Growth after the lockdown

The economic consequences of the coronavirus mostly derive from lockdowns. The shock of the pandemic has kept people from spending – but saving now is only spending put off for another day. Policies intended to discourage that saving could backfire.

In a nutshell

- The economic crisis is a supply-side problem

- Taking on more debt to boost spending won’t solve it

- Depleting savings could lead to much more trouble later

This report is part of a GIS series on the consequences of the Covid-19 coronavirus crisis. It looks beyond the pandemic’s short-term impact, instead examining the strategic geopolitical and economic effects that will inevitably be felt further in the future.

The world economy was not in great shape before Covid-19 struck. With the partial exception of some Asian countries, where the official statistics on growth are not always reliable, investments and productivity have generally been disappointing for many years, despite shamelessly low (and heavily manipulated) interest rates (like in the West and Japan). However, with the benefit of hindsight and despite much drumbeating, the economic impact of the virus has been limited.

Although the coronavirus may have appeared earlier than the first recorded cases in November 2019, its economic consequences became significant only after most countries reacted to the threat by imposing lockdowns. While in January 2020 the International Monetary Fund was predicting global economic growth at about 3.3 percent for 2020 (it was about 2.9 percent in 2019), the revised data at the end of June predicted a global contraction of 4.9 percent and a particularly sharp drop of -8 percent in advanced economies.

Facts & figures

Supply-side problem

The measures forced the partial or complete shutdown of various economic activities for some two months, with widespread consequences. Production plants that closed could not supply other factories, whose output also dropped sharply. This is the supply-chain problem. Production has not and will not rebound immediately after the lockdown, but only gradually and at a cost. Producers will have to consider the new structure of demand. Adjusting to the changed characteristics of the market will be expensive and certainly require new investments. Recent regulatory measures – think of the new health standards in the workplace – will be costly and take time to implement.

The lockdown crisis has been a supply-side problem: by definition, if production drops, growth rates turn negative.

So, the lockdown crisis has been a supply-side problem: by definition, if production drops, growth rates turn negative. Demand also drops, since the labor force is unemployed. The returns on investments are lower and asset owners – including retired people and bondholders – may suffer capital losses (companies go bankrupt).

However, demand falls because producers stop or cut production and thus fail to remunerate the owners of the production factors. In other words, negative shocks (such as lockdowns) hit production. The blow affects people’s purchasing power and the statistics understandably register a drop in consumption.

Saving for a rainy day

There is also another effect: negative shocks are usually scary, especially when there is a chance they can come back. Individuals worry more and more about their future and react by redistributing their purchasing power over time. Hence, they reduce their current consumption and save money to prepare for future unpleasant surprises.

The media usually describe this phenomenon as if people had reduced their willingness to spend. This is misleading. Individuals are always eager to improve their well-being. A crisis, however, ensures that they prefer to preserve their future purchasing power in case of a future negative shock to their incomes. By pouring scorn on those who restrain current consumption, commentators criticize those preparing for the next shock and build up reserves for future consumption.

Of course, the depth of the drop in consumption indicates how little people saved in the past. And the lower the savings inherited from the past, the more urgent the need to build up adequate reserves to avoid a similar mistake in the future. The Covid lockdown therefore teaches us two lessons. Lesson one is that a lockdown is a blow for production. Lesson two is that the less people have saved, the deeper they will fall into debt and the worse the economic setback will be.

Tax on the future

In response to the crisis, authorities have generally resorted to printing money and taking on public debt. These go hand in hand when the monetary authorities buy treasury bills issued by governments. From this perspective, three points deserve attention.

First, going further into public debt is a very poor substitute for lost production: treasury bills are hardly a replacement for cars, furniture or tourism. Second, in most cases, new debt does not originate from an attempt to reduce tax pressure and help healthy companies to bounce back quickly and shoulder the cost of adjusting to the new post-pandemic requirements. Instead, it has been an instrument aimed at boosting private consumption and public expenditure.

In other words, while individuals have cut consumption to match their weaker purchasing power, rebuild their stock of wealth and increase their savings, the authorities are urging them to do the opposite. Today’s new debt is actually a tax on future incomes and purchasing power.

Easy credit does not discriminate between good companies, which do not need it, and bad companies, which do not deserve it.

Third, easy credit does not discriminate between good companies, which do not need it, and bad companies, which do not deserve it. However, it prevents poorly run companies from going belly up, and thus denies successful companies an opportunity to recover and new companies a chance to gain footing. When this phenomenon is particularly intense, an economy cannot absorb the unemployment created by the lockdown.

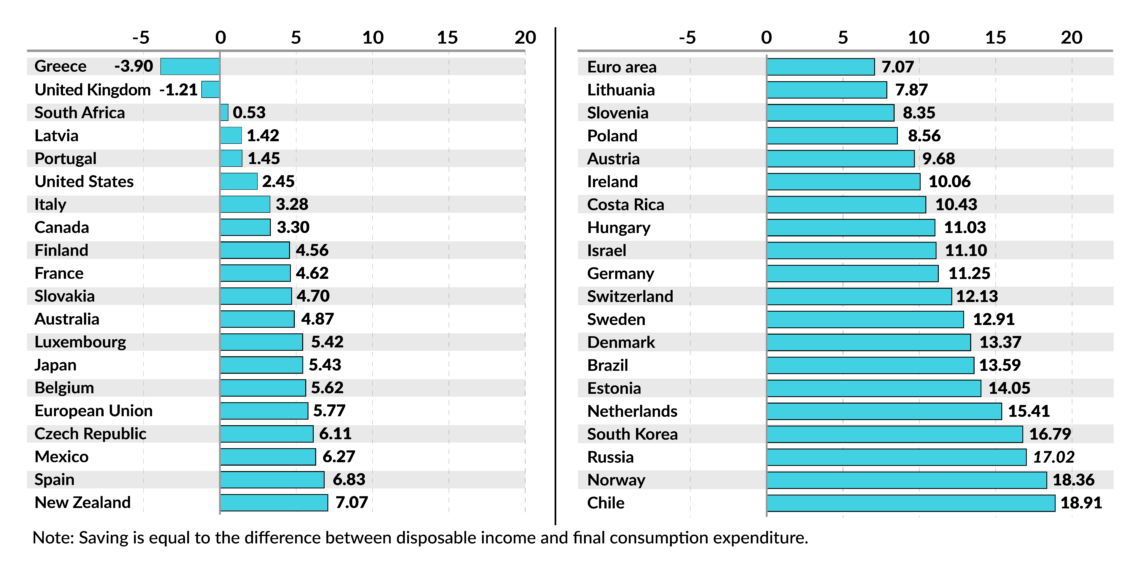

The upshot is that the spring 2020 lockdown has offered an excuse to increase public spending and hand out electoral favors to a wide range of interest groups. On the other hand, the effect of such policies on consumption is questionable. For example, while the average personal savings rate over the past 10 years in the United States was between 7 and 8 percent, it soared to 23 percent in March-May 2020.

This means that by engaging in easy credit, subsidies and public spending, governments have slammed the brakes on future growth. Boosting financial asset values (Wall Street), saddling individuals with more future taxation, raising the cost of entry for innovative producers and strengthening interest groups – including state bureaucracies – are not ways to ensure prosperity in the years to come.

Rude awakening

It is hard to tell what will come next. We do not know whether other waves of the pandemic are on the way or whether governments will implement lockdowns again – and, if so, for how long. We also do not know how individuals will react. For example, the spring 2020 lockdown has clearly shown that in many countries, large portions of the population had put too much trust in the welfare state as a general insurer against adversity, and thus engaged in excessive consumption (tax authorities tend to punish savings and wealth). When adverse circumstances struck, such people woke up with inadequate financial reserves and little government assistance.

Even under the most optimistic scenarios, the rise in consumption will be slowed by a rising propensity to save.

The overall framework has not changed. Individuals are even more vulnerable, since the spring lockdown has eroded whatever people had put aside, and governments cannot count on much fiscal firepower. Thus, a second blow could quickly unleash violence, probably in the name of unfair wealth distribution. Certainly, new debts, more easy money or sophisticated regulation will hardly be the way out.

Scenarios

Those who believe that everything will be all right because governments are supporting aggregate demand and that aggregate demand will soon recover are wrong on several accounts.

First, the lockdowns have hit supply, not demand. Second, even under the most optimistic scenarios, the rise in consumption will be slowed by a rising propensity to save, regardless of how severely and perversely the taxman will discourage people from doing so.

Third, the rising propensity to save will lead to lower living standards, to which governments will have no answer and no solutions. Finally, larger savings will not be enough to meet future people’s needs unless producers are willing and able to increase their future supply of goods and services.

That is not impossible. Yet, it requires greater investments and higher productivity. Regrettably, the current trend is to exploit all events to expand government intervention – in the form of public expenditure and regulation. Policymakers are blind to what growth requires and what it takes to face an emergency.