Some optimism for oil markets

The oil industry faces an optimistic outlook: A combination of several of post-pandemic factors will likely restore oil demand soon. Meanwhile, Saudi Arabia remains determined to spearhead the OPEC+ effort to boost oil prices.

In a nutshell

- An optimistic outlook for the oil industry is feasible

- OPEC+ has prevented oil prices from plummeting

- Issues with the vaccine would affect recent gains

This GIS 2021 Outlook series focuses on the opportunities that stem from the upheaval of the past year.

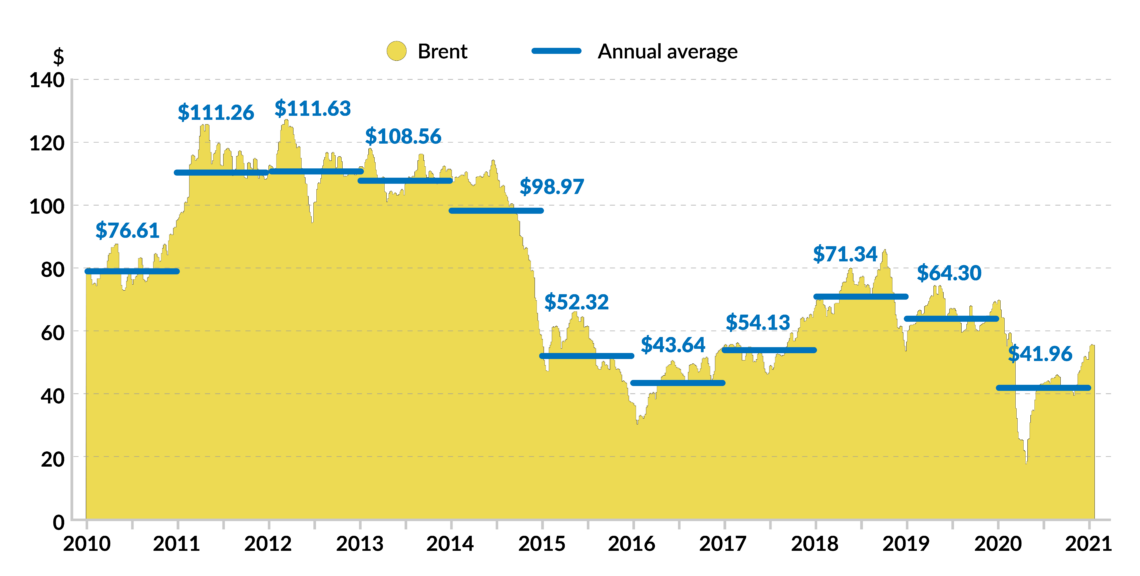

Following the blow dealt to the world by the coronavirus in 2020, one cannot help but hope that 2021 will be better. The second quarter of 2020 was particularly difficult for the global economy, especially energy markets. Oil prices went into freefall. West Texas Intermediate (WTI), a major benchmark crude, hit a historic low of minus $40 per barrel on April 20. However, oil prices have come a long way since.

OPEC+ has played a crucial role in oil markets’ recovery, agreeing upon unprecedented cuts in April 2020. The deal is expected to last for two years but the cuts are being gradually reduced. By December 2020, oil prices exceeded $50 per barrel (Brent). That recovery has been maintained since. On January 12, Brent crude oil reached nearly $57 per barrel – the highest figure since February 2020, just before the crisis hit.

It is astonishing that the average oil price for 2020 is around $42 per barrel – which is relatively high given the scale of the crisis.

Looking at oil markets in 2021, though risks abound, there are grounds for optimism. This is by no means to say that everything will be rosy indefinitely. But for the next few months, there is reason for an optimistic outlook for the oil industry as producers feel the wind blowing in their favor.

Facts & figures

Recent developments

- OPEC members Iran, Libya and Venezuela are exempt from any cuts under the April 2020 OPEC+ deal

- The International Energy Agency (IEA) expects global oil demand to recover by 5.5 mb/d to 96.6 mb/d in 2021, following an unprecedented collapse of 8.8 mb/d in 2020

- Goldman Sachs forecasts oil prices of $65 per barrel by summer 2021, instead of year-end as per their earlier forecasts

- Despite a loss of 1 mb/d of oil production in 2020, the U.S. remains the world’s largest oil producer with 11.3 mb/d (Energy Information Administration)

- In 2021, the main contributors to supply growth are expected to be the U.S., Canada, Brazil and Norway (OPEC)

Unprecedented?

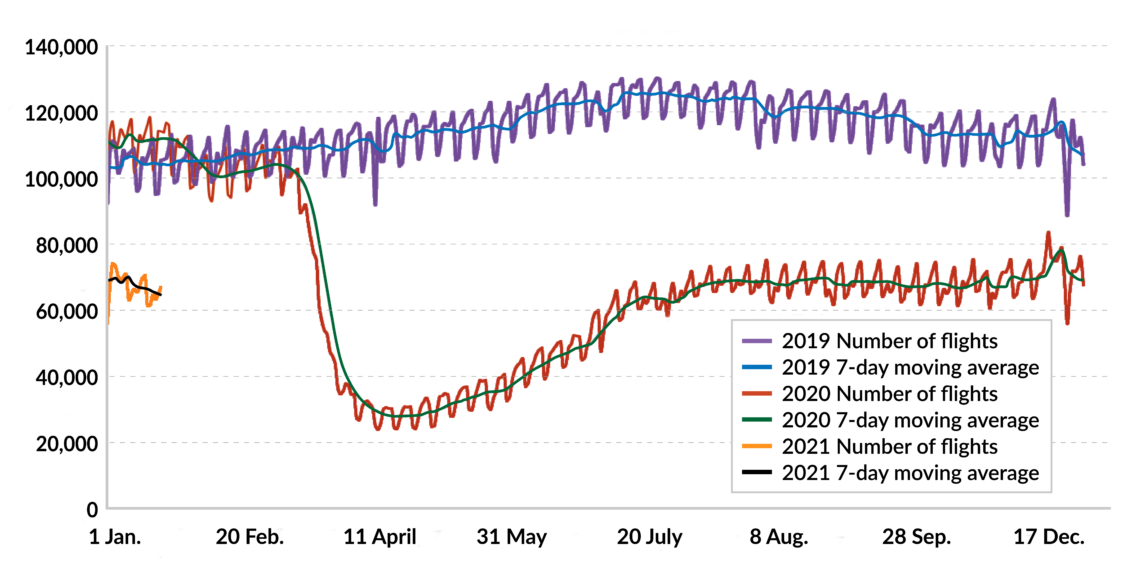

Once Covid-19 was declared a pandemic, nearly every debate or publication deemed the situation “unprecedented.” The International Monetary Fund called it “a crisis like no other.” More than 20 percent of oil demand disappeared virtually overnight. Lockdowns brought economies to a standstill, international borders were shut, and planes were grounded. The transport sector – the most important component of oil demand – was severely affected. Even today, air travel operates at less than 65 percent of 2019 levels.

In the longer perspective, however, it is astonishing to see that the average oil price for 2020 is around $42 per barrel – which is relatively high given the scale of the crisis. This price level does not significantly differ from recent years, like 2016, when oil demand was much healthier. In this respect, despite the general perception, 2020 was not such an annus horribilis.

Saudi gift

A lot of the credit goes to OPEC+, which comprises OPEC’s 13 members with Saudi Arabia being the largest producer and 9 non-OPEC producers with the largest being Russia. Its members first came together in 2016 when they agreed on a collective cut of 1.8 million barrels a day (mb/d) starting in January 2017. Back then, the deal was considered a major achievement. Fast forward to April 2020, and the producers’ group agreed on a record production cut of 9.7 mb/d – more than five times the level of 2017 cuts. This quantity has been gradually lowered; in January 2021, it amounted to 7.2 mb/d.

Facts & figures

Not surprisingly, compliance within the group has been patchy, with the usual suspects like Angola, Iraq and Nigeria not fully delivering on their promises. The United Arab Emirates also overproduced in one instance. Russia has not been a compliant member either, yet it escaped the chastising that other members faced. After all, Moscow and Riyadh are the main architects of OPEC+.

Noncompliance has been a frequent occurrence throughout OPEC’s six decades of existence. However, under the April 2020 deal, OPEC+ has pursued several strategies to improve discipline – from naming and shaming to having noncompliant members make additional cuts to make up for their overproduction. Iraq, for instance, has recently announced that it would deepen its cuts in January and February to compensate for having breached its quota last year. Given Iraq’s compliance record, however, there is reason to doubt these promises.

Riyadh has continued to subsidize noncompliant OPEC+ members.

Saudi Arabia has played, by far, the most influential role within OPEC+. Despite various statements in 2020 by Saudi Energy Minister Abdulaziz bin Salman about not tolerating cheating anymore, Riyadh has continued to subsidize noncompliant members. In 2020, it made voluntary cuts of 1 mb/d on top of its obligations set out in the April agreement. Back then, it was joined by the UAE and Kuwait, which implemented much smaller cuts of 100,000 and 80,000 barrels per day respectively – rather symbolic amounts. Then at the group’s meeting on January 5, Saudi Arabia made a surprise announcement that it was unilaterally cutting its production by 1 mb/d for the next two months. According to the Saudi Energy Minister, that decision came from Crown Prince Mohammed bin Salman, and was a “gift” to other OPEC+ members.

Clearly, Saudi Arabia is determined to shore up prices.

Economic support

Oil markets are also gaining support from beyond the industry. Around the world’s wealthier countries, the health crisis has considerably increased average savings and therefore available spending power. According to the European Central Bank, the propensity of households to save has reached unprecedented levels in 2020, partly because lockdowns curtailed spending and led to involuntary savings, and partly because of uncertainty regarding future income. In the U.S., households usually save about 7 percent of their disposable income; at the height of the first wave of the pandemic in April 2020, they saved 34 percent.

Facts & figures

This accumulation of savings is set to significantly boost consumer expenditure, with potentially large spillovers into oil markets as soon as the situation allows. Billions of people could not go on holiday this year, as they would normally do. To the extent that savings will be converted into expenditures after fears over the virus subside, one can easily foresee a boom in travel, especially air travel. This would fill in the biggest gap in global oil demand, namely jet fuels.

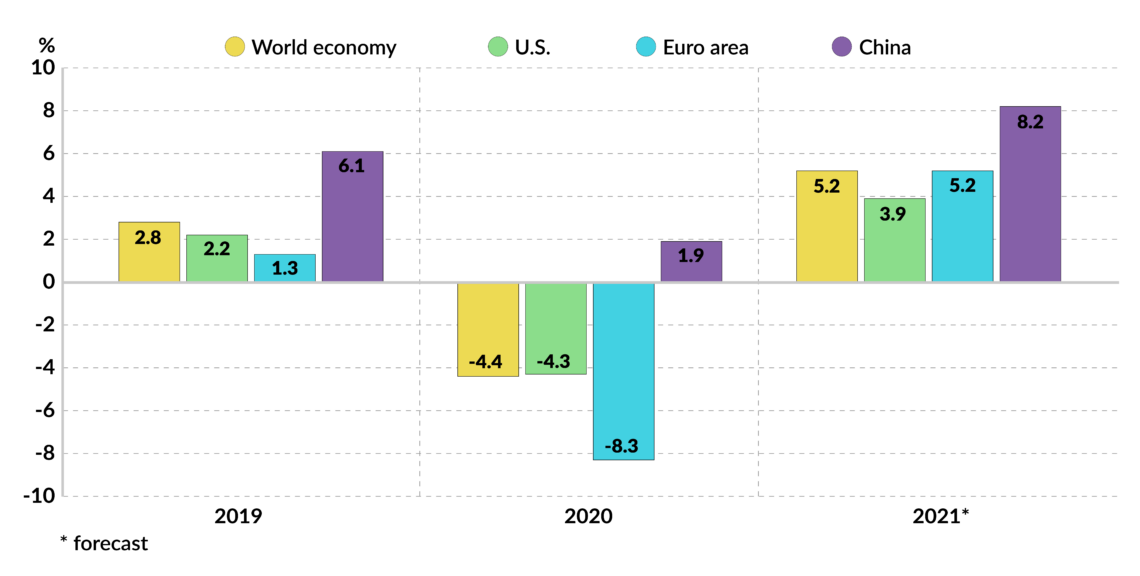

Oil markets are also getting a general boost from the improved outlook for economic recovery, with gross domestic product (GDP) growth across key oil-consuming countries also providing support for oil demand. China, the only major economy which recorded growth in 2020 and the second-largest oil consumer in the world after the U.S., could see a strong rebound in 2021. This optimistic macroeconomic outlook is not only based on the assumption of a successful vaccine rollout, but also on continued supportive monetary policies from central banks in all major economies.

Downside risks

Several risks remain and structural damage might appear in the coming few years. The list of things that can go wrong is long, including dangerous virus mutations outpacing existing vaccines as well as unforeseen issues related to vaccination itself. Such developments could easily reverse the recent gains in oil prices. OPEC+ could also become a victim of its own success. The more successful it is at shoring up prices, the faster supplies outside the group will return to the market, further limiting upside potential.

There is no shortage of potential pitfalls when looking beyond 2021.

Besides, the optimistic outlook for the oil industry itself could become a risk factor, especially when it is irrational. If the general sentiment suddenly changes because of unfavorable news, then mass reactions could negatively affect markets.

There is therefore no shortage of potential pitfalls when looking beyond 2021. But for now, oil markets can enjoy some respite.