The disruptive power of American tight oil

The shale revolution in the U.S. has transformed the domestic oil industry and global oil markets. Tight oil has both increased supplies and shortened the reaction time of production to prices, with the U.S. industry proving resilient. The new competition has reduced the leverage of other producers and shrunk the geopolitical risk in oil markets.

In a nutshell

- Tight oil has increased global supplies and competition

- U.S. supplies should maintain growth in the medium term

- The influence of OPEC and other producers is shrinking

- A new normal of low short-term volatility may be here

It is hard to overstate the role that the “shale revolution” has played in the recent transformation of the United States oil industry and the global market.

Today’s oil markets are very different from only a decade ago. U.S. tight oil has fundamentally altered oil supplies, not only in terms of additional quantity but because the reaction time of tight oil production to prices has shrunk to months instead of years, as is the case with conventional oil.

Such a simple yet powerful feature has created new competition to traditional suppliers and subdued the effect of what once used to be cause for major alarm: geopolitical risk.

A remarkable transformation

The technologies that allow the extraction of oil and gas from previously uncommercial source rock may be among the most important technical innovations in the history of the oil and gas industry. The revolution began only a decade ago, when shale drilling technologies came to natural gas and then spread to oil.

A combination of horizontal drilling and hydraulic fracturing (also known as fracking) techniques allowed oil and gas to be extracted in shale rock formations with low permeability. In this process, fluids are injected under high pressure to break up these geological formations and release trapped fuels.

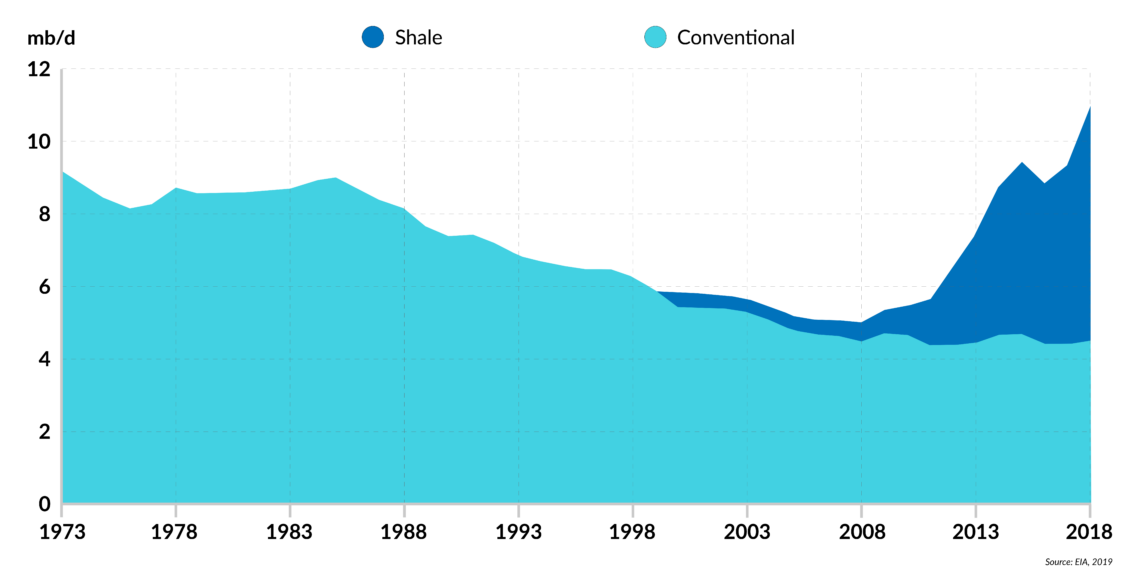

The impact of the shale technology on the U.S. oil industry has been nothing short of astounding. Long thought to be in terminal decline, in line with predictions of “peak oil,” U.S. oil production started to grow again. In 2017 it exceeded the previous production peak of 9.6 million barrels per day (mb/d), reached in 1970. At that time, U.S. oil production proceeded to shrink steadily for four decades and American dependence on foreign oil increased accordingly. The decline was only broken in 2009 when tight oil began to reach the market in large quantities.

Facts & figures

U.S. crude oil production

The Energy Information Administration (EIA) expects U.S. oil production to reach 13.5 mb/d by the end of 2020. For the first time since the early 1940s, the U.S. is expected to become a net oil exporter by the end of 2019 or early 2020 – a remarkable transformation.

Resilience

When oil prices plummeted in 2014 due to the new wave of U.S. oil production, skeptics (including senior OPEC decision makers) predicted the end of the “shale revolution,” believing that shale development would not be viable at low price levels. Indeed, by mid-2016, more than one hundred small, independent shale producers had filed for bankruptcy, while the number of active oil rigs had fallen from the peak of 1,609 in October 2014 to 316 in May 2016.

However, the industry proved to be more resilient than its critics anticipated. While undercapitalized producers had to exit the business, their assets were picked up by better operators and both cost efficiency and productivity improved significantly. As a result, the shale industry emerged from the crisis in better shape than ever.

U.S. oil production is expected to maintain its robust growth in the medium term in the current price environment. According to the latest Dallas Fed Energy Survey, U.S. exploration and production companies can, on average, profitably drill a new well when West Texas Intermediate (WTI) ranges from $48-54 per barrel. Logistical constraints due to a lack of sufficient pipeline capacity have negatively affected some shale areas, but that should be resolved by the end of 2019.

Impact on the market

Shale technology has not only revolutionized the U.S. oil industry but has fundamentally reconfigured global oil markets. By tapping into a vast and previously uneconomic resource, the U.S. industry added a major new source of oil supplies to the global market and one with a much shorter development cycle than conventional oil.

Long thought to be in terminal decline, U.S. oil production started to grow again.

A conventional oil project may take seven to 10 years to convert investment into production. But for tight oil projects this lag has shrunk to a few months, making production very price sensitive and limiting the influence over the market of traditional swing producers like OPEC, who are also able to increase or decrease production rapidly.

This new phenomenon has presented another challenge to OPEC. The organization’s most potent tool – coordinated production cuts, or the price increases they caused – would now suddenly result in a rapid loss of market share. U.S. shale companies would thus gain ground at OPEC’s expense, on the back of higher prices.

The challenge of plentiful and more flexible oil supplies was so big that in 2016 the group assembled OPEC+, a first-of-its-kind alliance with Russia and other non-OPEC producers to agree on coordinated production cuts.

For the Russian oil industry, however, every production cut has been imposed at the companies’ expense. The Russian tax system is designed in such a way that some instruments are imposed on a sliding scale varying with oil prices. As a result, Russian oil companies do not benefit much from higher prices, whereas they do benefit from higher (export) volumes. Furthermore, they have investments in the pipeline that they are keen to undertake.

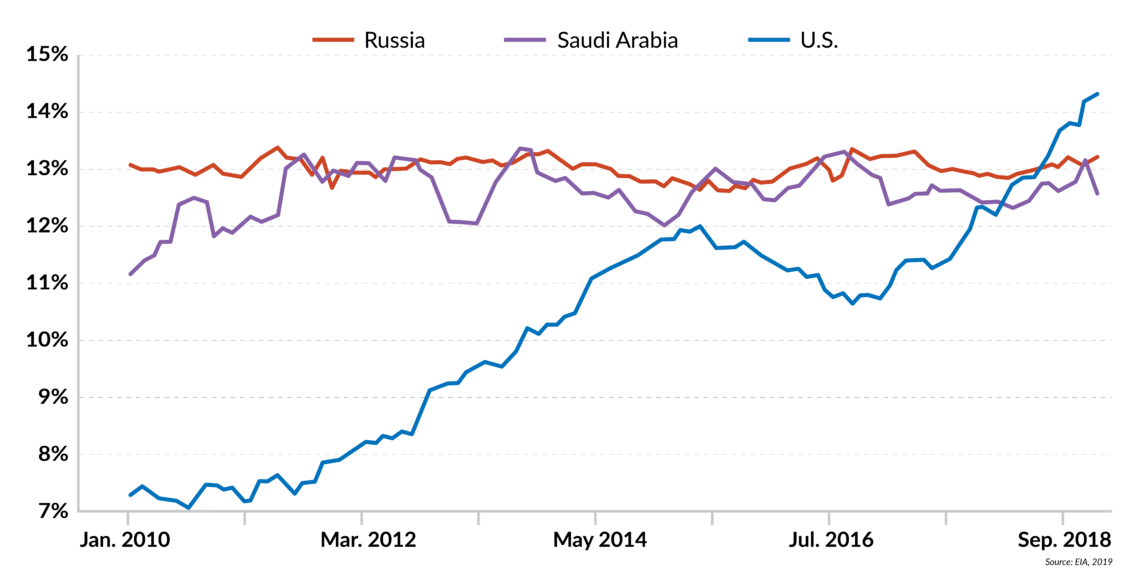

Since 2017, the U.S. has surpassed Russia and Saudi Arabia to become the world’s largest oil producer, which was facilitated by the latter two countries’ self-imposed production cuts as part of the OPEC+ deal. The attempt of OPEC+ to grapple with the new competition and to maintain production management to balance the market, rather than letting prices do the job, continues to define the global oil story. However, the more successful OPEC+ is in keeping prices artificially elevated, the faster the growth of U.S. production.

Diminished premium

Traditionally, when tensions arise in key producing regions, oil prices rise. The increase is often attributed to “geopolitical risk premium.” The potential for this premium to rise is higher when the oil market is tight; for example, when growth in supplies is not keeping up with increases in demand. Conversely, the premium shrinks (or may even disappear) when the oil market is well-supplied. For years, analysts have tried to measure the geopolitical risk premium, but no one knows how to quantify it.

Facts & figures

Global oil market share

In May 2019, Saudi Arabia and the United Arab Emirates reported that Saudi tankers and vessels off the coast of Fujairah were sabotaged. Two days later, Saudi Arabia said that armed drones hit two of its oil pumping stations, with Iran-aligned Houthi rebels from Yemen claiming responsibility. On June 13, 2019, two oil tankers – one Japanese-flagged, the other Norwegian-flagged – were damaged in the Gulf of Oman, south of the Strait of Hormuz.

The strait is one of the most important and strategic waterways in the world. An average of almost 16.8 mb/d of seaborne oil passed through it in 2018, equivalent to nearly one-third of the world’s total crude and liquids that are carried across oceans on tankers. The Strait of Hormuz is also the key export route for Gulf crudes.

Despite risks of supply disruptions, oil prices have seen low short-term volatility.

Given the strategic importance of the strait, some expected prices to rise significantly following the recent incidents. In reality, prices have reacted surprisingly little to the escalating tensions in the Middle East.

New normal

Since January 2017, OPEC+ has been trying to “rebalance” the market, an expression made popular by the organization. In reality, it means achieving a market “rebalance” at a higher oil price than what the system would have generated by itself, since markets can always take care of this themselves outside intervention.

While OPEC+ has succeeded in setting a price floor, the price upside has been constrained by tight oil and the plain fact that there is too much oil around. As a result, despite elevated risks of supply disruptions mostly within OPEC and tensions in the Middle East, oil prices have experienced relatively low short-term volatility and remained in a corridor of $60 per barrel, plus or minus $10/bl. The oil market seems to have found a “new normal,” which is a far cry from what oil markets were accustomed to less than a decade ago.

Facts & figures

The shifting oil landscape

- OPEC accounted for 41.5% of world supply in 2018

- By March 2019, crude oil production in the U.S. reached 12 mb/d (EIA, 2019)

- U.S. oil production in the 2040s may vary from less than 10 mb/d to more than 20 mb/d, depending on the assumptions used

- Under the terms of 2016 OPEC+ agreement, OPEC countries would cut their production by 1.2 mb/d while non-OPEC partners would jointly reduce their output by 558 thousand barrels per day

- In the “Tanker War” during the 1980-1988 Iran-Iraq war, almost 240 tankers came under attack and 55 of them sank