Risks and requirements for German gas and energy policy

Berlin is looking past the immediate energy crisis to reduce Germany’s dependence on Russian gas.

In a nutshell

- Putin has weaponized Europe’s gas dependency

- An EU gas import ban would hit Russia financially

- Returning to the prewar energy partnership is not realistic

Germany’s current dependence on Russian gas imports is the result of misjudgments, mistaken assumptions and a denial of geopolitical realities in its Russia policy. Berlin has underestimated the supply security risks since 2005, when it agreed with Moscow to build the Nord Stream 1 gas pipeline. Climate and environmental policy, as well as supposedly “cheap” Russian gas, have shaped Germany’s Energiewende at the expense of supply security and a realistic energy transition.

Even after Moscow’s annexation of Crimea in 2014, Germany’s gas import dependence on Russia – contrary to the EU’s 2010 and 2014 gas security strategy of greater diversification – rose from 45 to 55 percent. The new coalition government in Berlin has begun to rebalance its approach to gas and overall Energiewende to become more sustainable and resilient in a new geopolitical environment without Russian gas.

Export squeeze

With Russia’s recent gas export cuts, initially at 40 percent and up to 60 percent in June, President Vladimir Putin has again demonstrated his intention to capitalize on Europe’s gas dependency. Since Russia conducted 10 days of maintenance work on Nord Stream 1 (which has an annual capacity of 55 billion cubic meters (bcm)) in July, the German government and the European Commission have feared that Russia may entirely halt the flow of gas supplies to the European Union.

Predictably, at the end of August, Russia halted the Nord Stream 1 pipeline flow for another several days because of technical problems at a compressor station (which in reality could be repaired without a complete stop of supply). At the beginning of September, Kremlin spokesperson Dmitry Peskov admitted publicly that Nord Stream 1 would not resume supplies until Western sanctions against Russia are lifted.

Following the Kremlin’s invasion of Ukraine and the imposition of Western sanctions, the EU agreed to drastically reduce fossil fuel imports from Russia, hoping to cut revenues that could finance the war. The easiest step is stopping Russian coal imports because there are enough available import alternatives, and the EU already hopes to rapidly wean itself off coal. The German government ceased importing Russian coal in August.

Yet compared to the EU’s declared oil embargo, set to take effect only in December 2022, Germany – supported by other EU members – has insisted it is unable to impose a gas embargo due to fears of economic repercussions. In an April 15 interview, Russian Energy Minister Alexander Novak expressed his confidence that the EU would not be able to replace Russian oil and gas within the next five to 10 years.

The Russian president has escalated the energy conflict with Germany and the EU by announcing that all energy exports must be bought in rubles. Mr. Putin is seeking to blunt sanctions facing the Russian central bank and fracture the EU’s political cohesion.

However, German and other European gas import companies’ contracts only allow payment in euros or dollars. A mechanism devised by Germany, Italy and Austria to legally comply with the sanctions imagines energy bills paid in Western currency to Russia’s Gazprom-Bank, which then exchanges them into rubles (though only to 80 percent). But ultimately, these “solutions,” which exploit legal technicalities to suggest compliance, in fact, strengthen the ruble and undermine Western sanctions.

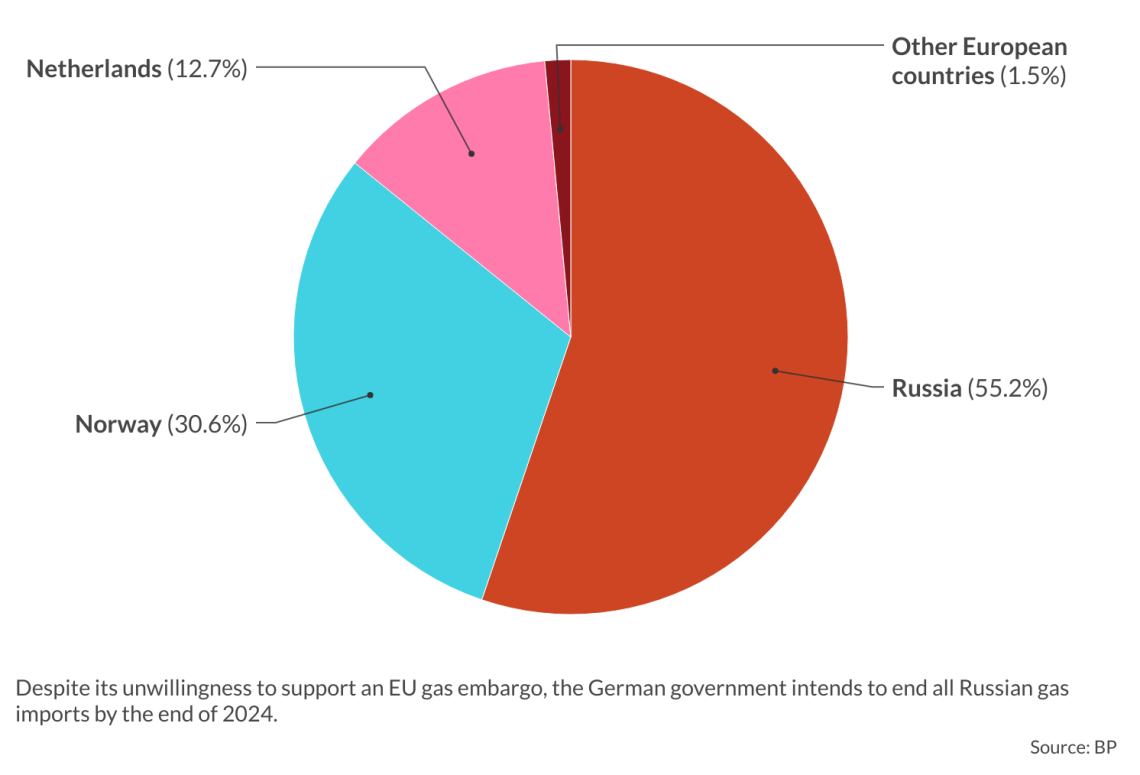

Despite its unwillingness to support an EU gas embargo, the German government intends to end all Russian gas imports by the end of 2024. Officially, its current gas import dependency had already been reduced from 55 percent in 2021 to less than 35 percent this past May.

Mr. Putin is seeking to blunt the sanctions facing Russia’s central bank and fracture the EU’s political cohesion.

But German and European reduction of Russian gas imports has not only been the result of efforts to diversify or to reduce consumption. Russia itself decreased its own gas supplies via Nord Stream 1 by 80 percent, citing maintenance work in July. Moscow has also reduced gas supplies flowing via Ukraine and (temporarily) the TurkStream-2 pipeline (an annual capacity of 17.5 bcm) without any justification.

After a 60 percent reduction of gas supplies prior to the Nord Stream maintenance work, the Kremlin officially blamed a broken Siemens gas turbine, which was sent for repair to Siemens Energy Canada. According to an unofficial source with the company, however, the turbine had no technical problems at all. While Canada delivered the turbine back to Germany, it had been refused transit to Russia, which cited improper documentation. Both Siemens and Berlin have denied any technical problems or any such document problems. Shortly afterward, Gazprom declared that another turbine now needs repairing along Nord Stream 1, which employs eight in total. (In fact, operating the pipeline requires only five turbines, as three are held in reserve.)

Typically, for periods of maintenance work, gas contracts also regulate how the missing supplies are replaced using other transport routes. Even though the Yamal pipeline through Belarus and Poland had been shut down last May because Poland did not sign a new contract with Gazprom, the capacities of Ukrainian gas transit – despite the war – would still be large enough to compensate. But Russia has not used this option either.

A complete halt of Russian gas exports to Europe without German or EU countermeasures could indeed lead to crisis, possibly forcing Berlin to resort to its stored gas reserves much earlier than originally planned. That threatens its plan to further fill gas storage capacity to 95 percent by November 1 – which is essential for sufficient supply during the winter, particularly if the weather is colder than in recent years.

A Russian embargo?

Moscow cutting supplies through Nord Stream 1 would not mean a total gas export embargo on the EU as long as gas still flows to Europe via Ukraine and TurkStream 2 and as liquified natural gas (LNG).

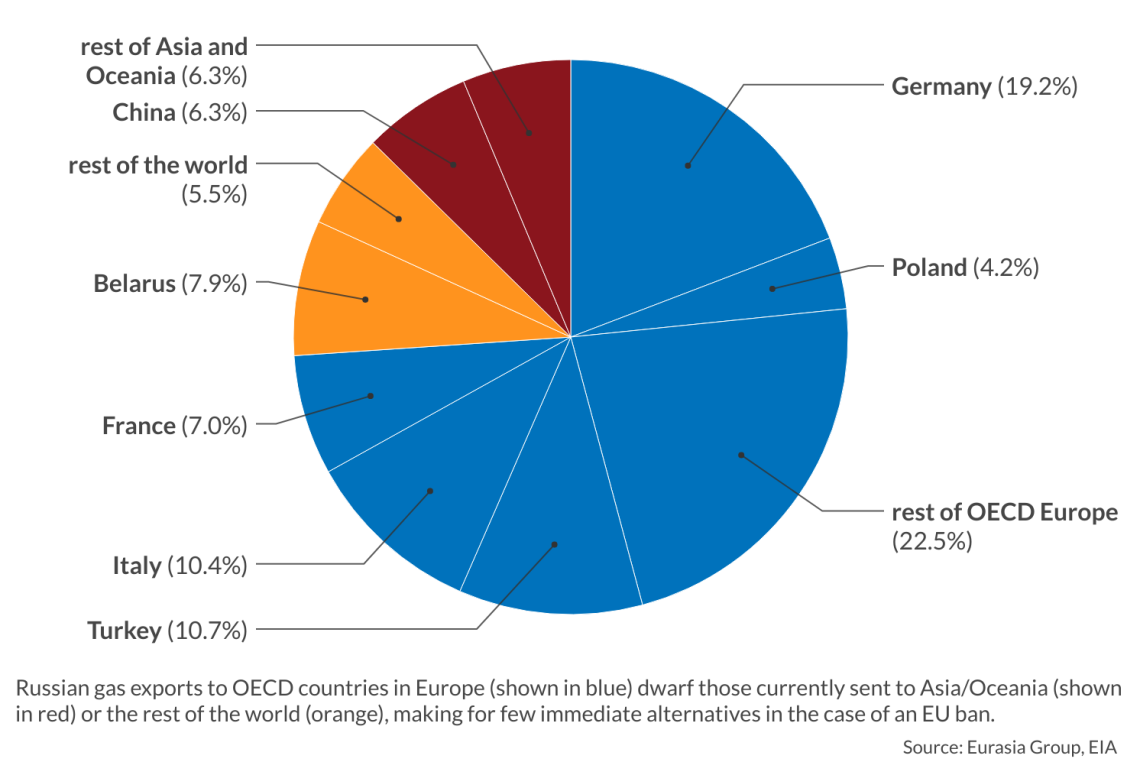

An EU gas import ban would financially hurt Russia more than the already declared EU oil embargo. Under the oil ban, Russia could still sell products previously bound for Europe to other countries via tankers (albeit with a loss). But in the event of a complete EU pipeline gas import embargo (or a Russian export gas ban to the EU), Russia cannot redirect its gas exports to Asia and other global markets, as alternative gas pipeline infrastructure is lacking.

Russia currently has only one gas export pipeline to China – Power of Siberia 1, with a capacity of 38 bcm per year – but it will not be available at full capacity until 2025. Gas exports to China and Asia are also far less profitable for Russia.

Last year, only 10.5 bcm of gas was exported to China via the Power of Siberia 1, and another 5.5 bcm as shipped LNG, together less than a tenth of the size of Russia’s exports to Europe. Moreover, concluding new gas contracts with other Asian countries and building new pipelines to Asia or Russian LNG ports in the Far East would take at least five to 10 years.

Instead, by further reducing its gas exports to just 20 percent of its contracted gas supplies via Nord Stream 1 this past July, the Kremlin continued to employ a divide and conquer strategy, playing individual European states off each other and weakening the EU’s political unity regarding the Western sanctions and military aid to Ukraine.

Nonetheless, it cannot be ruled out that Russia will halt all gas exports to Europe in the autumn or winter, despite the economic consequences. President Putin may also consider that Germany will no longer import any Russian gas from 2024-25. Russia could benefit more through the escalation of a gas export ban and cause further gas price explosions, fueling sociopolitical polarization and undermining Western resolve.

Coping without Russian supplies

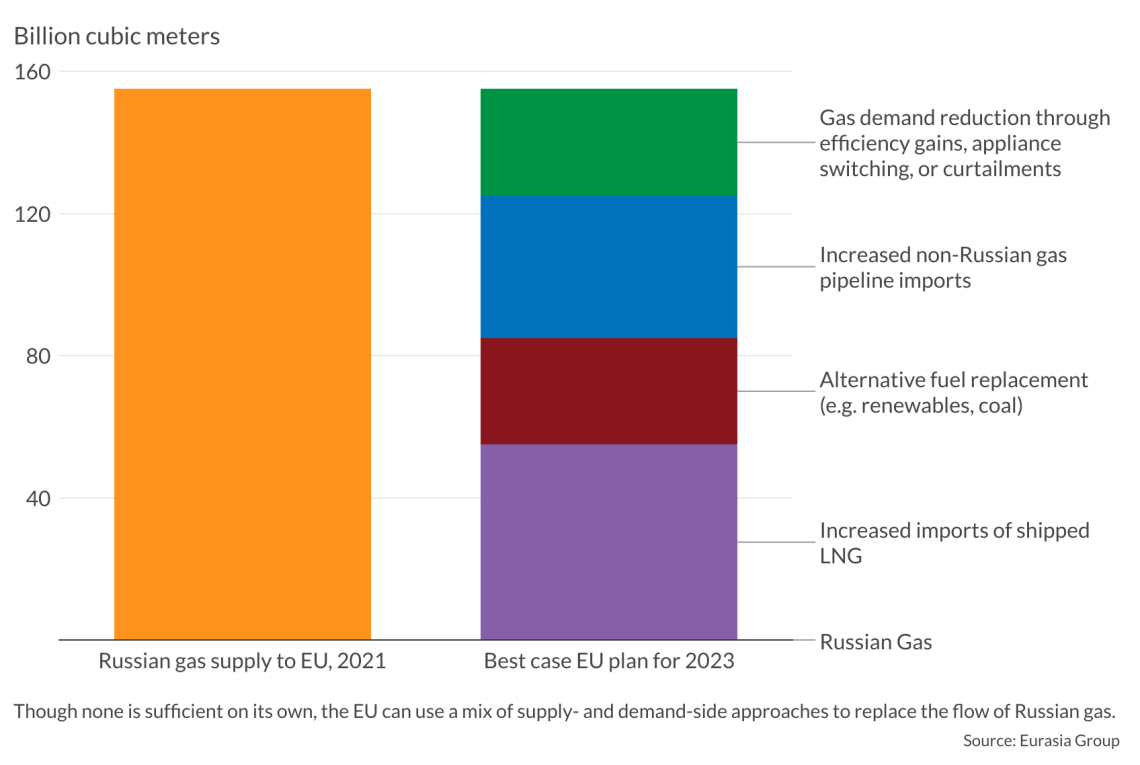

Both German and EU plans to counter lower or halted Russian gas supplies use a combination of measures, ranging from increased LNG and non-Russian pipeline gas (Norway, Algeria and Azerbaijan) to the replacement of gas consumption by other energy sources (renewables, but also coal and oil) and various initiatives for conservation and energy efficiency.

Diversifying imports

The government’s original assumption of making available three or four floating storage and regasification units (FSRUs) by the end of the year has proven unrealistic. Only one of these floating LNG import terminals will become available, in Wilhelmshaven (even if an additional 30 km gas interconnector to the pipeline network may not be available until January), along with a possible second FSRU in Brunsbuttel in January or February of 2023. But both may initially lack full regasification capacity.

This has made it more uncertain as to whether Germany will have enough gas to get through the winter. Two other FRSUs will only be available later in 2023 and 2024, and the completion of the fixed on-land LNG import terminals will take place in four years at the earliest. Two additional FSRUs are under discussion for Hamburg and Lubmin. Altogether, the German government has supported the charter of five FSRUs.

Consumption savings

Germany has still not declared a “level three” state of gas emergency, which allows the federal government to ration national gas consumption. This could even lead to the temporary closure of companies in energy-intensive industries. But predictions of economic and industrial losses vary significantly due to the potential cascading impacts on complex supply chains and affected industries.

Government appeals for people and businesses to save gas now – warning that if they do not, prices could triple by the end of the year – have already seen some effect: in the first five months of the year, demand for gas fell 14 percent (though it is also explained by the mild weather during last spring). Although there are possibilities for other savings, such as optimizing almost 7 million gas boilers, which had a 68 percent market share in 2021, any short-term readjustments to gas heating systems are constrained by a shortage of 60,000 craftsmen in the German heating industry.

A planned auction mechanism set for September, under which companies can sell the gas they conserve, appears more promising. That will also provide the government with a range of data for the so-called Gas Safety Platform, set to launch in October, allowing companies to replace and/or save gas in the short term.

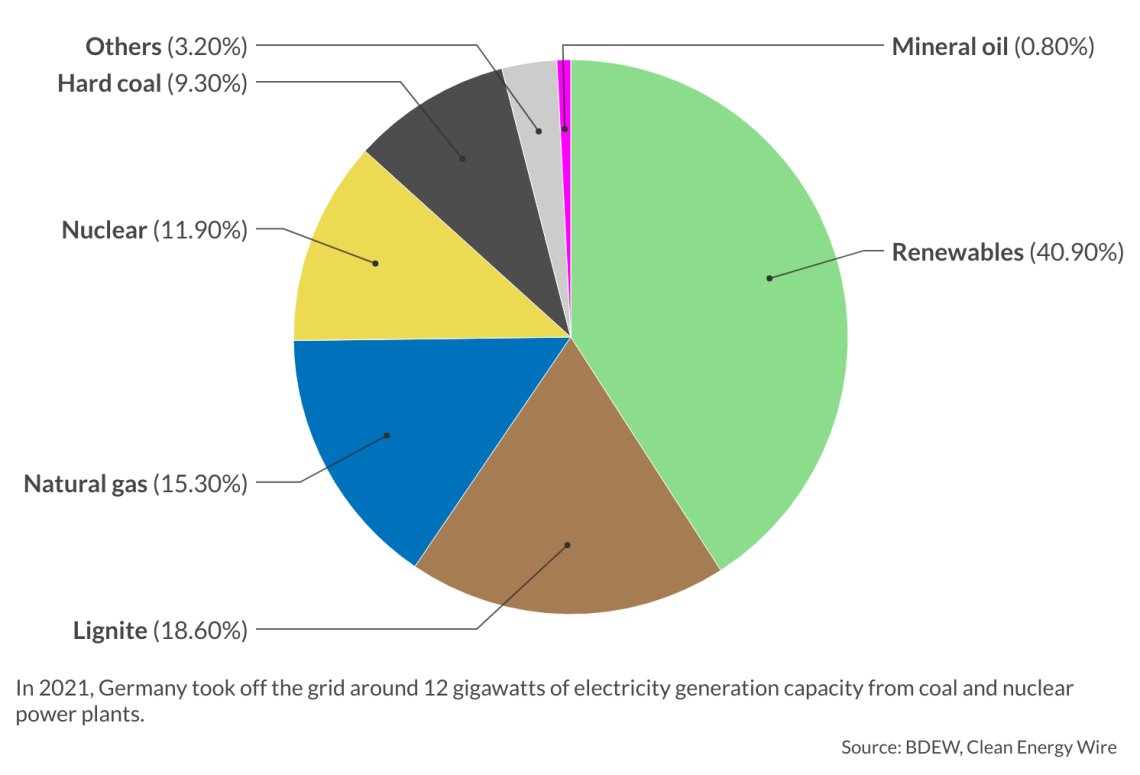

The most effective is the gas-to-coal transition in power generation, seeing gas-fired power plants replaced by coal-fired plants (that have around 40 percent higher CO2 emissions). Last year, around 12 gigawatts (GW) of electricity generation capacity from coal and nuclear power plants (NPPs) was taken off the grid. The German government is planning to bring back around 9 GW of mothballed coal-fired power plants over the coming months. But utilities’ prospects remain uncertain, as transport space on coal freighters for sufficient quantities of coal is limited. Furthermore, the present water levels of the Rhine and other rivers are so low that the freighters and other ships cannot be fully loaded.

As a result, Germany has too many gas power plants generating electricity. This has also led to rocketing electricity prices, as these plants are the last ones in the “merit order” system determining overall electricity prices – including for all other electricity-generating companies (such as renewables, which make huge profits given their low production costs). In response, the German government, alongside the European Commission and other EU member states, has called for some decoupling of EU electricity prices from gas prices, and an overall reform of the EU electricity market design. The government is also supporting lower- and middle-income households with various relief measures, in a new 65 billion-euro package to bring down soaring inflation and energy bills.

Shale reserves

Germany also has large shale gas reserves that could fully cover its annual gas consumption (of 2.3 trillion bcm) for more than 30 years.

The supposed environmental risks have already been characterized as manageable by major scientific studies both in Germany and by the European Commission since 2012, contrary to widespread perceptions of the outsize environmental dangers of fracking technology.

It is not politically credible to import shale gas fracked in the United States and at the same time reject German shale gas production. National shale production would also reduce gas imports, thus strengthening Germany’s gas supply security over the next decade. It would even contribute to global climate protection, as producing domestic shale gas emits significantly less methane and CO2 compared to LNG and pipeline imports, because the liquidation, re-gasification and transport of LNG is very energy and emissions intensive. In light of today’s extremely high LNG prices, domestic shale gas production would also be significantly cheaper than importing expensive LNG from outside Europe.

With the right political will, the approval procedures and legal changes needed for national shale gas exploration could be considerably hastened – enhancing gas supply security in the coming years for a transitional period, alongside greater EU gas production (in the United Kingdom’s North Sea, Norway and the Netherlands). But this scenario still does not appear to be the most likely, due to pressure from nongovernmental organizations as well as an ideological opposition against fossil fuels among SPD and even CDU/CSU elements in the German Bundestag and federal state parliaments.

Scenarios

The prospect of returning to the status quo ante of the German-Russian energy partnership and supposedly “cheap Russian gas” no longer appears realistic. That remains true even looking past President Putin’s tenure, with his replacement still possibly coming from the present power apparatus. Already before Russia’s invasion of Ukraine, the EU decided to decarbonize its energy supply by phasing out all fossil fuels, including natural gas, in the medium and long term. Even by 2030, the EU’s gas consumption was projected to fall by at least 20 percent.

Despite numerous efforts to diversify gas imports and reduce gas consumption, Germany could still experience a shortage this winter, at least locally or regionally (despite the fact that it has already filled its gas storage sites to more than 85 percent, four weeks ahead of an October 1 target). In countering Russia’s strategy of gas weaponization, Germany could be less reactive and instead unilaterally declare a “price ultimatum” to the Kremlin. It could use and bundle Europe’s purchasing power against Moscow to reduce Russian gas and oil prices and significantly decrease the Kremlin’s revenues from European gas and oil exports. Though this would temporarily lead to a short gas shortage over the winter, it would also help industry, private households and the German government plan more securely, allowing for more effective gas saving.

Otherwise, Berlin and the EU will continue to leave President Putin with a strategic edge in the present economic war of sanctions – able to stoke ever new fears about the supply of Russian gas, and to fuel polarization in Germany and other EU member states.