Parsing the ECB’s strategy on ‘lower bound’ inflation

In its latest strategy statement, the European Central Bank points to the “lower bound” of inflation – zero percent or lower – as an economic trap that must be avoided through “forceful” and “persistent” measures.

In a nutshell

- The ECB is no longer putting a ceiling on inflation

- It is pushing the limits of monetary policy to avoid disinflation

- Prolonged high inflation could prove highly problematic

On July 8, 2021, the European Central Bank (ECB) announced it was renewing its guiding principles for conducting monetary policy. After 18 years, this second strategy review in the institution’s 23-year history was long overdue. When taking office in November 2019, ECB President Christine Lagarde had made it a priority. Because of delays caused by the Covid-19 pandemic, it took her team 18 months to produce the much-awaited document. The new strategy statement is concise. In 12 short paragraphs, the ECB presents its revised policy framework.

New goals

Two innovations stand out compared to the previous strategy statement, published in 2003. First, the strategy moves the inflation target from below, but close to, 2 percent to simply 2 percent. At first glance, that does not seem like a substantial change. What it implies, though, is that the ECB is committed to a “symmetric” target, rather than just a ceiling to keep inflation low. From now on, both “negative and positive deviations” from the 2 percent target should be considered as “equally undesirable,” according to the new strategy.

Second, the statement lays out a new goal for the ECB: combating climate change. The communique comes along with a rather vague “action plan” for including climate considerations into the monetary policy framework (notably when it comes to future corporate sector asset purchases), as well as a “roadmap ” for implementing greener monetary policy over the next four years. For a start, the ECB wishes to gain deeper insight into the implications of climate-related risks for price and financial stability.

The strategy has not met expectations on several fronts.

The Lagarde review triggered a wide variety of reactions. Some say there is too much change; others say there is too little. Some had hoped for a higher inflation target, others for a lower one. Some think the review is just another compromise package; others assert it is a revolutionary framework in which monetary and fiscal policy can at last converge. Some insist that central banks should have nothing to do with climate change, and others regret that the ECB’s new environmental commitments do not go far enough. On almost every point listed in the document, experts appear divided, meaning it has not met expectations on several fronts.

Forceful response

The question-and-answer session following the strategy review press conference was particularly revealing in this respect. The journalists kept asking versions of the same question: does the ECB now want higher inflation? In response, President Lagarde tirelessly repeated versions of the same phrase from the communique: “[W]hen the economy is close to the lower bound, this requires especially forceful or persistent monetary policy measures to avoid negative deviations from the inflation target becoming entrenched.” She added that if “adverse shocks” were to hit an already depressed economy, an “especially forceful reaction” will be needed. “Closer to the effective lower bound, those actions might be more persistent.”

Facts & figures

When pressed, she eventually offered one concrete example of an “especially forceful” and “persistent” policy response to an acute crisis: the Pandemic Emergency Purchase Program (PEPP). In 2020, the bank scaled up that initiative’s spending power to a vertiginous 1.85 trillion euros within just a few months.

Change of focus

The key term here is “lower bound” – and it is the cornerstone of the 2021 strategy. At issue is a prolonged period of low interest rates, low inflation and low inflation expectations. President Lagarde has insisted all along a vicious cycle starts when short-term interest rates approach the lower boundary of zero (currently, they are even slightly negative, at -0.5 percent). At this point, conventional monetary policy loses its ability to stimulate the economy through rate cuts. But that is not the only problem. When inflation falls short of the central bank’s self-imposed target over a longer time span, people’s disinflation expectations can become ingrained and self-fulfilling.

By putting the lower-bound constraint at the heart of the new strategy review, the ECB is really announcing a complete reversal of its policy focus. For the 2003 framework, monetary policy’s concern was to keep inflation from rising too high. For the 2021 framework, the challenge is to prevent it from dropping too low. The previous strategy came at a time of low economic volatility and gave policymakers little insight into addressing deflationary threats. It simply advised them to raise interest rates when inflation overshoots the target. Ms. Lagarde’s team designed the new strategy to address this shortcoming.

Pushing the limits

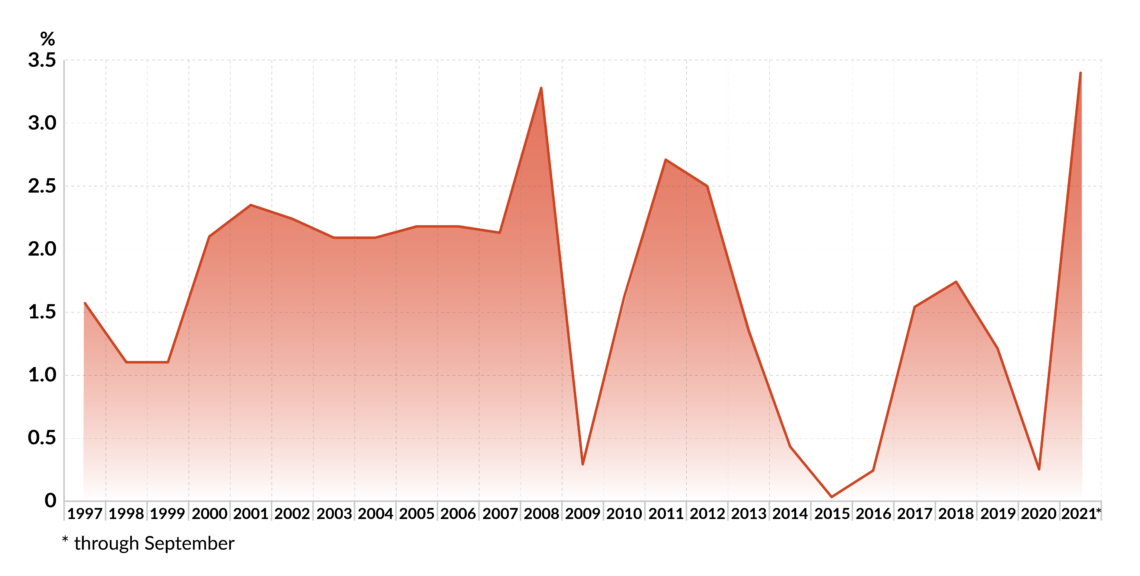

For decades, deflation was a nonfactor in the eurozone. Then came the Great Recession, which pushed inflation lower. Annual rates fell from 3.28 percent in 2008 to 0.29 percent the following year. The ECB reacted with interest rate cuts that were no less drastic. Deposit facility rates, which define the interest banks receive for depositing money with the central bank overnight, fell from 3.25 percent in October 2008 to 0.5 percent in April 2009

As a result, inflation picked up again in 2010. Then, it overshot the target in 2011, coming in at 2.71 percent and leading the ECB to raise policy rates to 0.75 percent. That decision did not consider increasingly volatile sovereign bond markets or banks’ potentially disastrous balance sheets. In hindsight, the choice to tighten monetary policy during a European debt crisis was an error of historic proportions.

The choice to tighten monetary policy during a European debt crisis was an error of historic proportions.

Mario Draghi, who took over in late 2011, was the first ECB president to understand the significance of inflation falling toward the lower bound. As the recession deepened and concern grew about whether the euro could project survive, he believed the ECB needed to push monetary policy to its limits. In his first days in office, he slashed rates. They eventually reached zero on July 11, 2012. The next day, Mr. Draghi delivered his famous speech in which he committed to do “whatever it takes” to preserve the euro. ECB chief’s words helped bring the situation under control, and the institution’s credibility as a lender of last resort and stabilizer of debt markets hit an all-time high. Inflation picked up again, hitting 2.5 percent in 2012.

At that point, the 2003 policy framework would have advised the ECB to start raising interest rates again. For Mr. Draghi, however, doing so was out of the question – and his instinct proved correct. For the first time in the ECB’s history, Mr. Draghi allowed interest rates to slightly descend into negative territory (measured year-on-year from December 2014 to March 2015). Soon, annual inflation was back on a downward slope. It hit 0.03 percent in 2015.

In the absence of a framework for addressing such low inflation, he took pragmatic steps. In 2015, he launched the first packages of large-scale quantitative easing (QE), through which the ECB has subsequently pumped trillions of euros into the eurozone’s financial system.

The ECB’s Asset Purchase Programme temporarily ended in late 2018, when inflation was close to target, at 1.74 percent. However, less than a year later – just before handing over the ECB to Christine Lagarde – Mr. Draghi reopened the easy money tap, anticipating that the lower bound threat was not over. At the time, members of the ECB’s Governing Council and others heavily criticized his decision since he did not make the move in response to an emergency.

Permanent crisis mode

In a way, the 2021 strategy is an attempt to put former President Draghi’s approach to crisis management in a framework to guide the ECB’s monetary policy going forward. Many now acknowledge that the unconventional tool kit he developed is an integral part of the ECB’s policy arsenal – not just in times of crises, but also in normal times. Ms. Lagarde’s statement makes clear that for the ECB, the new normal could resemble permanent crisis mode. The new framework prepares policymakers for a scenario in which our economy will ceaselessly gravitate toward the lower bound. ECB executive board member Isabel Schnabel calls it “a strategy for a changing world.”

According to the official narrative, the recent shocks like the financial crisis and Covid-19 have exacerbated the problem but did not create it. The downward spiral could be inexorable. In its opening lines, the ECB statement points to “profound structural changes” the economy has undergone over the past two decades. It lists aging populations, declining productivity growth, globalization, digitization and threats to environmental sustainability among the culprits driving down “equilibrium real interest rates” and increasingly obstructing monetary policy’s ability to steer the economy in the right direction.

Some economists argue that secular stagnation – in which private savings rise and investments languish – is the culprit for the current situation. According to them, it is not policymakers’ fault that inflation has remained tenaciously low despite years of monetary expansion. This is a convenient explanation for monetary policy’s decreasing effectiveness.

Tricky position

To quote British economist Charles Goodhart, QE was “originally successful,” but today is largely a “spent force.” In other words, central banks need to do more to achieve less. Still, the ECB continues to say that low interest rates and quantitative easing are the only ways to “resist” the ever-looming threat of the lower bound. Yet, at the same time, inflation-boosting measures must grow increasingly “forceful” and “persistent” to keep a chronically depressed economy afloat. According to the strategy, the ECB would “tolerate” a situation where inflation overshoots the 2 percent target, as long as it remains “transitory.” The central bankers do not say how much of an overshoot they will tolerate, or for how long.

The ECB continues to say that low interest rates and quantitative easing are the only ways to resist the ever-looming threat.

While the ECB was finalizing its new strategy, inflation unexpectedly picked up in Europe (and even more so in the United States). Many economists now predict that moderately high inflation will linger in the eurozone over the long term. The ECB’s own projections foresee inflation at 2.2 percent in 2021 but hold onto the assumption that the sudden surge is due to temporary factors that will fade in the coming years.

If higher inflation is here to stay, the ECB’s position will become trickier. The new commitment to keep inflation near 2 percent would require a return to restrictive monetary policy. The hawks at the Governing Council are already pushing to scale back the PEPP. As inflation increased to 3 percent in August, the ECB made a slight concession to these hawks, announcing that flexible bond-buying under PEPP will continue “at a moderately lower pace,” if conditions allow.

Stimulus forever?

The problem is that the eurozone economy is hopelessly addicted to easy money. Slowing down QE could plunge Europe into a deep recession.

In a way, QE, more than the lower bound, has become a trap for our over-indebted economies. They would find weaning themselves off the money flow highly problematic. The ECB’s leaders seem to have committed to stimulus, even in times of prolonged inflation. But then, of course, they could be accused of monetizing debt, which EU treaties prohibit.

To paper over this dilemma, the ECB will need to be ever more imaginative to prop up the narrative that the lower bound is a structural feature of the eurozone economy.