Increasing pressure on Russia’s oil industry

Russia’s ability to finance its war on Ukraine is starting to suffer because of Western sanctions and market forces. But a determined Kremlin may not care.

In a nutshell

- The West’s strategy: cut Russian prices while keeping its supply on the market

- Asian nations buying at discounts have largely replaced Russia’s European customers

- Russia’s higher-cost oil products are exposing weaknesses

This report was written in conjunction with Roberto Ulivieri.

The West’s attempts to curtail the Kremlin’s ability to finance its war on Ukraine are starting to bear fruit. Russia’s oil and gas revenues are dropping, along with its overall economy, while its budget deficits are growing. The early results of 2023 show that a combination of price caps, import bans and lower market prices is working even as Russia’s energy exports flow.

The EU embargo on refined products of Russian origin, with associated price caps, came into force on February 5, 2023. The measures are aligned with those adopted by the Group of Seven (G7) nations and Australia. They follow sanctions on crude oil, which went into effect on December 5, 2022. Together they ban the sale within the EU of seaborne Russian crude oil and oil products, except for pipeline oil, and a temporary exemption given to Hungary, Bulgaria and Croatia because of their limited alternatives.

Any third party willing to buy such products using enabling services provided by an EU entity – such as insurance and shipping – can only do so if the price they pay for the Russian products is at or below the price cap imposed by the EU. The price cap is set at $60 per barrel for crude oil and $45 per barrel for discounted petroleum products (such as fuel oil and naphtha) and $100 per barrel for premium petroleum products (such as diesel, kerosene and gasoline).

Recently, the market has been doing a better job than the price cap, with Russian crude oil selling below the $60 per barrel cap, at least before the 1.1 million barrels per day production cut that was announced on April 2 by OPEC+ nations, including Saudi Arabia and Russia.

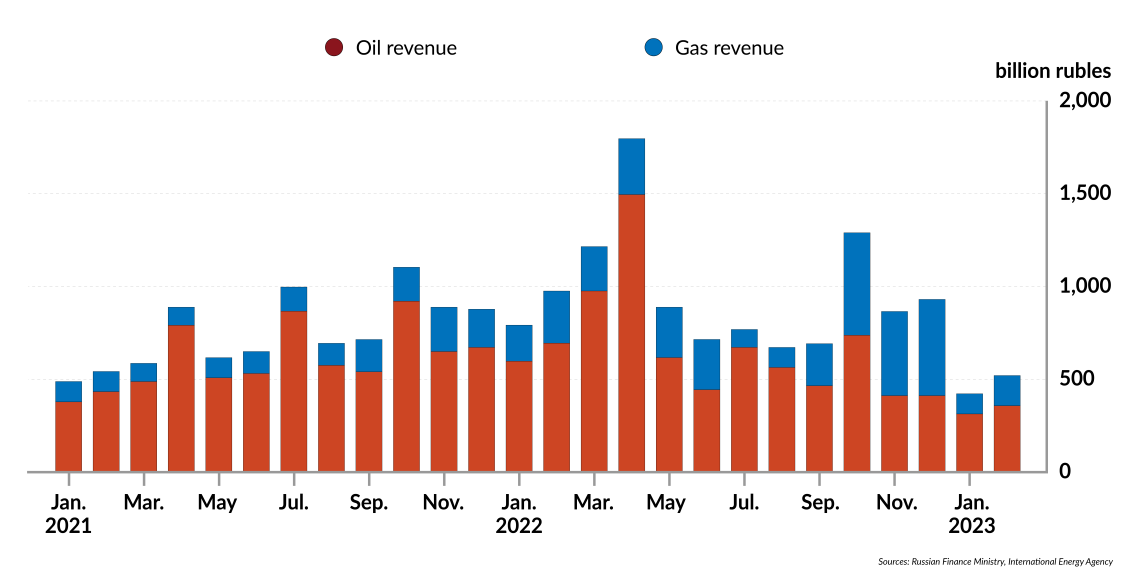

The upshot is that Russia’s revenues from oil and gas exports tumbled by nearly 40 percent in January 2023 ($18.5 billion) compared to January 2022 ($30 billion). The revenue decline will be even steeper in the coming months, the International Energy Agency (IEA) has predicted.

Targeting Russian energy makes sense because it accounts for roughly 18 percent of Russia’s gross domestic product (GDP) and at least a third of its state budget revenues. Yet despite the loss of revenue, the damage to the overall economy remains surprisingly slight, at least according to official numbers, which some question.

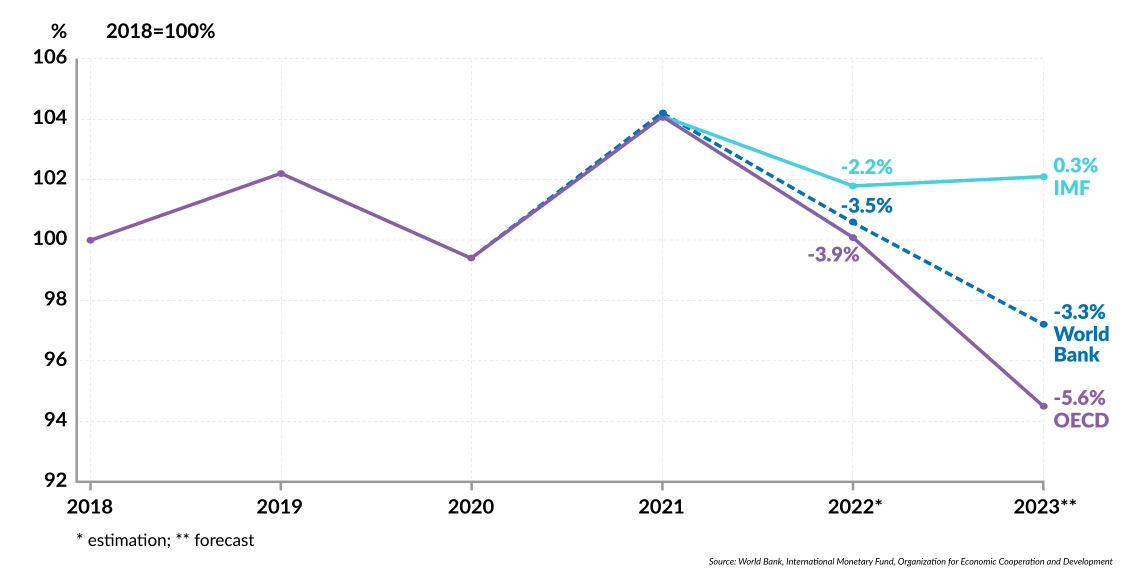

Russia’s GDP shrank to an estimated $1.5 trillion, or 2.1 percent, in 2022. The 2023 forecast ranges from no growth (+0.3 percent), according to International Monetary Fund projections, to a 5.6 percent decline, based on the estimate from the Organisation for Economic Co-operation and Development. But some critics say that the Russian government’s concealment of official data is masking deeper problems.

Facts & figures

Russia’s emptying coffers

Volume remains high

Another aim of the Western price caps, to keep Russian oil on the market, has succeeded. The volume of Russia’s crude oil production and exports has not been significantly affected, given the country’s ability to redirect its exports away from European markets to other buyers in Asia, primarily China and India. Even sold at current discounts, the oil business is still profitable for Russia. Removing the Russian supply would have put upward pressure on global prices – an undesirable scenario for the EU, which is still battling high inflation.

However, exporting oil products has not been the best way to monetize oil resources for the Russian government, which for decades has allocated part of its oil rent to subsidize highly uncompetitive refineries. Today, many Russian refineries are not viable without state support. The sanctions on the country’s oil products have made a bad situation worse. This raises the question of whether Russia will cut its supplies, particularly diesel fuel, to alleviate the financial burden on the state. In the current market conditions, a sustained loss of even half of the Russian diesel exports can be very disruptive. Should that scenario happen, it will have adverse consequences for major importers, particularly the EU, which is a very large diesel-importing region that has long depended on Russian diesel for more than half of its needs.

Also by Carole Nakhle

Russia’s energy plans derailed

The power of diesel

Among the various oil products that Russia exports, diesel stands out, not only because of the country’s export capacity and the importance of diesel to the global economy – often described as its engine and lifeblood – but also because the global diesel market has been particularly tight after recovery from the Covid-19 downturn. Supply disruptions in such a market will cause the price of diesel to rise further, which will lead to increased costs for a wide range of applications where diesel is a feedstock – from transport to heating and industrial processes.

Russia exports around 1 million barrels per day (mbd) of diesel in addition to a total of 700,000 barrels per day of petroleum naphtha and gasoline and 1 mbd of both fuel oil and vacuum gas oil. All the vacuum gas oil and part of the fuel oil are processed by refineries as an alternative to crude oil, so these products are more relevant to the crude oil supply and demand balance.

Russian diesel meets approximately 3.5 percent of global diesel needs (20 mbd). Although the figure may not seem high, it is important. History shows that the global refining industry can take in its stride year-on-year growth of diesel demand of around 500,000 barrels per day. Typically, any time demand has grown by more than this, such as through strong economic growth, market tightness has ensued. Even a partial loss of Russian supply in an already tight and recovering market would be a big ask.

Throughout 2022, Russian diesel exports continued broadly unchanged. They increased by about 200,000 barrels per day toward the end of the year, reportedly because players were trying to receive supply ahead of the sanctions.

Now that the sanctions have become effective, one would expect to see upward pressure on diesel prices, especially in light of the revival of Chinese demand. Yet the price of diesel (at Rotterdam) dropped from a January average of $125 per barrel to $110 per barrel in February ($10 above the price cap). Similarly, in January, Russian diesel was selling at $15 per barrel to $25 per barrel below European market prices; by February, the discount has reportedly increased to $30 per barrel, therefore pushing the price well below the cap.

Facts & figures

Russian economy expected to struggle in 2023

Business as usual

The price movements confirm that no disruptions to diesel supplies have happened. Instead, what has happened, just like in the crude oil market, is a redirection of trade flow: Russian diesel originally destined for EU countries is now marketed in Turkey and North Africa or forced to sail further away, for example to Latin America. In the European market, Russian diesel is being replaced with diesel coming from further away, such as the Middle East but also India and China.

Discounted Russian diesel has also created a substantial incentive for arbitrage. For example, it can be used to supply a market, like Egypt and India, at lower prices, while diesel produced by local Egyptian or Indian refineries can be sold in Europe at higher prices. Such trade movement is allowed by the sanctions and discounts of the order of $30 per barrel for a fungible commodity will compensate for a lot of storage and shipping costs. Furthermore, with more miles being sailed globally to deliver the same volume of product, the most noticeable impacts so far have been more oil at sea, higher demand for tankers and higher tanker rates. Diesel exports, however, have continued virtually unchanged volume-wise.

However, unlike crude oil, in which Russia became significantly reliant on India and China, the diesel market is a lot more fragmented and, if the heavy discounting of Russian products remains, arbitrage opportunities will stay abundant.

Facts & figures

How the Russian oil industry is holding up amid Western sanctions

- Since the invasion of Ukraine, the European Union has adopted 10 sanctions packages against Russia as of February 2023.

- In June 2022, the European Council adopted a sixth package of sanctions that, among other things, prohibits the purchase, import or transfer of seaborne crude oil and certain petroleum products from Russia to the EU.

- Since most Russian oil delivered to the EU is seaborne, the sanctions covered nearly 90 percent of Russian oil imports to Europe by the end of 2022.

- In 2022, Russian oil output rose by 2% to 10.7 million barrels per day while exports increased by 7.5%.

- The price differential between diesel and crude, also called crack spread, has been very wide in global markets, whereas gasoline cracks have been much weaker in comparison, an indication of a tight diesel market globally.

Russian refineries

What has been less talked about is the state of Russian refineries. For years, they have supplied Europe from a position of a competitive disadvantage because they are located deep inland and therefore have a logistics penalty. In a free and undistorted market, a Russian refinery selling into the European market would earn $5-10 per barrel less because of the higher costs of delivery. To keep them in business, the Russian government created a system whereby export taxes, primarily on crude oil, subsidize those refineries. Without any subsidies, 80 percent of Russian refining capacity would halt operations immediately.

Being indexed to crude prices, the subsidy has historically increased and decreased in tandem with movements in the price of Russian crude oil. The recent price collapse has reduced export taxes and subsequently subsidies to refineries to very low levels, thereby threatening the continuation of their operations, with consequences for global diesel markets and consumers.

However, with its revenues squeezed and financial capacity weakened, there may be an economic rationale for the Russian government to support such an outcome. If that happens, Russia would have more crude oil (an additional 1 to 1.5 mbd) to export – since less production would be refined domestically. But that would depress crude prices unless there is enough demand in global markets to absorb the additional oil. The IEA expects oil demand to increase by 1.3 mbd this year.

The alternative for Russia would be to reduce its crude oil production. Earlier this year, the Russian government announced it would cut crude oil exports by 500,000 barrels per day as of March. The primary reason is to sustain prices, but it could also be an indication of other difficulties. However, the deeper the cut, the bigger the loss to the country’s share in the global market. It may be difficult to regain the share – after all, shutting down oil fields from the Soviet era is much simpler than bringing them back on stream.

Scenarios

It may be easier for the Russian government to keep subsidizing refineries and keep the diesel flowing into the global market. This will improve access to markets and safeguard market share. While the severe consequences that the EU has hoped for may have not materialized, the pressure is clearly mounting on Russia’s oil industry.

Sign up for our newsletter

Receive insights from our experts every week in your inbox.