Qatar builds up its gas muscle

Today’s plentiful supply of natural gas is expected to turn into tight global markets by the mid-2020s. Qatar, a liquefied natural gas export powerhouse, will be ready for that phase with new production capacities. If the emirate also begins to offer flexible terms to customers, the repercussions on global LNG markets could be significant.

In a nutshell

- Qatar became a gas exporter in 1997 with the start of LNG shipments

- Two decades later, it exported 60 percent of its gas output as LNG

- The emirate aims to increase output capacity by nearly a third by 2024 to retain its market position

Qatar has been an outlier on several fronts compared to its Middle East neighbors. Capitalizing on its natural gas reserves is one of them. Although the Middle East holds 41 percent of the world’s proven gas reserves, it accounts for only 18 percent of global natural gas production. In the region, just two countries – Qatar and Oman – are net exporters, of which only Qatar is significant worldwide. Oman’s gas reserves, production and exports are only a fraction of Qatar’s. Excluding Qatar, the Middle East is a net gas importer; with it, the region is the largest liquified natural gas (LNG) exporter in the world. Qatar is an LNG powerhouse, holding one-fifth of global gas liquefaction capacity.

Following several years of a self-imposed moratorium, Qatar has recently announced significant LNG expansion plans, setting the stage for a major shift in the outlook for LNG markets. If all goes according to plan, Qatari LNG will hit the market at the right time, when tightness is most expected. However, growing competition is forcing Qatar to rethink its practice.

Facts & figures

Qatar, gas facts

- Almost three-quarters of Middle East gas reserves are in Iran (42%) and Qatar (32%)

- Qatar’s domestic consumption more than tripled between 2004 and 2017, while production quadrupled over the same period

- Since Qatar began shipping LNG in 1997, a total of 14 liquefaction trains have begun operations in the country

- Qatar is at the forefront of GTL technology, which processes natural gas into diesel, naphtha and lubricants. Pearl GTL, a joint development by Qatar Petroleum and Shell, is the world’s largest GTL facility

- Qatar and the U.S. could together account for some 40% of all global LNG exports by 2040

Source: BP 2018 and 2019; GIIGNL 2018

Gas-rich

Endowed with the third-biggest gas reserves in the world after Russia and Iran, Qatar is the largest Middle Eastern gas producer after Iran, accounting for 5 percent of global production in 2017, according to the BP Statistical Review of World Energy. With a population of just 2.6 million inhabitants, the country looks mostly to international markets to sell its gas.

With a geographical location well-suited to serve any coastal market in the world, Qatar ships 60 percent of its production as LNG. A further 10 percent is exported via the Dolphin pipeline to the United Arab Emirates (UAE) and Oman. Of the country’s remaining output, about 3 percent is shipped internationally in the form of gas-to-liquids (GTL) products, with the rest consumed locally.

The two countries have recently explored collaboration on the development of the jointly owned field.

Although domestic gas consumption has been rising rapidly, it still accounts for just above a quarter of the gas, Qatar produces, leaving the bulk of domestic output for exports. This is a key difference with most other Middle Eastern countries, where gas production is fully absorbed locally.

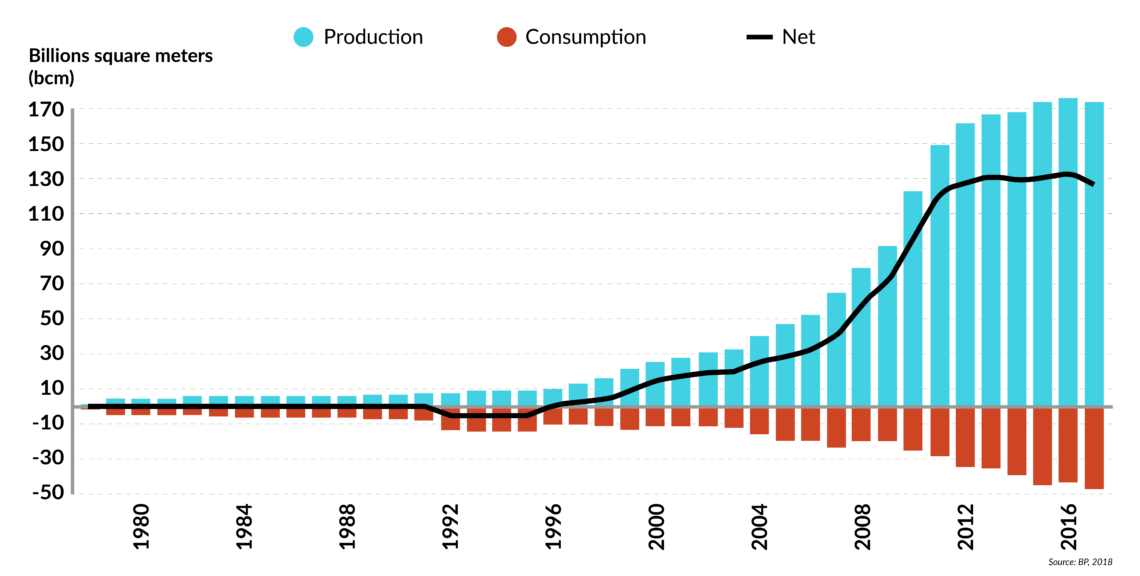

Facts & figures

Qatar: natural gas production and consumption

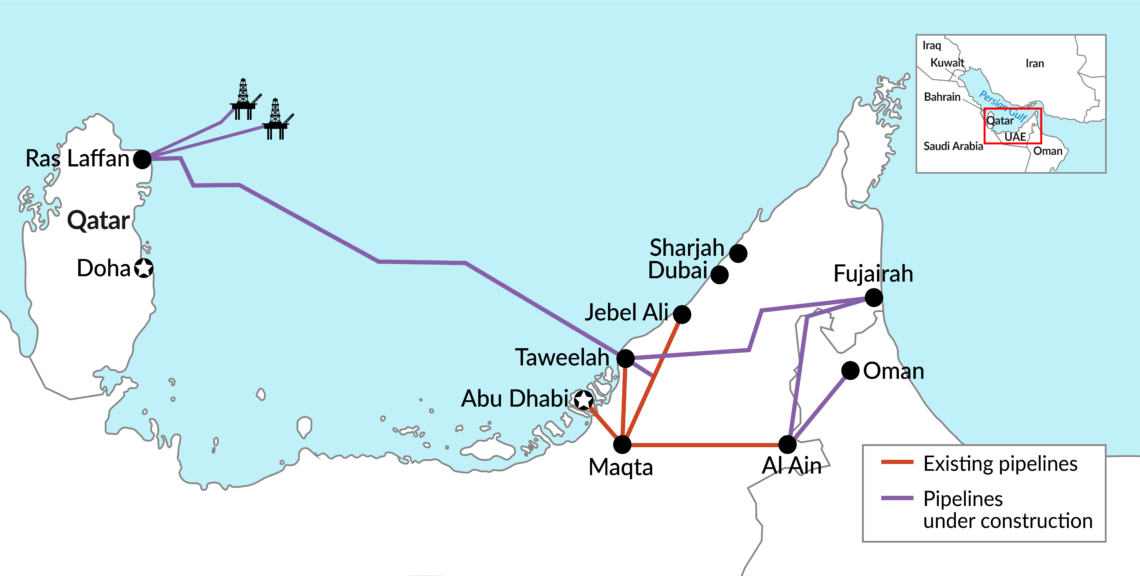

Qatar became a gas exporter in 1997 with the start of LNG shipments. Twenty years later, it exported 60 percent of its production as LNG. Pipeline exports commenced in 2007 and accounted for 10 percent of production in 2017, according to BP. The Dolphin project is the only significant intra-regional gas pipeline; most (90 percent) of the pipeline’s capacity is directed to the UAE, with the rest going to Oman.

Giant field

Most of Qatar’s gas production comes from the giant North Field, which is the world’s largest natural gas field, accounting for approximately 10 percent of proven global reserves, according to Qatar Petroleum. The field extends into Iranian offshore waters, where it is called South Pars. The two countries have recently explored collaboration on the development of the jointly owned field. Only a few years ago, they had clashed over divergent claims, with Iran asserting that one-third of Qatar’s North Field gas reservoir lay under Iranian waters. Although the issue has since been resolved, Qatar’s side of the field is far more developed than Iran’s. This has caused frustration in Tehran, where perceived “excessive” Qatari extraction has been condemned.

Worried about possible reservoir damage, Qatar imposed a moratorium on new projects in the North Field in 2005. This step was intended to allow time for experts to study the impact of rapid output increases on the reservoir. Initially scheduled to end in 2008, the moratorium was extended until 2017, when Qatar announced it would be lifted in conjunction with plans to increase liquefaction capacity. The decision clears the way for a robust increase in production and LNG exports, with significant long-term repercussions on global markets.

Facts & figures

Dolphin gas project

Major decision

The lifting of the moratorium coincided with two developments. Firstly, it came just as Iran revealed that it had reached a deal with France’s Total S.A. to expand production capacity at the South Pars field. Iran’s plans, however, have not made much progress after the United States withdrew from the nuclear deal with Iran and reimposed economic sanctions.

Secondly, the LNG market has become more competitive. A tidal wave of LNG investments was approved between 2009 and 2014 and these facilities are coming on stream now. The expansion has been led by Australia, where projects such as Australia Pacific LNG, Gorgon and Wheatstone became operational in 2017. Australia has been Qatar’s closest competitor. In November 2018, for the first time, Australia overtook Qatar as the world’s largest exporter of LNG.

Recognizing these threats, Qatar aims to increase its gas production by at least 30 percent through 2024.

For both countries, geographical proximity makes Asia the primary export market. Virtually all Australian and 67 percent of Qatari LNG was shipped to Asian customers in 2017, according to BP. Furthermore, with much of Asian gas demand growth centered in China, both Australia and Qatar see that country as their key outlet for expanding LNG production capacity. In 2017, 45 percent of China’s LNG imports originated from Australia and a further 20 percent from Qatar.

In North America, the shale revolution has boosted U.S. gas production well above the country’s domestic needs, creating a significant export surplus. According to the International Energy Agency (IEA), global LNG capacity will expand by 20 percent between 2018 and 2020, with the U.S. providing about half of this growth. Additionally, the flexibility of conditions under which U.S. LNG cargoes are traded allows the Americans to compete with established exporters in all their markets.

Recognizing these potential threats, Qatar aims to increase its gas production by at least 30 percent through 2024, according to the Gas Exporting Countries Forum. The IEA projects an increase of 50 percent between 2017 and 2040. This additional gas is mostly targeted for export, enabling Qatar to remain one of the world’s largest LNG exporters. The country’s decision to leave OPEC as of January 2019 was justified in part by a desire to refocus on natural gas. The other reason is a falling out with its Gulf Cooperation Council (GCC) neighbors.

Qatar has been blacklisted by other GCC countries, particularly Saudi Arabia, Bahrain and the UAE in addition to Egypt, which cut all ties with the small emirate in 2017, accusing Qatar of destabilizing the region and supporting radical Islam. The resulting land, air and sea blockade imposed on Qatar was the culmination of years of tensions between the gas-rich state and its Arab fellows.

Some feared that Qatar would retaliate by using gas as a weapon, primarily by cutting its supplies to the UAE through the Dolphin project. Doha, however, has not followed Moscow’s example with Ukraine. By respecting existing arrangements, Qatar has reinforced its reputation as a reliable supplier and boosted its appeal to existing and potential customers.

Scenarios

While the overall trend is toward an expansion of LNG trade, the industry typically goes through cycles of feast and famine, making supply rather lumpy. LNG projects have a slow pace of development because of the scale of investment. This explains why additional capacities come in waves, bringing new supplies to the market every couple of years. Between one wave and the next, however, the market tightens. The lumpiness of investments means that global LNG markets are expected to tighten in the mid-2020s if no additional capacity comes on stream.

This is where Qatar’s role looms large. Its planned expansion of production capacity is expected to hit the market in the mid-2020s, thereby alleviating potential market pressure and reemphasizing Qatar’s central role in global LNG. Under increasingly competitive conditions, however, there is a need for cost competitiveness as well as the flexibility to divert cargoes to higher-priced markets as and when they emerge. Qatar is well-positioned in terms of production costs and should have the ability to undercut rival projects if it wishes. Yet an outright price war is unlikely to be in Qatar’s interest, since it would undermine the overall profitability of its output.

Furthermore, most of Qatari LNG is sold under long-term, oil-indexed contracts, denying it the flexibility that is increasingly desirable in markets where the demand outlook is uncertain. In this respect, U.S. LNG, though slightly disadvantaged to Qatar’s in terms of cost, scores high, since it is traded on a spot or short-term basis. Qatar will be forced to rethink its existing LNG strategy, primarily in terms of increasing the use of spot and short-term contract sales, if it is to safeguard its position in the longer term.