The Suez Canal privatization conundrum

Faced with unsustainable debt levels, Egypt is taking steps to privatize the highly profitable Suez Canal.

In a nutshell

- Egypt is under growing economic strain

- Cairo is attempting to privatize key assets

- The privatization of the Suez Canal could backfire

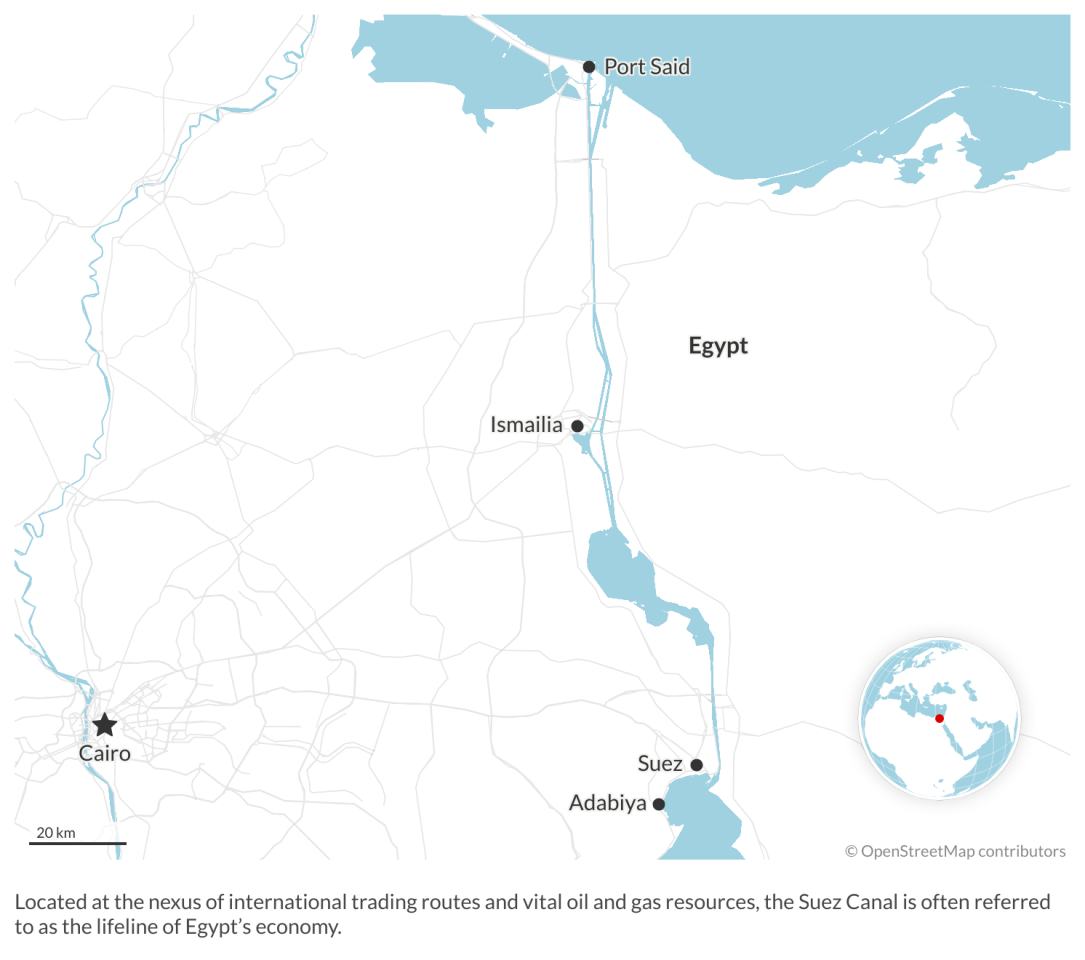

The Suez Canal is the crown jewel of the Egyptian economy, bringing in a steady stream of income that has withstood wars, pandemics and financial crises. Some 10 to 12 percent of world trade and 10 percent of global oil and gas shipments pass through the 193.3-kilometer channel, generating daily revenues of $21.7 million. If the authorities in Cairo were to shut it down, the disruption to supply chains would trigger a massive inflationary surge.

Given the strategic importance of the waterway, the creation of a fund allowing the sale of Suez Canal assets was met with a frosty reception from the Egyptian public and business sector. Selling some port facilities to private or foreign investors would take the country into the uncertain waters of free market economics. Egyptian President Abdel-Fattah El-Sisi is aware of this, but he has no other solution. At a recent summit in Dubai, he declared: “Egypt needs a trillion dollars per year. Do we have the money? No. Do we have half? No. Do we have a quarter? No.”

The Suez Canal’s profitability is not under debate. In fact, after carving out a new river section for supertanker transit, profits surged 25 percent, reaching $7.9 billion last year. This upward trajectory has continued throughout the first months of 2023, with a robust 35 percent rise in the first quarter. These revenues suffice for maintaining the canal and managing navigational hazards, such as the infamous grounding of the Ever Given container ship in 2021, which blocked the canal for six days.

Development work on the canal is almost nonstop. The latest project to widen the waterway by an additional 10 kilometers of bidirectional traffic (between terminals 122 and 132) is nearing completion. It will allow an additional six vessels to pass through every day. More ships mean more revenue. On March 13 this year, Cairo celebrated a record number of vessels passing through in one day: 107.

Business and sovereignty

There is a widespread fear that the Suez Canal could become the target of rushed deals. If the state gradually sells off shareholdings to refill its coffers, Cairo could eventually lose control over this highly profitable entity. The unease is amplified by President El-Sisi’s decision to open equity in 32 companies to minority shareholders, aiming to draw in $40 billion in investments over the next four years.

Strictly speaking, the buyers are not from the business world. They are sovereign wealth funds, subject to diplomatic goodwill from the Arab world. Abu Dhabi’s sovereign wealth fund will invest $2 billion in fertilizer and logistics companies, as well as in the Commercial International Bank, one of the country’s main banking institutions. The Saudi Public Investment Fund has positioned itself to take stakes in the energy sector, including in the petrochemical company MOPCO, for $266 million. The Gulf monarchies have understood the gravity of the Egyptian economic situation, which has become so dire that the government is now advising the poorest to survive on chicken feet.

From centralism to free market

The Suez Canal’s excellent financial health is not representative of Egypt’s overall business climate. The Egyptian central bank devalued the currency by 20 percent to offset the knock-on effects of the Ukrainian crisis and to curb runaway inflation, which reached 33.9 percent during Ramadan. President El-Sisi knows that to avoid state bankruptcy, he must undertake the long overdue privatization of the economy to generate jobs and wealth.

The concern is that investors might primarily be attracted to the country’s standout businesses, such as Wataniya Petroleum, with its network of 250 gas stations; Safi, a mineral water bottling company; and of course, the Suez Canal. These represent the safest and most lucrative investments with clear potential for growth.

More by Pierre Boussel

Tunisia’s democratic decline

New hope for an end to Yemen’s civil war?

These thresholds of profitability and transparency are not common for most Egyptian companies that have been asked to open up to private partners. Some business leaders have lived away from prying eyes for decades. They are not used to opening their books and formalizing their business model in writing. Even determining the purchase value of their business is a challenge. In addition to the potential for inflated valuation, there are inherent limitations associated with minority ownership. For instance, minority shareholders typically lack direct access to a company’s top executives, making it more difficult to ensure good governance.

It has long been an unspoken tradition for the state to reward senior officers with prestigious positions in large companies when they retire. The current chairman of the Suez Canal Authority, Osama Rabie, is an admiral and the former commander of the Egyptian Navy. Though Mr. Rabie is a widely accepted and respected leader in his role, there are instances in other organizations where individuals have been assigned roles for which they lack proven competence. The negative impact of such placements on the efficiency and performance of these organizations is readily apparent.

President El-Sisi’s drive toward privatization is risky because it threatens the vested interests of the Egyptian army, which has evolved into a political force over the years. The military has proven its capabilities in managing megaprojects, such as the $45 billion construction of the yet-unnamed new administrative capital – a towering skyline sprouting from the desert. However, the same army can also be a source of resistance and obfuscation. The connections between the formal and informal economies are plentiful and often hard to trace.

For years, the World Bank, the IMF, the United States and the European Union have been urging Egypt to abandon the structures inherited from the Nasser era in favor of a new economic model that is more dynamic, more transparent and better suited to Egypt’s immediate challenges. The privatization of the Suez Canal is both vital and precarious, given the current economic climate in Egypt. Debt alone accounts for 54 percent of public expenditures and domestic consumption is on a downward trend. Cairo is racing against the clock to implement necessary changes.

Scenarios

Silk Road expansion via the Suez Canal

The Suez Canal is attracting investors. On the heels of Xinxing Ductile Iron Pipes, which will invest $2 billion in steel plants in the Canal Economic Zone, Beijing could use the Suez Canal Authority Fund to consolidate its Silk Road initiative and seize the opportunity to invest in the Egyptian domestic consumer market that will emerge sooner or later.

Social tensions amid expansion of the Suez Canal

The development of the Suez Canal could cause tensions. Hundreds of Egyptians are being displaced from the town of Arish, where a new port is soon to be built. Anger could spread. The deteriorating social climate would halt Egypt’s ambitious megaprojects. The economy would only be partially privatized, without any significant improvement in the living standards of the Egyptian people. Popular mobilization could lead to unrest and spark demonstrations that would have to be brutally suppressed. The chasm between Egypt’s highly profitable entities and the rest of the failing economy would widen.

Sign up for our newsletter

Receive insights from our experts every week in your inbox.