Oil prices in 2019

Where are oil prices headed in 2019? In the long run, the slowly rising global demand for energy will not be enough to offset the declining costs of extraction. In the short term, much depends on U.S. producers, whose shareholders are dissatisfied. The Russians and the Saudis would like prices to go higher.

In a nutshell

- Long-term, shrinking extraction costs will have the biggest impact on oil prices

- In the short term, producers are likely to run down their inventories

- Thereafter, American producers may restrain production to push up prices

- President Trump could convince the Saudis and Russians to do the same

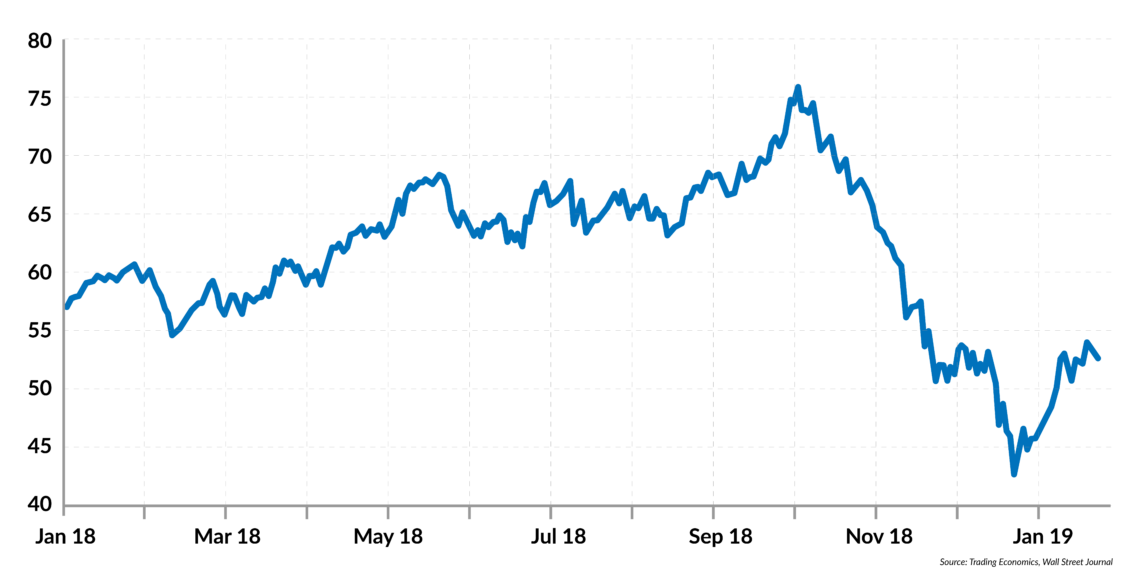

Oil prices behaved according to the rule book for most of 2018. As fears about an all-out global trade war receded, expectations grew that oil demand would rise. Hence, oil prices increased by almost 30 percent, from about $58 per barrel in January 2018 to about $75 in early October. During the next three months, however, oil prices collapsed to about $45 (40 percent), though they have since recovered somewhat, to about $53. What happened? And what will happen next?

To be fair, some alarm bells were already ringing almost a year ago. Last spring, oil prices crossed the $60 threshold and several observers promptly pointed out that something was amiss. Supply was building up rapidly, and not only within the Organization of the Petroleum Exporting Countries (OPEC). A suspiciously large number of tankers were loitering offshore, waiting for prices to rise further before unloading their cargoes. Suppliers were producing and stockpiling their oil, rather than selling it, in hopes of snatching better deals simply by waiting.

They had good reasons to do so. For example, in April Saudi officials declared they were confident oil would reach $80 before long, and some experts thought $100 was a feasible goal. As we now know, the strategy paid off for those who did not wait too long and moved before major producers changed tack and began selling.

Three predictions

To get a clear picture of what the future holds, we can start by observing that oil markets will be heavily influenced by two variables. Since global oil demand is expected to rise by at least 1 percent a year for the next decade, and perhaps stabilize afterward, prices will depend on drilling costs in the long term and on inventories in the short term. Given the speed of technological advances recently – which affect both extraction costs and the demand for oil for transportation – it is relatively easy to make three predictions.

Oil prices will follow a long-term decline until investing large sums in drilling technology becomes unprofitable.

First, oil prices will follow a long-term decline until investing large sums in drilling technology becomes unprofitable. If one looks at the rate of technological progress that has characterized the past decade, this will probably happen when the price of crude oil reaches about $30 per barrel.

Second, short-term prices will clearly react to unexpected changes in demand provoked by two phenomena. One is the rapid shift toward electric-powered transportation, combined with more energy-efficient ways of generating electric power. The obvious substitutes for oil are cheap natural gas and/or renewable sources. The other relates to the growth prospects of several undeveloped countries in Asia and Africa. These countries are still largely dependent on oil. Should their growth accelerate, their demand for oil will rise, too.

Third, short-term fluctuations in oil prices will also depend on broader geopolitical phenomena and on what the leading actors believe a reasonable price for oil should be. Since in many countries oil production is controlled by the state, politicians’ views and decisions about “desirable supply” matter. This applies to individual countries as well as multilateral agreements (like OPEC), or even combinations of the two (such as the ad hoc understanding between OPEC and Russia).

Opinions on appropriate price levels differ. For example, United States President Donald Trump has repeatedly said that he considers “excessive” any price above $60 per barrel. On the other hand, Russia needs an oil price of at least $60 to maintain economic growth. Russia’s gross domestic product (GDP) grew at a rate of about 1.7 percent in 2018, but the figure could drop below 1 percent if oil prices stay at their current level.

Saudi Arabia, for its part, needs an oil price of about $80 per barrel and no significant output cuts to curb its budget deficit (currently about 7 percent of GDP) and finance a large public expenditure program designed to make the country less dependent on oil exports. Reaching and enforcing a compromise among these big players is hard. Moreover, the bargaining process itself could become a powerful source of uncertainty and therefore price volatility.

The Americans’ choice

Given this rather broad picture, two scenarios are possible. The U.S. is likely to play a key role in both. From the political viewpoint, President Trump has considerable power over American oil production and exports and can play a significant role in terms of global supply.

Crucially important is that American economic performance is far less dependent on oil than that of other oil superpowers, such as Russia or Saudi Arabia. Accordingly, the U.S. has more freedom to choose its strategy and the means to implement it.

President Trump’s ability to rein in American producers is also a critical element. In the past, producers have invested considerable sums in drilling technology and equipment, largely related to tight-oil extraction, otherwise known as fracking. Until last September, however, a substantial portion of this production capacity lay idle; even facilities in operation were not delivering the anticipated output. Stockholders are eager to recoup their investments, which in many cases have been a fiasco.

The Russians and Saudis can do little unless their moves harmonize with the Americans’ strategy.

The ball is now in the Americans’ court, and much depends on what the U.S. producers do. The Russians and Saudis can accomplish little unless their moves harmonize with the Americans’ strategy. U.S. producers must choose between restoring profitability by cutting production and letting prices rise (the first scenario) or by expanding output regardless of the oil glut that would likely follow (the second scenario).

In the first case, U.S. companies will need to strike a deal with Russia and Saudi Arabia on doing what it takes to push crude oil prices close to $60 a barrel – a level that would make Russia happy and that the Saudis could eventually accept, albeit reluctantly. In the latter case, oil prices are bound to tumble another 30 percent and stay there for a couple of years or more – until the flow of American tight oil peters out (exploiting an oil well through fracking delivers high output only initially).

New framework

We tend to believe that the first option will ultimately prevail, despite short-run volatility triggered by fears about Chinese growth and supply uncertainties: What will the Americans do, and will other suppliers follow? In the very short term, oil producers will likely run down their inventories: some to meet the expectations of disappointed shareholders and others to comply with tight budget constraints (the Russian and Saudi treasuries). Hence, oil prices could drop further.

Before mid-2019, however, a trilateral cartel could solidify and shape a new framework for the world oil market. This framework would be fragile, because it would be vulnerable to geopolitical tensions such as conflicts in the Middle East and strains between the U.S. and Russia. Yet, a deal among these three leading producers could guarantee relatively high oil prices (say, in the $55-$60 range) until early 2020, when the main actors will reconsider the entire situation.

This scenario would also involve an important side effect. A joint effort to prop up prices would be in vain if economic growth stalls in China and in some large developing countries. Hence, a commitment to support oil prices is also a commitment to enhance global growth.

That would be good news for everybody, even in the oil-importing countries, and great news for all those who support free trade. The next steps in the trade saga inaugurated by President Trump will tell us whether the scenario presented in this report is realistic.