Post-election Turkey returns to economic orthodoxy

President Recep Tayyip Erdogan is eyeing economic revival by turning the country back toward conventional policies and partnership with the West.

In a nutshell

- Reelected President Erdogan seeks to lower inflation, restore investor trust

- He will likely realign closer to the West in both economic and foreign policies

- It is unclear what he hopes to achieve with a new Turkish constitution

Turkish President Recep Tayyip Erdogan, reelected in May 2023 to a third five-year term, has decided to adopt more conventional economic policies to reduce inflation and right the suffering economy in the Middle Eastern nation of 85 million people. He has the political capital to sustain the shakeup. Not only did Mr. Erdogan win with 52 percent of the vote, but the People’s Alliance – a coalition led by his Justice and Development Party (AKP) – also won a parliamentary majority.

First, as part of the overhaul, the president appointed a new economics team that includes Cevdet Yilmaz as vice president, Hafize Gaye Erkan as central bank governor and Mehmet Simsek as treasury and finance minister. Ms. Erkan, however, recently resigned and Fatih Karahan, the new appointee, is expected to continue with the same policies.

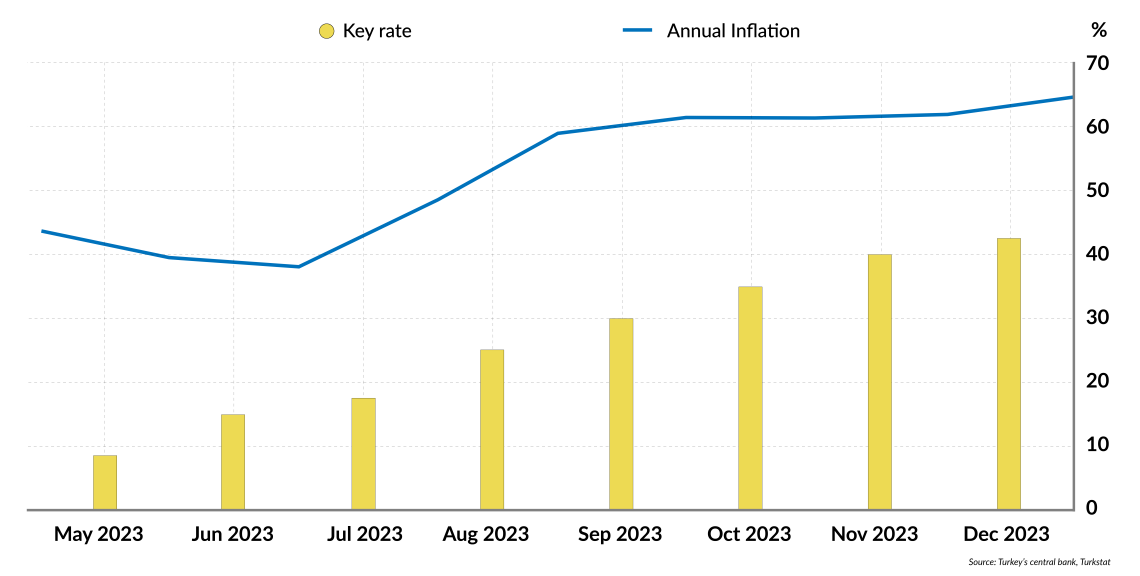

The new team has a difficult task in restoring investor and consumer confidence. Inflation in the nation is expected to average 66 percent throughout 2024, according to a September forecast by the Economic Policy Research Institute of Turkey (TEPAV). That is one of the highest rates in the world, fueled by unconventional preelection central bank policies of low interest rates. The government’s target inflation rate is 36 percent by year’s end. Mr. Simsek – who is popular among foreign investors – and the rest of the economic team quickly adopted orthodox economic policies.

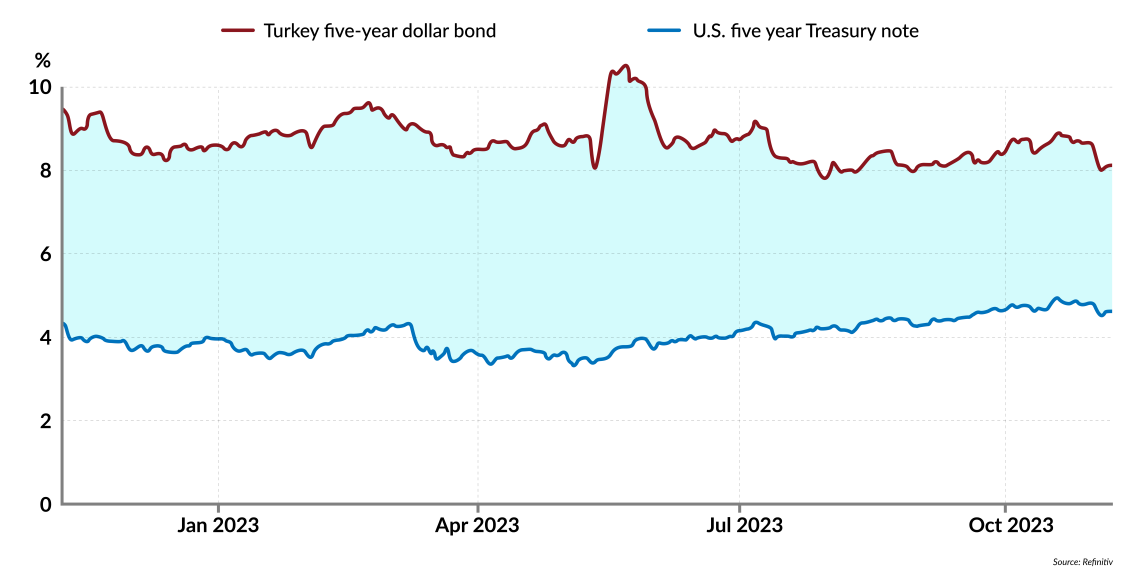

Turkey returned to the dollar bond market in November 2023 to finance debt, securing $2.5 billion in the first deal. Since the May 2023 elections, the Turkish central bank has hiked interest rates from 8.5 percent to 45 percent. The results have not slowed inflation yet, but expectations are that they will work eventually: In mid-January, Moody’s Investors Service upgraded the country’s outlook to positive from stable, citing a “decisive change” in economic policy. Some experts expect inflation to moderate despite a recent 49 percent hike in the minimum wage.

Second, President Erdogan has reiterated that joining the European Union is Turkey’s strategic priority, a declaration greeted with incredulity by its European partners. Yet it has become the new motto in Ankara simply because the return to rational economic policies will require an accompanying return by Turkey to the West in its foreign policy orientation.

Third, President Erdogan has started talking about the need for a new civilian, democratic constitution based on domestic consensus, a switch from the normally contentious Turkish politics.

Facts & figures

Turkey’s interest rate hikes have yet to cool inflation

How the era of irrational economics began and why it ended

It all started after the Islamic State siege of Kobane in northern Syria in 2015, in which 120 civilians were killed. Until the Kobane massacre, Turkey was part and parcel of an alliance that included the United States against Syrian President Bashar al-Assad. After Kobane, Turkey’s allies broke from Ankara and established a new headquarters in Syria with the YPG, Kurdish fighters aligned with the U.S. Turkey considers the YPG to be terrorists, indistinguishable from the Kurdish PKK, which the West officially labels as a terrorist organization.

The rupture turned Turkey into a foreign policy spoiler from the West’s perspective, not just in Syria, but also throughout the Eastern Mediterranean. The establishment in 2019 of the East Mediterranean Gas Forum, a multinational grouping that excluded Turkey, made matters worse.

A salient feature of the Turkish economy is a savings deficit that requires Turkey to rely on U.S. dollar markets to finance its current account deficits. But former U.S. President Donald Trump’s threat to destroy Turkey’s economy, if it took unspecified “off-limits’’ actions in Syria, fueled Ankara’s fears, prompting the country to cut its ties with dollar markets. That step required eliminating credit-swap lines with London and bringing Turkish gold back home.

The era of irrational economic policies had begun and extended to the foreign policy realm, given the developments in Syria. The circumstances prompted NATO member Turkey to fall out of step with the West and go its own way.

As legitimate as the grievances may have been, it led to harmful government economic policies that Turkey is still trying to undo today. A nation in chronic need of financing cannot decouple from U.S. dollar markets. Russia, China or the Gulf states are no substitute for orderly Western markets.

Facts & figures

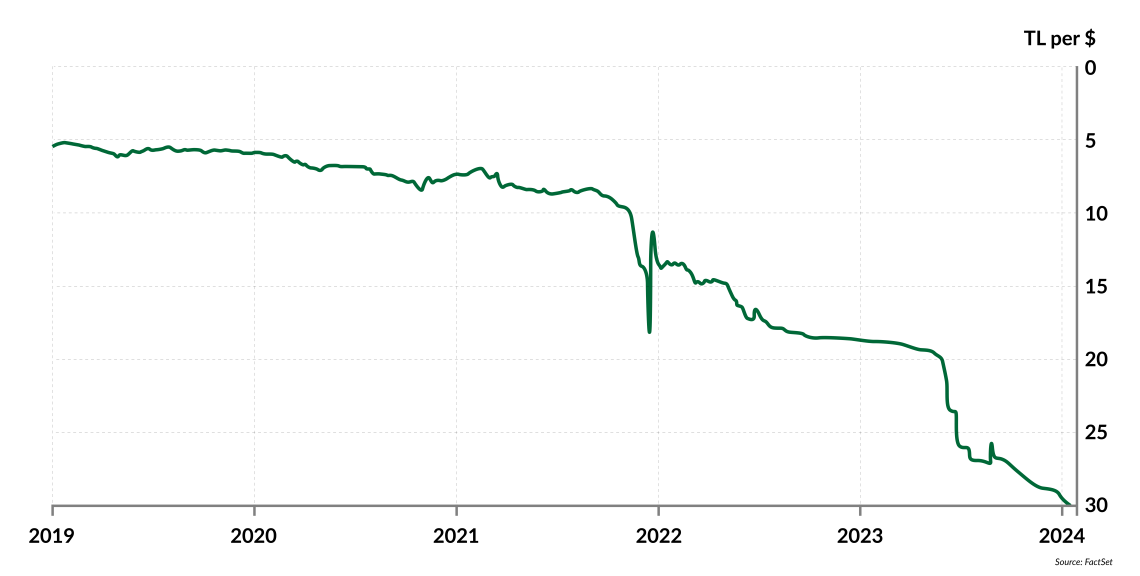

Turkish lira tumbles

Turkey knows better

Turkey was one of the first developing countries to design and implement financial liberalization measures in the 1980s, when the nature of fund flows between countries started to change. The transfer of funds had previously been government-to-government before the 1980s but then shifted to market-based transactions. Recognizing the sea change, Turkey was one of the first to establish and liberalize its financial markets among developing countries. That meant it had not only developed orderly government debt instruments and a stock market but also opened its financial markets to foreign participation and allowed for the convertibility of the Turkish lira.

The harm from the unorthodox economic policies in recent years became visible even before the May 2023 elections. Coupled with election dynamics, the country saw a rapid rise in inflation and a swift deterioration in both the current account and budget deficits. Today’s policy turn is simply one of necessity to stabilize the Turkish economy.

Turkey’s robust economic potential

Turkey is an industrialized country with a diversified manufacturing base and a nominal gross domestic product that topped $1.1 trillion in 2023, ranking 17th among nations. Its economic transformation is mostly due to close relations with the EU. About 95 percent of Turkish exports are manufacturing products and around 53 percent of them go to G7 countries. Close cooperation with the West has turned the sleepy agrarian country of the 1960s into a dynamic industrialized country in the 2020s.

A balance of payments crisis in an industry-based economy is more detrimental than a balance of payments crisis in a resource-based economy, like Argentina. In Turkey’s case, the country’s earning capacity requires it to have hard currency at the beginning of the production cycle, so it can pay for imports. The failure to procure imports or repay debts can lead to massive unemployment and rampant inflation in a country such as Turkey.

However, untangling a web of irrational policy measures requires care. Hard currency demands could skyrocket overnight, given the weakened state of the lira, which is trading at record lows against the dollar. Gradualism would deliver fewer shocks, but fuel the risk that impatience grows among the people and the political elite as new municipal elections approach in March 2024.

Facts & figures

Scenarios

More likely: Erdogan sticks to economic orthodoxy, EU, new constitution

Turkey has municipal elections coming up in March 2024. President Erdogan’s AKP lost the 2019 municipal elections, most notably in big cities like Istanbul, Ankara and Antalya. If their objective is to start a rapid economic recovery in the lead-up to March balloting, especially in urban areas, then the administration is running out of time for the new, gradual economic policy framework. If these steps create a sense of positive economic expectations, such as lower inflation, they may work.

Keeping the EU as Turkey’s strategic priority could also boost positive economic expectations. The sooner that Western partners start engaging with Turkey, the higher the expectations will become.

As for a new constitution, it could be part of President Erdogan’s attempt to find new coalition partners in a parliament that will remain until the next presidential election in 2028. Implementing policy shifts made since the 2023 election may require new allies in an expanded coalition in parliament. A debate over a new civilian constitution may quickly bring new partners together, probably right after the local elections.

Less likely: Erdogan tries to stay in office past 2028

The debate over a new constitution might also be a way for Mr. Erdogan to extend his presidency. The president’s final constitutional term ends after the 2028 elections, so perhaps he will seek a new term with a new constitution. Such a power grab would, however, unite the otherwise disparate opposition. If it were up to voters in metropolitan areas, Mr. Erdogan would not be Turkey’s president today. Thus, he probably will not risk manufacturing ways to hold on to power.

For industry-specific scenarios and bespoke geopolitical intelligence, contact us and we will provide you with more information about our advisory services.

Sign up for our newsletter

Receive insights from our experts every week in your inbox.