How will central banks tackle the next stage of inflation?

While the U.S. and the euro area appear to have avoided the worst, much depends on how central banks will react to unanticipated news in the coming months.

In a nutshell

- The fight against inflation is not over

- Central bankers’ short-term focus is on price stability

- Potential shocks could change their outlook

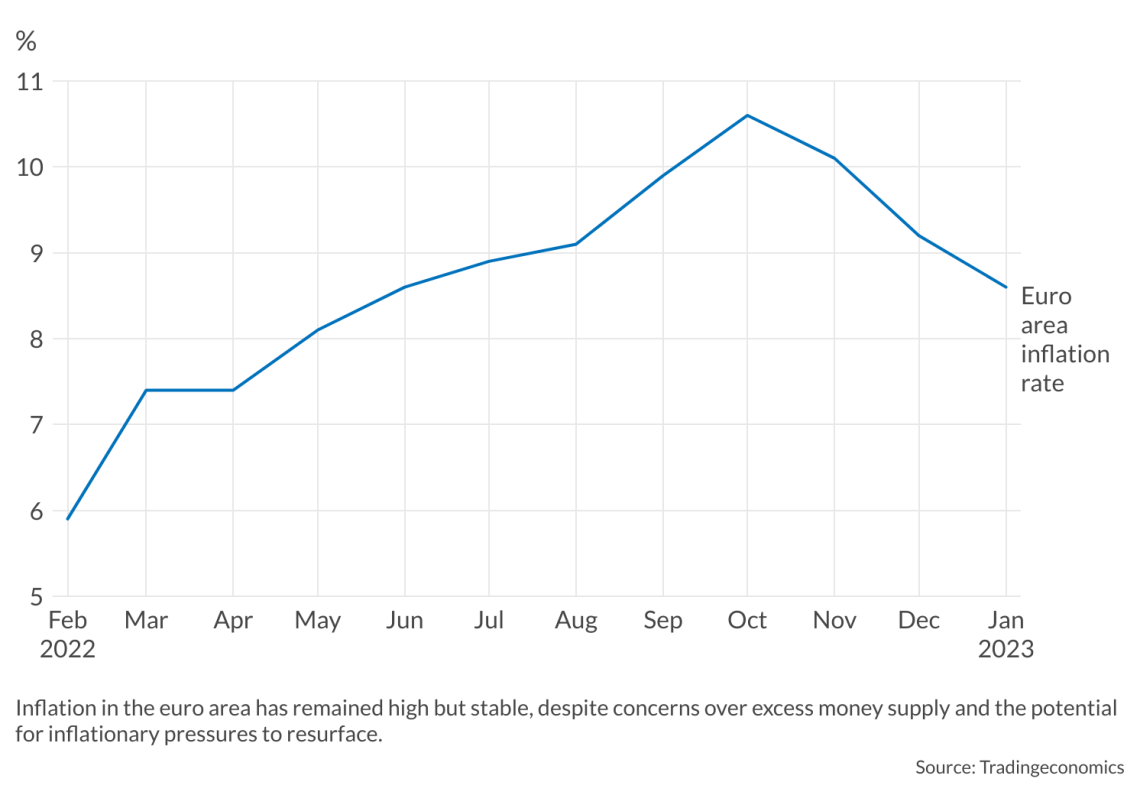

Inflation is still high, but under control – or so the world of business and financial markets believes. In the euro area, year-on-year consumer prices rose by 8.6 percent in January, down from 10.6 percent in October. Although core inflation is still rising (5.3 percent in January 2023 from 5.2 percent the previous month), many have breathed a sigh of relief, especially in Frankfurt. The stumbling block remains the excess money supply. It is declining now, but at the end of December 2022 M2 and M3 figures were still higher than at the beginning of the year.

In other words, these last months of tight monetary policy have done very little to eliminate the monetary overhang in the eurozone. The outlook is more encouraging for the United States, where the money supply is currently lower than a year ago. Core consumer price inflation is also retreating; it was 5.6 percent in January 2023. Although it is clear that the fight against inflation is not over, on both sides of the Atlantic it is generally believed that interest rates will stop rising in the second part of this year and perhaps drop a little early next year, and that no major crisis is in sight.

These perceptions are likely correct. But navigating the next few years of lower (but not negligible) inflation may not be all smooth sailing. Inflation started rising some three years ago in the U.S. and a few months later in Europe. Looking at what happened, there are three lessons to be learned that may help understand how future developments will unfold.

Understanding the causes of the inflation crisis

First, central bankers are not in control of monetary policies. They seem to oscillate between panicking when headline inflation deviates from the two-percent benchmark, and running to the rescue when major financial players threaten to go belly up and trigger systemic financial trouble. As a result, central bankers tend to operate day by day and react to the latest figures available. A telling example is the latest U.S. alarm about the unexpectedly high figure of the personal consumption expenditure (PCE) price index.

Second, both in the U.S. and in the euro area, the rise in nominal wages has fallen behind the rate of inflation. As real wages fell, many households had to use up their savings. Imbalances will follow.

Third, and not surprisingly, the main beneficiaries of this inflationary episode have been governments, whose debt has been cut significantly in real terms.

At its beginnings, central banking had little to do with price stabilization. Fluctuations in prices were considered normal. The gold standard was meant to provide an anchor that would prevent governments from tampering with monetary policy and interest rates, and punish them whenever they engaged in profligacy and ended up with exceedingly high public debt. In fact, central banks were created to bail out financial actors that would otherwise go bankrupt. After the gold standard was abandoned, independence and price targeting became makeshift measures to ensure that central banks would not become money printing machines.

The outcome has been disappointing. For example, between 2000 and 2020 the euro and the dollar lost 28 percent and 33 percent of their purchasing power, respectively. In fact, ever since the Bretton Woods corset was dismantled, central bankers have been wavering. At times they have prioritized bailouts, at other times price stability.

The next few months will likely focus on price stability, but only because no systemic threat is in sight. The picture could easily change if a shock of some kind took place – a new virus, a war, a climate-change scare, a public-debt crisis. In their absence, much depends on how central bankers interpret ongoing events.

Policymaking pitfalls

Central bankers have a paradoxical tendency to worry when economic activity picks up. Clearly, they believe that production capacity is a constant, that all increases in demand necessarily translate into higher prices, and that a wise central banker should react by raising the rate of interest and squeezing credit.

This is wrong for two reasons. First, supply is not a constant, as economic history demonstrates. Policymakers should rejoice when production and aggregate supply increase, since it is the best way to stabilize prices after a money-printing hangover. Second, the very idea that changes in demand should be brought under control is plain wrong. Changes in demand reflect past imbalances and/or new preferences.

Tampering with households’ demand, through monetary policy or otherwise, adds to uncertainty and provokes further distortions.

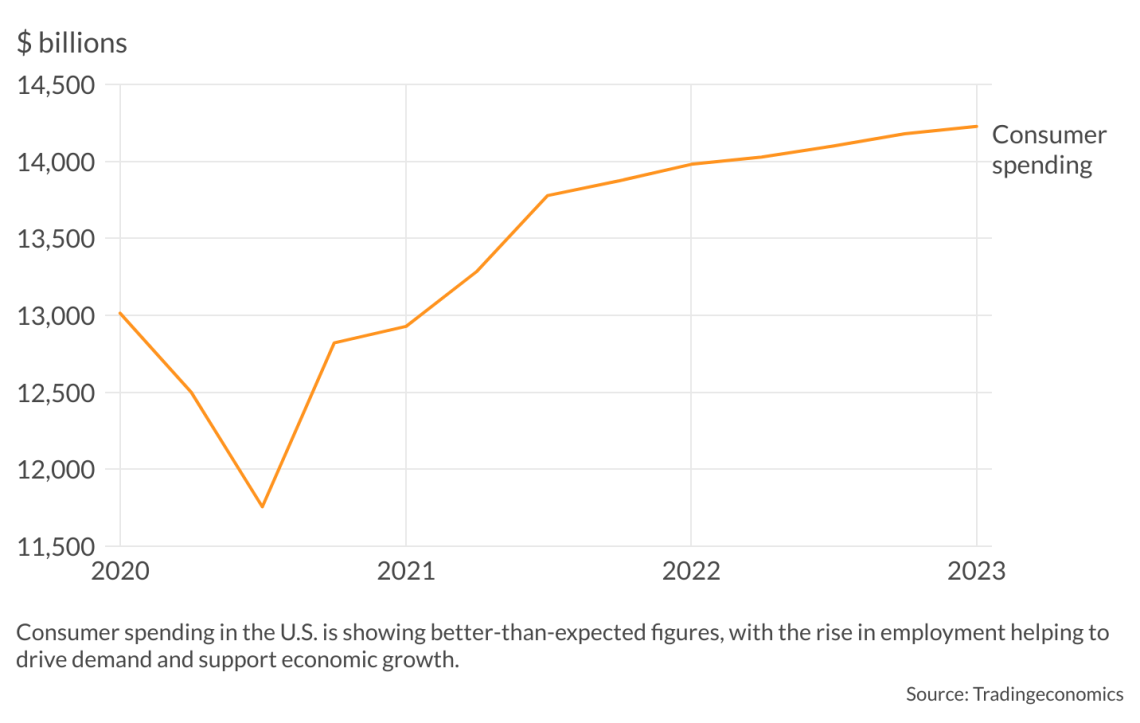

Consumer spending in the U.S. seems to be faring better than what observers had expected a few months ago. The rise in employment has certainly contributed to this phenomenon. U.S. employment in January 2023 was back to where it was before Covid-19 struck, 20 percent higher than in early 2020. This is good news. All else being equal, more employment means more supply and weaker inflationary pressures. The employment dynamics are less pronounced in Europe. This explains why consumers’ spending net of inflation has fallen in the euro area, and why European Central Bank President Christine Lagarde’s advisors remain silent.

Read more by Enrico Colombatto

The U.S. is subsidizing clean energy. What about the EU?

Paying the sustainability bill with inflation

Scenarios

The U.S. Federal Reserve is about to enter a period of declining inflation during which nominal wage rates are likely to catch up with previous levels, and real interest rates slowly move out of negative territory. If Federal Reserve Chair Jerome Powell has learned from his past mistakes, his frequent references to the U.S. tight labor market and PCE inflation should not be taken too seriously. They are not harbingers of measures to cool off demand, but merely serve to warn producers not to expect new waves of easy credit to compensate for lower operational margins.

In Europe, energy prices are declining, and a recession appears to have been averted. The 2023 performance for the European Union should be fractionally better than anticipated, and labor markets are not overly tight. At the end of 2022, the unemployment rate was 6.1 percent. Like in the U.S., in the short run, the main concern seems to deflect pressure from those who would like easy credit, and this explains Ms. Lagarde’s emphasis on the disappointing data about core inflation.

In contrast with the U.S., however, the precarious budgetary situation of some key euro members – the debt-to-GDP ratio is well above 100 percent in Italy, Spain and France – remains a matter of concern for Frankfurt. Inflation lowered the debt-to-GDP ratio slightly in the euro area, from 98 percent in June 2021 to 94 percent in June 2022. However, the recent rise in interest rates is about to reverse that trend. Some governments will certainly explore ways of getting cheap credit and persuade the European Central Bank to meet their requests.

It is unlikely that the ECB will resort to money printing. Public opinion would not accept a new wave of unexpected inflation and other solutions are needed. Ms. Lagarde has not revealed how she intends to deal with the public finance issue. For instance, the ECB could introduce additional banking regulation that encourages commercial banks to buy government bonds with a possible bailout guarantee for the buyers, so as to make it easier for them to collect liquidity. If this happens, European inflation will be tamed, but at the cost of an ever more sclerotized financial system.