U.S. interest rates: Where will they take us?

President Trump worries that the Federal Reserve is raising interest rates too quickly. In fact, the Fed has engaged in moderate tightening so far. By mid-2019, it is likely to end the cycle and hold rates steady. At that point, Trump will not be able to blame the Fed for any fiscal trouble and will have to implement reforms to spur growth.

In a nutshell

- Interest rates in the U.S. have been rising at a slow to moderate pace

- The Fed is likely focused on restricting money supply, not on a specific interest rate

- The tightening will probably come to an end in mid-2019

- If U.S. debt remains high, the dollar will continue to appreciate

Despite considerable clamor calling for a stop – and a reverse – to expansionary monetary policy, during the past year new United States Federal Reserve Board Chairman Jerome Powell has proceeded rather cautiously.

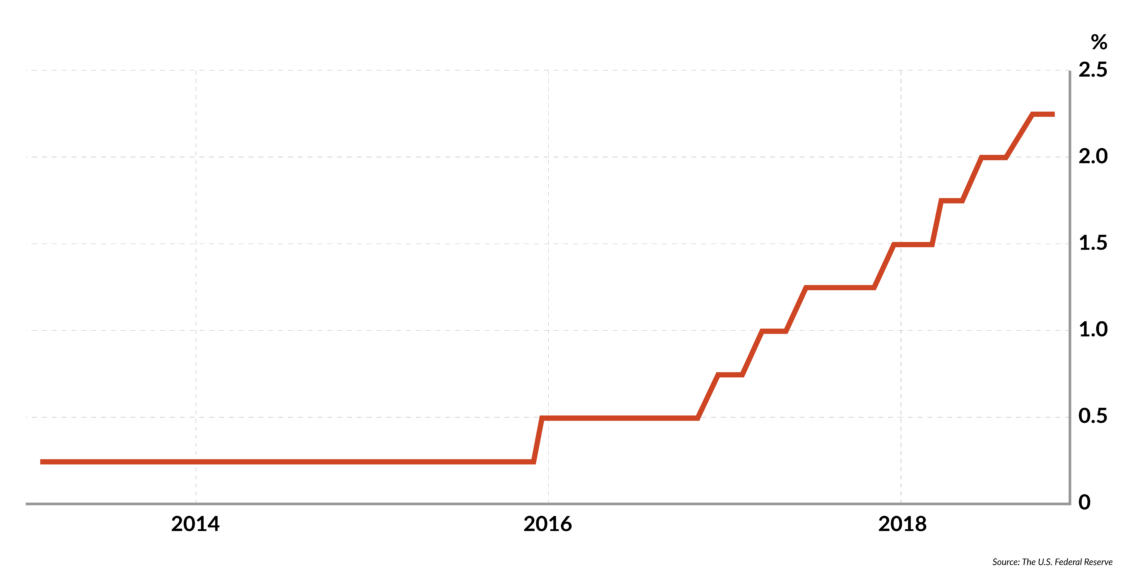

For example, since the beginning of this year until mid-December, the federal funds rate – the short-term annual rate of interest controlled by the Fed – rose from 1.42 percent to 2.25 percent. A rough measure of how long-term interest rates have moved is the yield on the 10-year U.S. Treasury bonds, which during the same period has progressed from 2.45 percent to 2.85 percent. At the same time, the annualized rate of inflation in October was 2.5 percent, up from the 2.1 percent figure registered in January.

So U.S. interest rates have increased moderately, especially in real terms, and despite President Donald Trump’s complaints, they are still low. Not surprisingly, most commentators expect the American central bank to move the federal funds rate to 2.50 percent before the end of the year, and to continue along that path during 2019. Will it happen?

This report analyzes the various options and outlines the scenarios that could unfold accordingly. Future developments depend on two sets of variables. We shall briefly describe them, then draw some conclusions about what outcomes they may generate.

Policy and debt

First, one must consider what kind of policy the Fed is pursuing. It could try to keep the money supply more or less stable (say, by letting it grow by a 1 to 2 percent on an annual basis) and raise interest rates to the level required to reach that condition. From January to the end of October 2018, the money supply (M2) in the U.S. increased by some 3.1 percent. This is roughly equal to the proportional increase recorded during the same period in 2017, but significantly slower than the average yearly rise between 2014 and 2017 (7 percent).

The Fed could take aim at an interest-rate target defined in real terms, which would be bad news for all borrowers.

On the other hand, the Fed could take aim at an interest-rate target defined in real terms, which it might want to reach fairly soon, regardless of what happens in the rest of the economy. This is obviously what President Trump fears, since it would be bad news for all borrowers, and for consumers in particular – and those consumers will be deciding the presidential primary elections a little over a year from now.

A second set of issues regards the public debt. The U.S. public debt is currently above 105 percent of the gross domestic product (GDP) and rising. The public deficit is also growing. The government has estimated it at 4.7 percent of GDP in fiscal year 2019, up from 3.9 percent in fiscal year 2018. Unless GDP growth accelerates and generates higher tax revenues, the picture could deteriorate further.

Certainly, the quality of the U.S. as a debtor is not in doubt. Nonetheless, the U.S. Treasury will be selling increasingly large amounts of bonds. Potential buyers will likely require higher coupons, especially if the Chinese government cuts its purchases of U.S. securities and/or inflation rises. If one of these possibilities were to materialize, the entire interest-rate structure would move upward, regardless of what the Fed decides to do.

An end to tightening

Let us now consider the scenarios that could follow. Although most commentators believe that the Fed will continue its monetary policy tightening, we argue that the end of the cycle is not too far away. As mentioned earlier, further increases in the federal funds rate are expected and will soon become operational – in December 2018 or in early 2019. Yet, the Fed will probably be satisfied once money supply growth slows to less than 2 percent. That might happen in mid-2019. If so, the Fed will just monitor the situation and stand pat until the end of 2020 or longer. After all, recent years have shown that the cost of servicing large public debts is effective enough in restraining erratic behavior in the real economy and nipping overheating in the bud.

Facts & figures

Gradual rise

The U.S. Fed funds rate

Markets have become responsive to debt-financed expansionary policies. The short-term beneficial effects of a budget deficit are quickly eroded by rising interest rates on debt financing, by greater uncertainty and deeper worries about future troubles. If a high public debt scenario materializes, monetary authorities must only resist the temptation to engage in irresponsible money printing.

Nor is there a need to pursue fine-tuning objectives or oil the wheels of the real economy. If governments – on both sides of the Atlantic – really want to promote growth, they should consider reducing the public debt and releasing resources for productive purposes. Perhaps the message is not yet clear to all policymakers, but it will be.

Inflation is no source of worry. Although consumer price growth in the U.S. accelerated from mid-2017 to mid-2018, it now seems rather stable, at about 2.5 percent. And in contrast with what would happen if monetary hawks had the upper hand, under a do-nothing monetary policy approach tensions would subside, and a weakening dollar would make U.S. foreign-oriented companies happy.

If governments want to promote growth, they should consider reducing public debt.

Less likely scenarios would materialize if the Fed were actually pursuing a strategy targeting the real interest rate. In such a case, predictions would depend on the goal the Fed would be setting. During the past 40 years, and before the dawning of the various versions of quantitative easing, the real rate on short-term, high-quality securities was about 2 percent, and about 4 percent for long-term assets. Thus, if historical data were the benchmark, and annual inflation stayed between 2 percent and 3 percent, one could expect rising interest rates (and an appreciating dollar) for quite some time.

Scenarios

What consequences should one expect, domestically and on a global scale, if the Fed gradually raises interest rates until mid-2019 and then stops? We venture two predictions.

One regards the U.S. economy. After reaching a peak in summer 2018, GDP growth has slowed. The explanation has little to do with Chairman Powell’s monetary policy. Rather, structural variables – labor shortages and moderate productivity growth – have started taking their toll. A gradual rise in the short-term interest rates during the next six to nine months will make no difference. In fact, it will restore confidence in the Fed and eliminate one important source of uncertainty.

However, President Trump will bear responsibility for the evolution of America’s public debt and for his attitude toward future potential buyers of American Treasury bonds. He cannot rely on households, since in contrast to Europeans, Americans tend to prefer stocks and mutual funds to fixed-income securities. His relations with the buyers of treasuries in East Asia will thus play a crucial role, and blaming the Fed will not hold much water.

Indeed, even if the Fed gave way to his requests to keep interest rates low, the dollar would further appreciate because of the higher cost of debt servicing, and President Trump’s efforts to reduce the trade deficit and revive the economy through protectionism would come to nothing.

A second prediction regards Europe. Its leaders will be relieved if the rise in U.S. interest rates comes to an end sooner than expected. The lower the return on competing American securities, the lower the cost of servicing European public debts. Fewer cracks would appear in the euro. Brussels and Frankfurt would have little to celebrate though, because these benefits would not last long. The monetary problems of the euro have nothing to do with what the Fed does, but with the public-finance situations in some key countries, which are very fragile and could easily spiral out of control.