Oil markets: Relative stability amid geopolitical strife

Multiple factors stopped oil prices from hitting triple digits, contrary to what many forecasters had anticipated.

In a nutshell

- Most analysts expected oil prices to rise sharply in late 2023

- Supply growth outside OPEC contributed to lower prices

- Current forecasts disagree on how much demand to expect

Global geopolitical friction has intensified since the invasion of Ukraine. In October 2023, Hamas attacked Israel, sparking another war in Europe’s immediate neighborhood. Shortly after, Houthis began attacking ships crossing the Red Sea, prompting Western powers to retaliate against the Iranian-backed militia in Yemen. Iran has seized an American oil tanker off the coast of Oman. Not long ago, any tension in the Middle East, the largest oil and gas supplying region in the world, would send global oil prices soaring. Yet, oil prices have barely taken notice, ending 2023 at less than $78 per barrel and barely hitting $80 per barrel in January this year, despite several production cuts made by OPEC+ to prop them up.

Today, there is no end in sight to the fighting in Gaza, on top of another war involving a leading oil producer. After the invasion of Ukraine, Russia was hit by heavy sanctions directly targeting its oil trade. Producers like Venezuela and Iran are also under sanctions curtailing their oil trade. No wonder many analysts warned of spiking oil prices, with some expecting them to hit triple digits by the end of last year. But they were proven wrong.

Facts & figures

OPEC and OPEC+

OPEC+ is an alliance of OPEC members and additional non-OPEC oil-producing nations. Formed to regulate the supply of oil with the declared aim of “stabilizing the market,” OPEC+ works through coordinated production cuts or increases.

Current OPEC members are Algeria, Congo, Equatorial Guinea, Gabon, Iran, Iraq, Kuwait, Libya, Nigeria, Saudi Arabia, the United Arab Emirates and Venezuela. (Angola exited from OPEC in December, following earlier departures of Ecuador in 2020, Qatar in 2019 and Indonesia in 2016.)

OPEC+ includes Azerbaijan, Bahrain, Brunei, Brazil, Kazakhstan, Malaysia, Mexico, Oman, Russia, South Sudan and Sudan.

This does not mean that geopolitics have become irrelevant to oil markets. But the current times call for a more comprehensive assessment of the market fundamentals that are acting as headwinds and dampening the geopolitical risk premium.

From bullish to bearish price forecasts

The latest 2024 oil price forecasts for Brent – the global benchmark for crude oil – from major financial institutions and forecasting agencies have clearly turned more bearish. They range from a low of $75 per barrel from the usually conservative CitiBank to $95 per barrel. Interestingly, traditionally bullish Wall Street banks such as Goldman Sachs and JP Morgan have set moderate figures. Last year, Goldman’s forecast had oil prices hitting $95 in December 2023, then averaging $92 in 2024. In December 2023, however, the bank announced it expects the oil price to average $81 in 2024.

Similarly, in early November 2023, JP Morgan published a note asking “Will oil prices continue to rise?” The bank’s answer was that “in short, most probably … we envisage an emerging supply-demand gap beyond 2025, coupled with strengthening bottom-up sector fundamentals.” A few months later, the bank changed tack and now expects $83, in line with the Energy Information Administration, which downgraded its previous estimates by $10 per barrel.

Revising oil-price forecasts is a common practice to accommodate changes in market conditions. These recent adjustments reflect growing concerns about certain market dynamics that are putting downward pressure on prices.

Uncertainties over future demand and economic health

One of the factors that has caused this divergence in outlooks is expectations in oil demand growth, which in turn is largely determined by the health of the economy.

The gap is clear in data from the International Energy Agency (IEA) and OPEC’s monthly oil market reports. In its January 2024 report, the IEA expected oil demand growth to decelerate by nearly half this year, reaching 1.2 million barrels a day compared to growth of 2.3 million barrels a day in 2023. In contrast, OPEC expects oil demand to remain strong, growing at a “healthy” 2.2 million barrels a day, twice the IEA’s estimates. In both forecasts, Asia and China in particular account for the lion’s share of that growth. But this aspect is far from certain.

More on energy markets

China is the world’s second-largest oil consumer after the United States. It has been the main growth engine for oil demand since the beginning of this century and is expected to remain so for many years. When in December 2022 China announced it was abandoning its zero-Covid policy, most oil-market observers expected a significant boost to oil demand and prices accordingly. However, the following months gradually unveiled structural problems in the economy: a heavily indebted property sector, high youth unemployment and low consumer and investor confidence. These problems are unlikely to dissipate overnight. A slower growth of 4.2 percent for the Chinese economy is therefore expected this year, compared to 5 percent last year – the lowest in decades.

Facts & figures

Global oil supply and demand

- Global oil demand growth slowed to 1.7 million barrels per day (mb/d) year-on-year in the fourth quarter of 2023, well below the 3.2 mb/d rate registered during the second and third quarters of last year.

- According to OPEC, non-OECD oil demand is expected to increase by around 2 mb/d, led by growth in China, India, the Middle East and the rest of Asia.

- China is the world’s second-largest economy after the U.S. In 2023, its population decreased for a second year in a row to 1.4 billion people.

- Over the past decade and a half, China has been the main driver of the world’s economic growth, accounting for 35 percent of global nominal GDP growth, while the U.S. accounted for 27 percent (IMF).

- In 2023, the U.S. accounted for two-thirds of the 2.2 mb/d non-OPEC+ expansion.

- Non-OPEC+ production will dominate growth in 2024, accounting for almost 1.5 mb/d.

OPEC’s influence on supply-side dynamics

On the supply side, the landscape is divided: on one hand, OPEC+ and on the other, non-OPEC suppliers.

Since 2022, OPEC+ has announced several production cuts, including voluntary ones by key members such as Saudi Arabia and Russia, which are the group’s largest producers and have carried the bulk of the reductions. The latest round was announced in December 2023, effective for the first quarter of 2024.

However, the last meeting of the year failed to impress the market for several reasons. First, the initial delay of the meeting, albeit brief, was reported by media outlets as a result of internal disagreements. Some African states, including Angola and Nigeria, were resisting having their production quotas reduced. When the meeting did take place, Angola, which joined the group in 2007, announced it was leaving the group. Angola is not the first country to leave OPEC – Qatar did so in January 2019, among others. However, such exits are still exceptional.

Facts & figures

Furthermore, the timing of Angola’s exit at this tricky phase for oil markets has raised doubts about the cohesion of the group and therefore its influence. Second, and more importantly, the cuts announced were not perceived as significant enough to alter the course of prices, especially when Saudi Arabia and Russia simply extended their previously announced reductions. Meanwhile, within OPEC, production of Iranian oil, which is exempt from any quotas, continued to increase.

But the key factor that shaped oil supplies in 2023 and is expected to continue to do so this year has been the rapid growth outside OPEC+, particularly from the U.S. – which once again defied expectations and reached a new output record in 2023 – as well as from other producers like Guyana and Brazil. It is worth noting that although the announcement was made at the December OPEC+ meeting that Brazil would join the group, the Latin American producer clearly stated that it would not agree to any production restrictions.

Although non-OPEC+ supply growth is forecasted to decelerate in 2024, its growth is still expected to exceed demand, increasing downward pressure on prices. OPEC+’s ability to maintain solidarity and discipline will be essential if it wants to ensure that prices do not begin sliding downward.

Scenarios

Even when oil supply does not decrease, fears that it might usually lead to higher prices. At the outset of the war in Ukraine, some institutions forecasted prices exceeding $300 per barrel. Many also warned of triple-digit prices after the outbreak of the Israel-Hamas war.

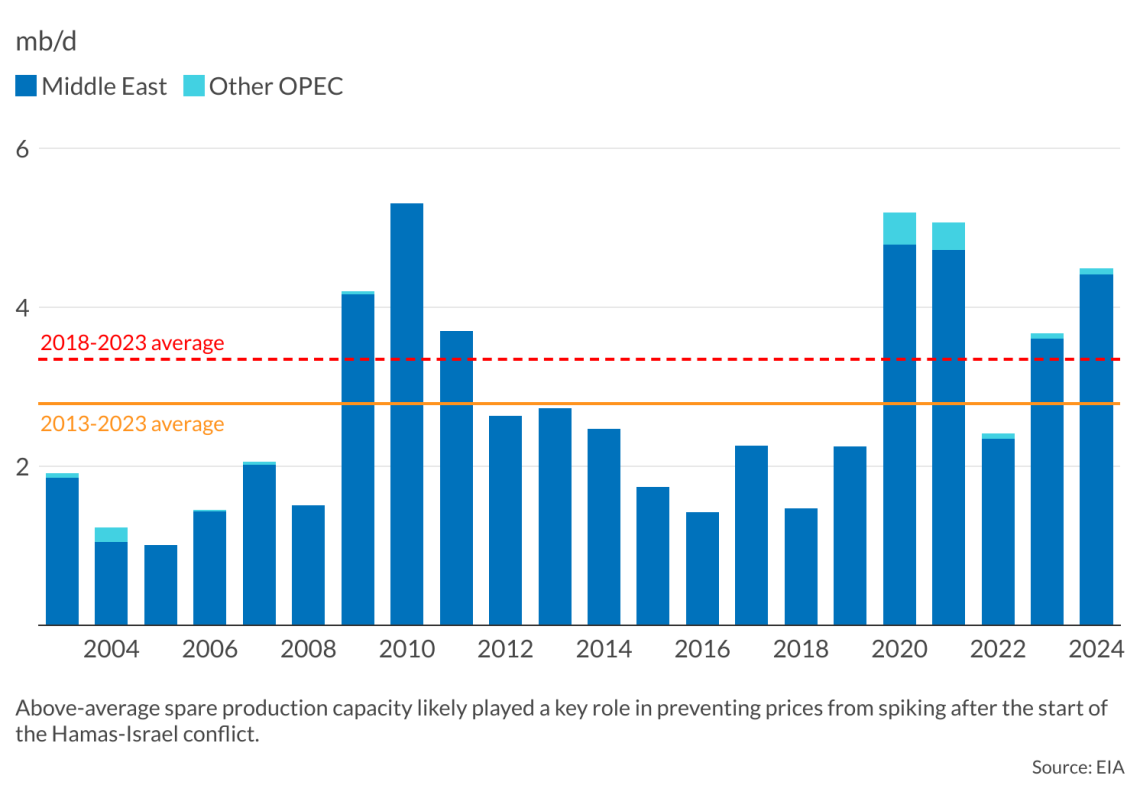

The impact of geopolitics on oil markets also depends on how much of a “safety cushion” there is in the system. That cushion is spare capacity, defined as “the volume of oil production that can be brought online within 30 days and sustained for at least 90 days.” In its note published in November 2023, JP Morgan warned that “diminishing spare capacity introduces an additional risk premium of around $20-30 per barrel.”

The world’s spare capacity of oil is concentrated in OPEC countries. The more the group cuts production, the more it replenishes that capacity. Today, OPEC’s spare crude oil production capacity is well above both the last five- and 10-year averages and is at the third-highest level in more than 20 years. By cutting production to stop prices from sliding further, OPEC has also helped in stopping prices from spiking. Whether this was carefully engineered or simply a consequence of the output reductions, the organization has delivered on its long-trumpeted raison d’etre of achieving market stability.

Very likely: Politicians will attempt to prevent supply shocks ahead of elections

The current prevailing sense of plenty and bearish sentiment dominating the outlook for oil markets for this year can still change if geopolitical tensions – especially in the Middle East – escalate and cause a significant loss of supply. However, many key players are likely to push hard to avoid such a scenario. 2024 will be the biggest global election year in history, with the U.S. presidential elections being the closest watched. A supply shock and subsequent high oil prices would not bode well for those seeking electoral victory.

For industry-specific scenarios and bespoke geopolitical intelligence, contact us and we will provide you with more information about our advisory services.

Sign up for our newsletter

Receive insights from our experts every week in your inbox.