How long will high inflation last?

A return to low inflation is likely to take years, not months. Policies for stable prices require a brand of central bankers not now in vogue among U.S. and European politicians.

In a nutshell

- Increases in production will not stave off inflation

- Demand-driven pressure may remain elevated

- High prices should persist for years, not months

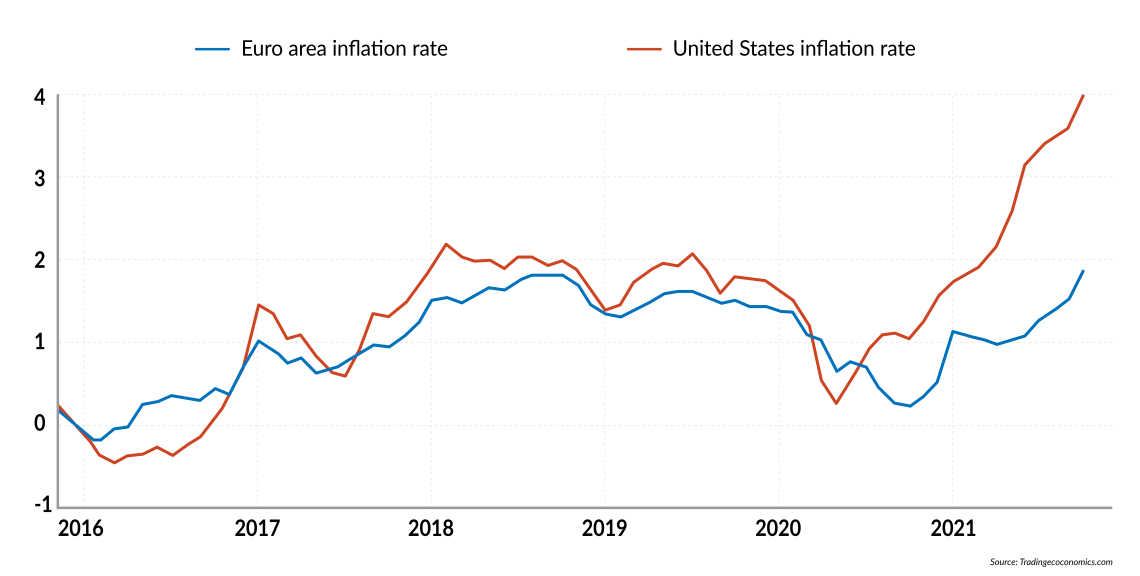

In January 2022, inflation in the United States reached 7.0 percent, up from 1.4 percent in January 2021. The data in the eurozone is better, but still alarming: 5.1 percent, as opposed to 0.9 percent one year prior. Long gone are the days when U.S. Federal Reserve Chair Jerome Powell and European Central Bank (ECB) President Christine Lagarde claimed that rising prices would be moderate, temporary and limited to certain industries.

Current predictions vary, but in general, the rate of inflation is expected to fall at least 2 percentage points by the end of this year, stabilizing at around 2 percent in 2023. Financial markets seem to agree: 10-year U.S. treasury and German bund interest rates about 1.9 percent and 0.2 percent, respectively. How reliable are these forecasts? Can we trust financial markets to predict future inflation?

Economics is not a hard science, but an exercise in logical thinking and common sense. Predictions are in fact informed guesses – sometimes colored by wishful thinking and enriched by efforts to influence market behavior. This report focuses on common sense reasoning, assesses the prevailing scenarios for declining inflation and imagines alternatives.

Conventional wisdom

According to the general view held by today’s central bankers and most prediction models, aggregate demand is the key variable that drives inflation, although some adjustments are necessary when supply shocks or unexpected events emerge. For example, most analysts say the source of the current high inflation in the U.S. is the recovery of economic activity in 2021, as people increased their spending after the pandemic crisis. Supply-chain and labor market bottlenecks ensured that the rise in aggregate demand would not be met. According to the dominant narrative today, as a post-pandemic rebound in 2022-2023 sees demand tapering off and supply bottlenecks easing, inflation should also subside.

Can we trust financial markets to predict future inflation?

The European story is similar. Although the 2021 recovery in the EU has been weaker than in the U.S., the ECB also ascribes today’s unexpectedly high inflation to a mix of soaring consumer spending and supply bottlenecks. Moreover, European authorities frequently blame higher energy prices and, oddly enough, point out that in 2020, prices were very low – suggesting that inflation just brings the general price level to its appropriate level.

According to this view, lower aggregate demand and loosened bottlenecks should characterize the rest of this year. It is not clear whether or when the ECB believes that prices in 2022 will be “just,” but its allegedly reassuring message is that inflation is simply the price to pay for a speedy transition to social justice, clean energy and sustainable growth models (whatever these expressions mean).

Strong demand

Of course, there is another way of reasoning about inflation. Aggregate demand rises if people decide to spend more, which they can afford only if they have money in their pockets and decide to exchange it for goods and services. On the other hand, supply fails to adjust if companies hesitate to increase output: e.g., if they cannot hire enough workers, decline to expand production facilities (including machinery), fail to obtain enough intermediate inputs, or simply do not approve of the rules of the game (taxation and regulation). How will these factors move during the quarters to come?

Although both the Fed and the ECB have announced that the era of profligate money printing is over, there will be no tight monetary policy. For example, the federal funds rate is 0.25 percent; even if it rose to 2.1 percent by the end of 2023, as some Fed officials expect, the real rate would still be negative. The same applies in Europe, where nominal interest rates should actually remain stable, according to ECB President Lagarde. Regrettably, this is a credible promise, since a number of highly indebted European companies and countries would suffer dramatically if interest rates went up and if predictions about low growth came true.

Facts & figures

Inflation in U.S. and Europe, 2016-2021

As a result, we may expect that this year, large amounts of money will continue pouring into people’s pockets on both sides of the Atlantic, keeping demand lively. In this light, the relevant scenarios actually depend on whether people will repeat the patterns of 2021; to what extent they will spend their liquidity, possibly further using up past savings; and whether supply bottlenecks will dissolve.

Scenarios

Taking all this into account, we can set out the following predictions:

Consumer spending will keep rising in the U.S., but at a relatively low pace. Even a modest rise in interest rates will likely discourage debt-financed consumption, while less liquidity will enter the economy. The 2021 drop in real wages will make people cautious, and stock market performance could be disappointing. Declining rates of corporate profits will ensure that the spending euphoria of the past will no longer be propelled by significant increases in individual financial wealth.

Household private spending will stabilize in Europe. Although the rate of unemployment is relatively low, nominal wages are not keeping up with inflation, and the future outlook remains uncertain (with slow growth, increasing taxation and large public deficits in some key countries). Accordingly, people will remain cautious. To be sure, they will spend more on energy, the relative price of which may increase further. But spending on non-energy goods will suffer, as money balances are absorbed by energy bills. The real handmaiden of demand will be government expenditure, through which much of the 2022 fiscal stimulus will be channeled.

Despite fading supply-chain problems, growth rates of gross domestic product (GDP) will decline in both the U.S. and Europe, probably dropping below the levels predicted by many observers at the end of last year (about 4.0 percent for the U.S. and 4.3 percent for the EU). As anticipated in a previous report, the American labor market is problematic, with companies struggling to prevent employees from quitting in search of better pay. Moreover, after having recovered from the early 2020 decline, gross fixed capital investments in the U.S. and Europe are now stable, which shows that companies are unlikely to expand their production capacity.

Large increases in production will not keep inflation low in 2022. The key question, therefore, is whether the demand for consumer goods will cool off.

Certainly, the Federal Reserve can rein in demand by persuading consumers that significantly higher interest rates are just around the corner. However, this would require Chairman Powell to make clear that monetary policy targets inflation, operates with automatic rules, and disregards the consequences for the realm of business (and growth).

If this happens, and the automatic rules are strict enough, inflation could perhaps drop to 3 percent by the end of this year and possibly lower in 2023. On the other hand, if Mr. Powell hesitates, or if people believe that he will be cautious, demand-driven pressure will remain high. Uncertainty will prevent companies from expanding capacity, and he might have to relent and pump more money into the economy.

Meanwhile, there is little room for optimism for Europe, especially in the eurozone. Inflation will stay close to current levels due to several factors: high public expenditure, as the Maastricht Treaty’s budgetary rules continue to be ignored; relatively generous monetary policy, with Ms. Lagarde’s pledge to refrain from weakening growth prospects and creating a public-debt crisis; and disappointing growth, as EU policies on regulation, taxes and climate change serve to discourage entrepreneurial activities.

Contrary to what the long-term interest rates on safe bonds seem to indicate, the conclusion is that reverting to low-inflation scenarios will take years, not months. While credible policies for stable prices require a new generation of central bankers, politicians on both sides of the Atlantic seem to favor a different stripe of candidate.