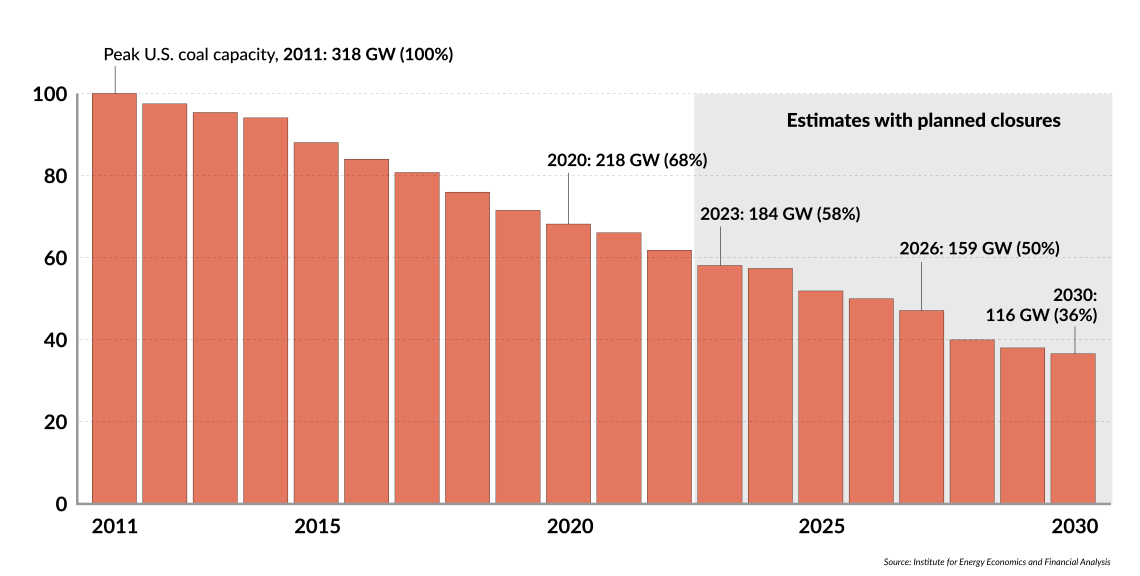

Facts & figures

U.S. coal capacity

In 2023, coal power never made up more than 20 percent of the U.S. energy mix in any month. Coal mining output there is expected to fall 25 percent this year, from 581 million tons in 2023 to 466 million tons in 2024. No new coal power plant has been constructed in the U.S. since 2014.

2022 saw surging global coal demand, combined with import bans imposed by China against Australian coal and by the EU, Japan and South Korea against Russian coal (the three countries were together previously buying some 40 percent of Russia’s coal exports). This resulted in supply shortages and an exceptionally tight global coal market, with unprecedentedly high prices. Today, those prices have returned to normal levels.

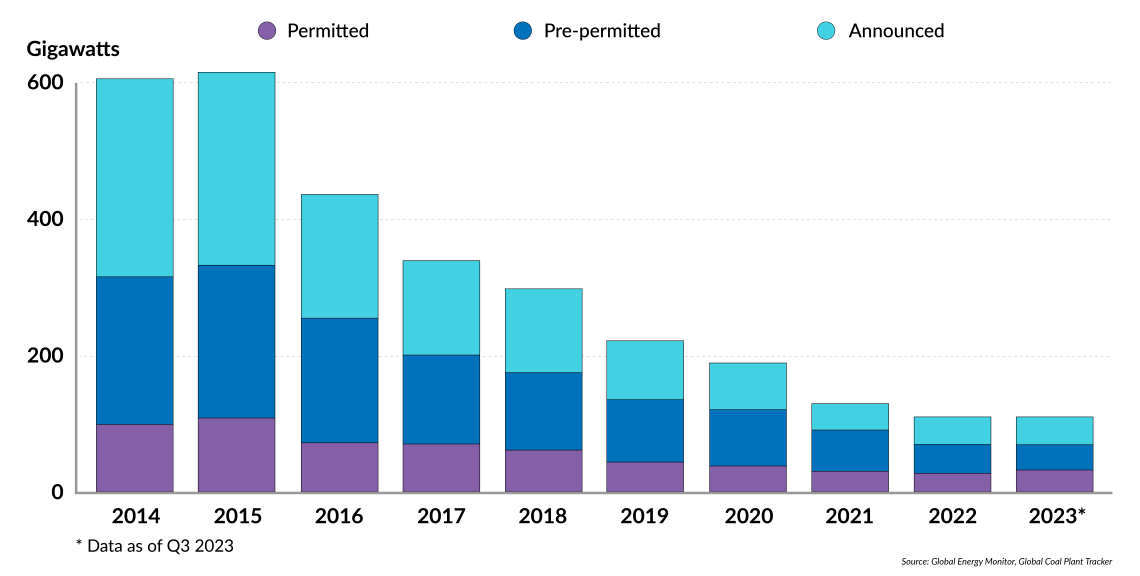

Facts & figures

Proposed coal-based power capacity, outside of China

Headwinds

Even the G7 countries – which account for 15 percent of coal power plants operating worldwide, with 323 gigawatts of installed capacity – have not yet settled on their coal exit strategies for 2030. While G7 members have basically agreed to speed up the phaseout of coal by that year, less than half of the grouping’s coal power capacity had a scheduled retirement plan announced by end-2023. To achieve the Paris Agreement climate goals, the G7 must retire an average of 40 GW annually by 2030 – more than two and half times the 16 GW reduction they achieved in 2022.

In its most recent coal report, from 2023, the International Energy Agency (IEA) forecasted that global coal demand could peak within the next two years and then steadily decline. But international coal prices have soared in recent years. The world’s 20 largest coal mining companies reached a record $97.7 billion in total earnings in 2022 (compared with “just” $28.2 billion in 2021). This has renewed the interest of hedge funds in purchasing shares of coal mining groups and making investments in new coal power construction, in the conviction that the decarbonization process will now take longer.

Even Germany will not likely be able to phase out coal by 2030 as previously intended. Its plan to build more than 50 new gas power plants as a backup capability for expanded intermittent solar and wind power was only ever feasible by subsidizing construction (with assessed costs up to 60 billion euros), as their limited operation time of a few hours a day is commercially unprofitable for private companies. That plan has now become unrealistic in light of new constraints on Germany’s state budget, after its highest court ruled that 60 billion euros in envisaged deficit spending must be scrapped.

Scenarios

Major fossil fuel exporters such as Russia, China and Arab OPEC countries made clear prior to COP28 that a phaseout of all fossil fuels is not realistic, and participants only agreed to a non-binding formulation of “transitioning away from fossil fuels in energy systems, in a just, orderly and equitable manner.” But over the next several years, the decline of coal consumption in the U.S. and Europe is still expected to be offset by continued demand growth in Asia.

While the IEA predicted in 2023 that global coal demand would peak within the next two years, this is not at all sufficient to achieve the critical 1.5-degree Celsius target of global climate policies. China plays the pivotal role and is the most important actor in combating climate change. Whether Beijing likes it or not, it will set a precedent for other countries.

Less likely: Leading China

In a rather unlikely scenario, China would stop building its 209 new coal power plants already under construction or permitted by the government. Other countries would follow China’s example, which would hasten global decarbonization and the phasing out of coal in their energy policies.

More likely: Slow progress

In a more likely scenario, the global phaseout of coal will take place over a longer period, with different speeds between Western/OECD countries and Asia. This is especially true for China and India, which will opt for “clean coal” projects and those including carbon capture/storage technologies to decrease carbon emissions while still using coal.

For industry-specific scenarios and bespoke geopolitical intelligence, contact us and we will provide you with more information about our advisory services.

Sign up for our newsletter

Receive insights from our experts every week in your inbox.