The promises and risks of the EU’s single safe asset project

The launch of a Sovereign Bond-Backed Security (SBBS) is advocated by EU leaders as the best way to overcome the flaws inherent in the monetary union. The SBBS is supposed to offer investors new reliable stores of value and, as such, a miracle cure for chronic instability in European bond markets.

In a nutshell

- The EU’s single safe asset project is advertised as a way to palliate the shortage of safe financial assets in the euro area

- The Sovereign Bond-Backed Security would be an alternative to debt issued by countries with low default risks

- Securitizing sovereign debt is a trick for circumventing the problem of risks mutualization among EU member states

The release of a new financial product rarely makes headlines. The Sovereign Bond-Backed Security (SBBS), however, is one that did. More precisely, it was the European Commission’s proposal of May 2018 for a regulation that could enable the “market-led” development of such securities that made a splash.

From the start, SBBS was announced as a miracle solution for eliminating chronic instability in European bond markets. It is argued in EU policy circles that what the euro area most desperately needs, after a decade of financial stress, is “safe assets” – that is, financial products that can be used as reliable stores of value. And the SBBS is supposed to be exactly that: a promise to deliver lower credit risk and higher liquidity than most national government bonds available in the euro area can offer.

Breaking the German monopoly

The abundantly advertised new debt instrument is said to palliate the tremendous shortage of safe financial assets in the euro area, deemed responsible for persistent financial instability in the aftermath of the crisis. The SBBS is also supposed to reduce the destabilizing cross-border flights of investors into safe bonds that occur in times of uncertainty – in particular, the German Bunds, which are the benchmark for safety in the present-day eurozone.

Today, as a whole, the euro area does not have a safe asset of its own, i.e., one that guarantees a payoff even in the face of severe adversity. European financial markets operate exclusively with national bonds as safe assets denominated in euros. At present, only Luxembourg, the Netherlands and Germany supply AAA-rated sovereign debt to eurozone financial markets – of which the latter alone issues more than 80 percent. A euro-wide Single Safe Asset would relieve EU officials from this awkward situation. (Could this be the unspoken reason why this concept has the wind in its sails?)

Before being picked up by EU technocrats, the idea of “creating” safe assets was debated in academic circles.

The launching of a Single Safe Asset is generally advocated as a way to overcome a series of flaws inherent to the Economic and Monetary Union (EMU), which became obvious notably after the euro debt crisis at the end of 2009. The success of the SBBS, therefore, appears crucial to its defenders. The future deployment of Europe’s Banking and Capital Markets Unions is said to be at stake.

Supranational engineering

Before being picked up by EU technocrats, the idea of “creating” safe assets was debated in academic circles, principally after the euro crisis. In 2016, a first working paper addressed the matter, asserting that spillovers across sovereign bond markets that were affected by localized shocks could be reduced significantly by the introduction of so-called “European Safe Bonds” (ESBies). Two years later, a group of 14 high-profile economists also defended the idea that a Union-wide “synthetic” safe asset would offer European investors a credible alternative to national sovereign bonds.

Political discussion on safe assets in the European context truly began in 2018, after the European Systemic Risk Board (ESRB, a body hosted and supported by the European Central Bank, or ECB) had commissioned an independent high-level task force, directed by former governor of the Central Bank of Ireland and present ECB chief economist Philip Lane, to investigate into the technicalities related to the creation of a common safe asset for the euro area.

After a wide-ranging feasibility study, the team came up with a concrete plan for bundling up member states’ sovereign debts into a security that should be capable of withstanding default by one or several governments without sparking euro-wide propagation.

The idea fell on fertile ground. The European Commission actually anticipated it in its 2017 White Paper on the future of Europe, and the European Parliament adopted a first version of the project in April 2019. In the latter’s resolution, the systemic risk board, is formally designated as the competent macro-prudential oversight body of the EU’s future SBBS market.

Safety in tranches

SBBSs differ from ordinary “safe assets” (debt issued by countries with low default risks) insofar as they entail a “securitization” process.

Their creation would, as a first step, involve an entity – the “arranger,” that puts together a diversified portfolio of euro-denominated government bonds. This arranger could be a private or public institution: a bank or insurance company, a hedge fund, a government or the European Stability Mechanism (ESM).

The arranger would then sell the portfolio to a private-sector entity – the “issuer,” who would issue a series of claims. The idea is to use a pool of sovereign bonds as collateral for a security delivered in “tranches,” which are ranked according to “seniority.”

Basically, there is a “senior” tranche and a “junior” tranche. While the first is low-risk (expected to be “at least” as safe as Bunds), the second is high-risk (like Italian or Greek debt, for instance). Ideally, SBBSs should contain a 70 percent risk-free (senior) and a 30 percent risky (junior) tranche. That means that losses arising from sovereign default would first affect the holders of the junior claim. Thirty percent is estimated to be a large enough buffer to absorb potential losses on the portfolio’s underlying sovereign bonds.

At the start, joint liability had been considered as a foundational value for the European Union.

The different parts of the SBBS’s liability structure should attract different investor profiles. The junior tranche is for high-yield seekers. Risk-averse investors, whose objective is the preservation of the value of their capital, would go for the lower-yield but safer senior. Preferably, for the sake of financial stability, banks should be those to invest in the safest tranche, leaving the riskier purchases to other stakeholders, the ESRB maintains.

Joint-liability fallacy

Securitizing sovereign debt is a trick for circumventing the thorny problem of the mutualization of risks among EMU member states. At the start, joint liability had been considered as a foundational value for the union. With the crisis, however, inter-government solidarity rapidly became controversial. In particular, the Germans made clear they are no longer willing to pay for others that entangled themselves in (self-inflicted?) debt-traps.

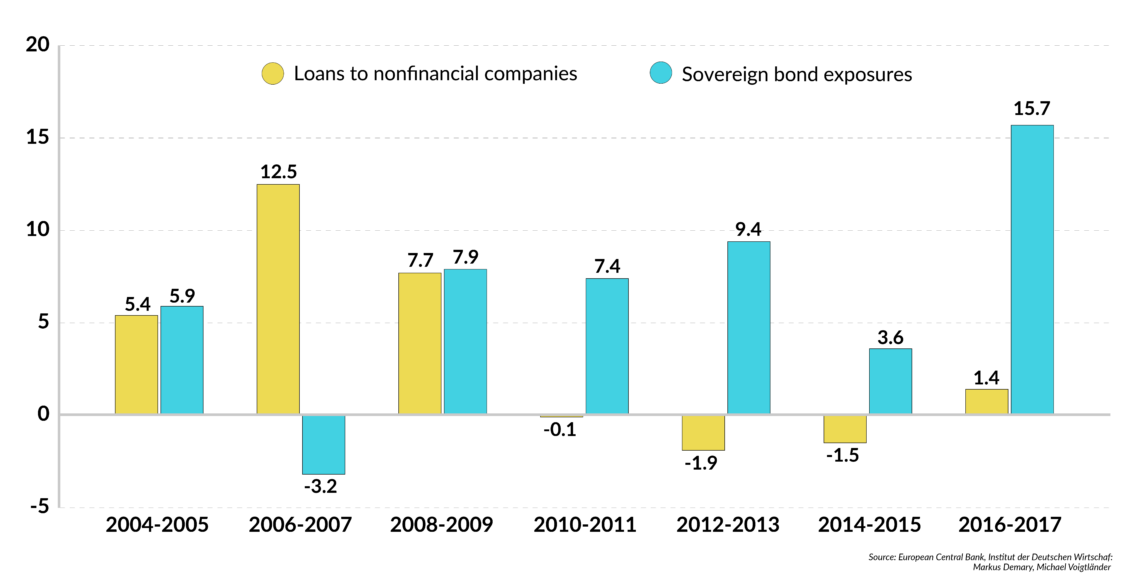

Facts & figures

Bank are incentivized to lend to governments

Average year-on-year changes in the notional stocks of loans and sovereign bonds, in percent, eurozone

In this sense, SBBS contrasts with earlier endeavors to create a single safe asset. For instance, the so-called “Eurobonds” or “stability bonds,” proposed by the Commission in 2011 as a way to cope with the European debt crisis, implied that the 19 member states of the union were jointly responsible for each other’s debt. The project did not move forward, given the Germans’ refusal to be part of it.

As mentioned before, SBBSs are created through private contracts. Hence, they merely involve risk-sharing by investors (i.e., on the liability side). Each government should remain individually responsible for meeting its debt obligations.

Spreading debt risk

The foremost ambition of the safe asset project is to break the “home bias” in banks’ sovereign exposures, which had been at the heart of the European debt crisis. If banks accepted to load up on SBBSs instead of debt issued by their home government, they could break the fatal linkage (or doom-loop) between their solvency and that of the nation-state in which they reside.

Indeed, SBBSs only incorporate exposures to a small part of sovereign risks of each member state. Avoid putting all eggs into one basket – that seems to be the piece of advice underlying the Commission’s proposal to “aggregate” debt from weak and strong countries into “packages of debt securities.” (On this point, a Netherlands-based Institute notes a certain parallel with the subprime mortgage junk bonds in the U.S.)

Also, since a myriad of investors would bear risks, none of which are supposed to have a systemic impact, the danger of system-wide contagion that could otherwise result from banks’ excessive exposure to high-risk sovereigns would be attenuated if SBBSs achieved a breakthrough.

Regulatory impediments

SBBSs are increasingly promoted as the cornerstone of stable eurozone financial systems in the future. There is a problem, however, that is likely to hinder the emergence of their market. To the ESRB’s regret, financial regulation treats these instruments as “securities” and, therefore, inflicts securitization-specific surcharges on them.

Not only do these need to be dropped, insists the EU Commission, but to succeed, SBBSs must benefit from “preferential” regulatory treatment. This is what the “enabling” regulation for the creation of SBBSs – recently endorsed by EU Parliament and pending approval by the EU Council – hopes to achieve.

Banks’ preference for sovereign debt has been fostered for years by international banking regulations.

Barriers are not all out of the way, in any case. Right now, there is no reason for investors to prefer the sovereign -debt-backed security to ordinary sovereign bonds. On the contrary, experts tend to predict that financial markets will not react enthusiastically to the entrance of SBBSs and that some national sovereign (most likely German) bonds will probably remain the preferred asset in our uncertain times.

Thus, for months, interinstitutional negotiations keep dragging on. Last July, Eurogroup President Mario Centeno reportedly set up working groups to explore ways to end the current impasse as soon as possible.

Nonstarter?

Banks’ preference for sovereign debt has been fostered for years by international banking regulations (based on the Basel standards), which classify OECD public debt as zero-risk. Hence, for the purchase of public bonds, no capital increases are imposed on banks, no matter the fiscal soundness of the sovereign issuing the bonds. In times of crisis, where capital is scarce and costly, banks, therefore, prefer accumulating government bonds instead of other assets associated with higher risk weights in the regulatory framework.

Today, banks in the euro area altogether hold 1.9 trillion euros in sovereign bonds, many of which are high-risk. That means some would not have loss-absorbing buffers big enough to face sovereign default. And this is how the “doom-loop” comes about: a sovereign in difficulty can bring down part of the banking sector, which in turn can bring down a government.

In this line of thought, the German banking authorities, as well as some top EU executives, urge regulators to drop the assumption that euro area government debt bears no risk.

Banks should constitute a cushion for holding risky sovereign bonds. The requirement would deter them from piling up debt from broken governments. Hence, the systemic risk could be contained by merely abandoning the preferential regulatory treatment of euro area sovereign debt. This appears to be a sensible policy for breaking the “diabolic loop” between sovereigns and banks.

Encouraging the creation of diversified funds of eurozone government bonds is another policy option proposed by economist Daniel Gros from the Brussels-based think tank CEPS. He maintains that the euro area needs a “diversified” rather than a “safe” asset. But there again, the problem is that the current regulation hinders diversification.

Finally, is there truly a need for a single safe asset in the euro area?

Safety fiction

Critics argue that the SBBS is merely a technocratic response to chronically unstable financial markets. The project is not unanimously endorsed. Some economists (Paul De Grauwe and Yuemei Ji, also from the CEPS research center) assert that financial engineering cannot succeed in creating stability in an inherently unstable environment.

In normal times, the SBBS can be used as collateral (in repo or derivatives transactions), thereby efficiently providing markets with liquidity. It is also undeniable that, as argued before, securitizing public debt helps considerably de-risk bank balance sheets.

It is hard to say, however, whether the senior SBBS can maintain its safety status during a severe global crisis. As the CEPS authors point out, panicking investors could put into doubt the safety of both the junior and the senior tranches, and trade them for sovereign bonds they still consider safe. In the end, it does not seem to matter how safe assets actually are, but how they are perceived.

In such a scenario, liquidity would quickly decrease and, once again, the entire financial sector could be at risk.

With ECB intervention foresworn, announcing that the central bank stands ready to provide the European sovereign bond market with liquidity (something that ECB President Mario Draghi did in 2012) could make financial instability systemic. The highest risk of the SBBS project is that it creates an illusion of safety.

Without a commitment to joint liability by EMU member states (and, right now, there is no political readiness to go in that direction – rather the opposite), it will be hard to imagine a common euro area sovereign bond market.