Why combating inflation will not be easy in Europe

Profligate government spending in response to whatever “crisis” comes along and unsound monetary policies will keep inflation needlessly high.

In a nutshell

- Real interest rates remain negative in much of Europe

- Many governments routinely flout deficit and debt rules

- Central banks do not feel empowered to combat inflation

A look at economic policy in Europe today offers a gloomy and rather puzzling picture. While inflation has been climbing for months and is now touching 10 percent in the eurozone (and running at unprecedented levels of more than 20 percent in some member states), the European Central Bank’s policy rate did not get above zero until September this year. Until then, it had been idling in negative territory for the better part of 10 years.

And it is not just the eurozone. The non-euro European Union countries are also experiencing remarkably high inflation. In none of them does the policy rate exceed the current inflation reading. Real interest rates (the central bank rate minus inflation) therefore remain negative in many European countries, even more so than during the pandemic.

Governments, with some notable exceptions, are meanwhile continuing to amass new debt. Ratios for debt to gross domestic product (GDP) are comparable with those at the end of World War II not only in Europe, but throughout the developed world.

Anyone looking at this picture solely through the lens of macroeconomic textbooks would probably shake their head in disbelief. But economics alone is not enough to understand where we are today. On the contrary, a knowledge of economics may paradoxically get in the way.

When the rules do not work

At the beginning of the process of deeper European economic and monetary integration, the future euro area members adopted a set of rules intended to curb politicians’ fiscal profligacy. To ensure discipline, government deficits and debts were capped at 3 percent and 60 percent respectively.

These relatively simple rules were constructed in 1997 and called the Stability and Growth Pact. They were mainly intended to ensure “monetary policy dominance” – a situation where central bank decision-making on interest rates and exchange rates is not paralyzed by irresponsible government fiscal policy and where debt problems in one part of the euro area do not prevent stabilization in other parts and do not easily spill over from neighbor to neighbor.

It soon became apparent, though, that it would not be all that simple. How can such strict and restrictive rules be enforced among sovereign states? With great difficulty.

Analyses have shown that compliance with the fiscal rules was only around 50 percent between 1998 and 2019. And this score excludes the Covid-19 pandemic years when the main fiscal policy rules were switched off throughout the EU.

No revisions of the original rules (the six-pack and two-pack reforms), no stronger enforcement mechanisms and no attempts to rewrite the rules to make them more consistent with the logic of the business cycle have led to greater compliance. What is more, these changes have made the rules so complex that even those who are meant to apply them no longer understand them. That is another reason the willingness to follow them has fallen.

This is having a fundamental impact of course. Monetary and fiscal policy experts know full well that the contagion of irresponsibility almost always goes from the government to the central bank, not the other way around. When the International Monetary Fund’s experts travel around the world to determine where macroeconomic problems might be festering, they always start with the government and investigate its behavior, decisions and blunders. That is why it is often joked that IMF stands for “It’s Mostly Fiscal” – the monetary fund is to a substantial extent a fiscal fund.

When public budgets go wrong, the government finds it more difficult to finance itself or even becomes unable to service its debt. The central bank takes a hit in the next round. It is implicitly or even explicitly required to intervene to help the government, calm the markets and reduce the unsustainably high returns on government debt. These are all things we are very familiar with in Europe.

In such a situation, the desirable and, in the early days of the euro, well-intentioned monetary policy dominance ends. Fiscal policy dominance then begins, which is highly undesirable because it ties the central bank’s hands or even completely deprives it of the ability to act. It restricts it most of all when its actions are most needed and would be most effective, such as at times of high inflation.

Few doubt that the growing fiscal policy dominance is one of the reasons why monetary policy in the eurozone cannot be more aggressive in combating inflation, why conversely it had to be so overactive during the fiscal crisis in the south of the eurozone, and why it now has to come up with such highly unconventional measures as the Transmission Protection Instrument (TPI), which is intended to prevent growth in interest rates from having a stronger effect on riskier, more over-indebted member states.

Fiscal policy is now so dominant that the single currency area needs multiple monetary policies.

The long run as the sum of a series of short runs

Looking back at the single monetary policy, this is exactly what we see. Through gradual, stepwise breaches of the rules, deviations from standards and noncompliance with obligations, first by just some members and then progressively by the majority, the monetary integration project has arrived at the situation it wanted to avoid. The excessively large debts of the largest borrowers – and the biggest single borrower in any country is the government – are destroying monetary dominance and, as seen so many times in history, giving rise to government and fiscal policy dominance.

In the end, fiscal policy is more acute, more immediate and more understandable, as it is made by elected politicians directly for their voters. It is thus typically focused more on the short run. But monetary policy should not be like that. The Stability and Growth Pact was designed as a long-run tool.

There may be a good reason for each “crisis.” But if we are always able to define at least some sort of crisis, we also always have a good reason not to look to the long run.

As the last 20 years have shown, however, the long run is only ever the sum of a succession of short runs. And in those short runs there are always enough good reasons to borrow a little more than we have, spend a little more than would be responsible and sacrifice a little more of the future for the present than would be sensible.

Politicians typically speak of a “new reality” that makes it impossible at a particular moment to respect the rules of responsibility. Such “new realities” have included the great financial crisis, then the fiscal crisis and later the migration crisis. Recently we have had the pandemic crisis, and now there is the energy/war crisis. And in the absence of those, it is the climate crisis. It is always something.

There may be a good reason for each “crisis.” But if we are always able to define at least some sort of crisis, we also always have a good reason not to look to the long run.

The super short-run approach to budgets was summed up brilliantly by Charlie McCreevy, the former Irish minister of finance and later European commissioner: “When I have the money, I spend it. When I do not, I do not.” We have taken his maxim to the next level: “When I do not have the money, I borrow it.”

The current energy crisis is another example of all this. There is no doubt that the events of recent months have sent energy prices to dizzying heights. But instead of addressing the roots of these problems, policymakers are again only able to tackle the immediate impacts in the short term.

In Europe, this means compensating consumers or cutting indirect taxes, measures that are very costly and sending budgets back into large deficits.

What has almost been forgotten in the current turmoil is that when we are truly at war, taxes go up, not down. The welfare state model, however, does not allow this.

Guns or butter? Both

Economists have long been aware of the “guns or butter” dilemma – the situation where, in difficult times, a nation must choose whether to spend public money on defense and security (including energy security) or on maintaining current wealth.

It is a trade-off, but it is one which in Europe we are “resolving” by offering the electorate both weapons and butter – by taking on more debt.

Countries are copying each other when it comes to adopting measures to “mitigate” the impacts of inflation. But these measures are often purely inflationary, not anti-inflationary. They are merely increasing the quantity of money in the economy. Governments are supplying this money by borrowing, and the resulting debt is being financed either by commercial banks or by central banks through the creation of new money.

The European debt crisis after 2010 showed that when it comes to keeping our houses in order, we are not as harsh on ourselves as we are on the neighbors we have lent money to.

All this is being exacerbated by the lack of anyone to keep discipline. The developed countries still have a dominant influence in the IMF. After a fashion, they act as policy enforcers regarding less developed countries, as they have the political and financial leverage to do so.

But how can the developed countries be kept in line? Who among them will enforce rules and responsibility? The European debt crisis after 2010 showed that when it comes to keeping our houses in order, we are not as harsh on ourselves as we are on the neighbors we have lent money to.

This thorny question remains unanswered if we refuse to let the market enforce discipline and if we always smooth its interventions with central bank assistance because we fear the severity of the punishment.

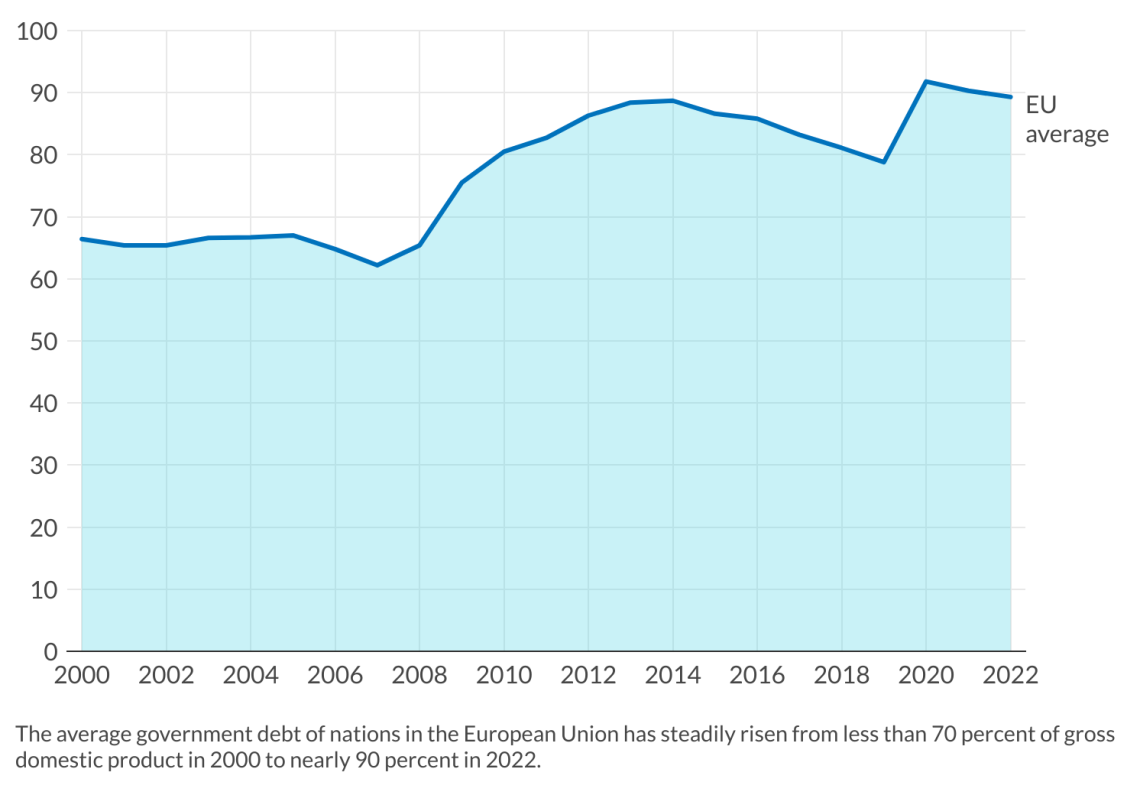

The urgency of the issue of enforcing responsibility is being increased by the bad example effect. In the EU, more and more finance ministers from traditionally fiscally conservative countries are logically asking: Why should we keep our debt below 60 percent of GDP when most large countries are above that criterion, the average debt-to-GDP ratio in the EU is 90 percent and no one is getting into trouble?

The contagion of irresponsibility has not ended. Quite the reverse: it is happening before our eyes. Fiscal consolidation is constantly being deferred to the next government.

The fact that we have no answer also indicates how long we may ultimately be fighting inflation. We have tied the hands of monetary policy and are continuing to untie those of fiscal policy. So, unless there is a strong demand shock, it may truly take a long time to rein in inflation.

Scenarios

The first and most likely scenario assumes that fiscal policy will remain dominant and monetary policy will continue to have a limited ability to eliminate the inflationary pressures in the economy. Relaxed fiscal policy will conversely fuel the inflation pressures and the debt-to-GDP ratio will be stabilized not through desirable fiscal restraint and respect for the rules, but through debt reduction because of higher inflation and nominal GDP growth. Moreover, the fiscal rule will most likely be softened. The probability of this scenario is 45 percent.

A second and less likely scenario is based on the expectation that impending risk will lead to a large central bank bailout that will save the day in the short term and, after a pause, allow the current fiscal policy to continue. The probability of this scenario is 35 percent.

A third and least likely scenario assumes that fiscal policy discipline will be enforced abruptly by the financial market, which, in an instant shift of the economy from the existing equilibrium to a new one, will force national fiscal policy to adjust sharply and return to responsibility. This shock will also help reduce inflation, but at the cost of losses in the real economy. The probability of this scenario is 20 percent.