Labor markets after Covid

Economies have not come roaring back after the Covid-19 crisis due to complicated problems in labor markets. In the U.S., people’s decision not to come back to work is putting pressure on wages. In the EU, governments have to spur growth to solve financial imbalances.

In a nutshell

- Labor markets present deep economic challenges post-Covid

- Fewer willing workers in the U.S. means wages may have to rise

- In the EU, higher participation leaves little room for maneuver

The post-Covid recovery is sputtering on both sides of the Atlantic. Most analysts blame broken supply chains, and indeed, the presence of serious global bottlenecks is undeniable. Health restrictions have increased the time it takes to ship cargo across the world. Many industries are suffering from a lack of the goods they need to make their products, and the prices of many of these goods have soared. All this, however, is only part of the problem.

Not coming back

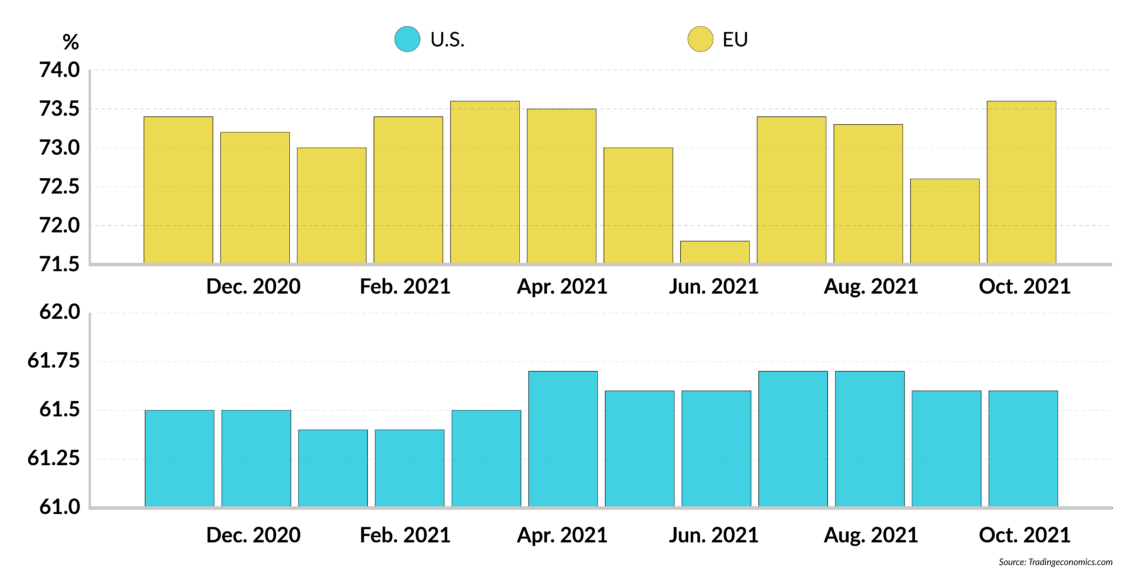

Labor markets present deeper, less transitory challenges. In the United States, even though data shows that demand for goods and services has been rising fast, the labor market remains stuck in neutral. Companies have begun trying to ramp up hiring but are running into trouble attracting workers. In October 2021, the number of employed workers in the U.S. rose by 531,000 – in line with expectations. Payrolls, however, remain 4.5 million units below January 2020, and the labor force participation rate is stuck at 61.6 percent (it was above 63 percent in February 2020). On the other hand, unemployment has dropped to 4.6 percent (it was almost 15 percent in the spring of 2020). That is not too far from the pre-Covid rate of about 3.5 percent.

The unemployment rate counts those actively looking for a job, a number that falls not only when unemployed people find work but also when they stop searching. When the latter occurs, these people exit the labor force, even if they still belong to the working-age population. That group weighs heavily on U.S. labor-market conditions: the unemployment rate falls, but that does not mean that employment is booming.Many of the workers who left the labor force are not coming back

Many of the workers who left the labor force during the Covid-19 crisis are not coming back. The low number of people looking for a job has put pressure on nominal wages. These have started to rise, possibly hitting companies’ profits. The average annual increase is 4.9 percent and is soon likely to begin increasing faster than inflation, currently at 6.2 percent.

Rising participation

The situation in the European Union is different. The EU labor force is relatively larger than the American one and is growing. In 2012, the EU labor force comprised 70.5 percent of the working-age population. In early 2020, the figure was just below 72 percent, and it has now risen to above 73.5 percent. As mentioned above, in the U.S., the figure is currently only about 61.6 percent. EU nominal wages have also followed a different path as opposed to the U.S.: since many low-wage earners in the EU lost their jobs during the Covid years, the average wage rate increased during the crisis, and has dropped during the recovery.

Broad analyses of data are always dangerous. This especially applies to the EU, where local situations present significant differences. Nonetheless, the crisis has underscored that two phenomena are at work. First, it pays to remain in the labor force in Europe, possibly because generous welfare programs are available to those who continue looking for jobs. This does not mean that all those looking for work in the EU are ready to accept any offer. But they are more likely to come back to and stay in the labor force, even at lower wages.

Facts & figures

Working in Europe, waiting in the U.S.

Labor participation rates in the United States and European Union

This explains why the EU unemployment rate is generally higher than across the pond. Moreover, it seems that workers in Europe are less sensitive to price changes than their colleagues in the U.S. In other words, EU workers are probably more concerned about having and keeping a job than whether inflation will erode their wages.

At the same time – and this is the second issue – growth in the EU is likely to attract people who are currently in the workforce but are unemployed and possibly worry that their governments could cut welfare provisions in the future. This contrasts with the U.S., where persuading the working-age population to join the labor force and accept a job will require a significant rise in real wages, at the risk of tamping down growth.

Wages vs. growth

Two preliminary conclusions follow. First, raising the labor force participation rate in the U.S. is problematic since it would require higher real wages. Such a rise could perhaps occur if labor productivity rises or corporate profits are squeezed. However, U.S. productivity over the past decade has been far from stellar, at about 1 percent a year, and it is unlikely to accelerate soon. In fact, the post-Covid recovery is slowing down. Corporate profits seem healthy, but the dramatic increase in asset prices has squeezed profitability. If higher wages pull down profits, stock values would necessarily drop, and resources to finance investments would become scarce.

The second preliminary conclusion regards the EU, where a tight labor market does not constrain growth. Its modest increases in productivity – even lower than in the U.S. – play a lesser role. The EU’s future therefore depends on how much growth it needs to solve the current economic imbalances, and eventually, on what it will take to make growth possible. Slashing subsidies to the unemployed and deregulating the labor market would be part of the answer.

Tax and spend

The American administration seems unwilling to cut public expenditure. However, it is evident that the current estimated budget deficit of 12.4 percent of gross domestic product (although better than the 2020 figure of 15 percent), is unsustainable. Higher taxes are around the corner. Members of the Biden administration and Democratic members of Congress have already called for new ways of taxing capital gains and wealth. Their demands may be just the beginning of more extensive tax rises, and the call to arms to fight the war on climate change will sugar the pill.

This policy will have modest short-term consequences. Heavier taxes on wealth will be perceived as a minor nuisance, given the significant gains accumulated recently. The labor market situation will remain tight, but less so: if the threat of stagflation materializes, weak growth will check employers’ demand for labor, and rising prices will encourage people to join the labor force.

The problem with high taxation is more severe in the long run. While more tax revenues will reduce the need for the government to print new money to finance the budget deficit, capital formation will decline, and entrepreneurial spirit will weaken.

This is not the only possible scenario. The picture for the U.S. economy could improve substantially if global trade tensions and regulatory pressure were to ease: growth rates would gain momentum and create enough room to accommodate significant increases in real wages and possibly higher tax revenues. However, the Biden administration seems reluctant to abandon former President Donald Trump’s “fair trade” protectionism and embrace free-market principles.

Financial mess

Whereas America needs to increase its labor force to propel growth, defuse future tensions and avoid major cuts in public expenditure, the EU needs faster growth to avoid collapsing under its financial imbalances: a monetary mess (inflation) overall and high public debt in some key countries. Achieving a higher labor force participation rate is not an option.

After having bashed “neoliberalism” for over a decade, the European public now believes that solutions can only come from strong government intervention, possibly harmonized and financed through public indebtedness. Free market entrepreneurship and big business are perceived as part of the problem, not the solution.

Policymakers’ decisions in the coming weeks will be crucial. Business as usual is tempting in the U.S., and likely to keep Wall Street in good shape. A slowdown in growth would actually be welcome, as it would defuse tensions in the labor market. Yet, business as usual in Europe would aggravate its current difficulties. If governments will still have to manipulate the money supply to sustain public indebtedness with low growth, soaring inflation could eventually rock the boat. The current quiet atmosphere characterizing its labor markets could quickly dissolve.