The U.S.-China tug-of-war over chips and capital

The U.S. and China are wrangling over Western investment into chips and other advanced technologies, with the long-term consequences of U.S. controls uncertain.

In a nutshell

- Several factors are driving foreign investment away from China

- U.S. policies to stunt Chinese tech growth face implementation challenges

- The Biden White House is determined to follow through

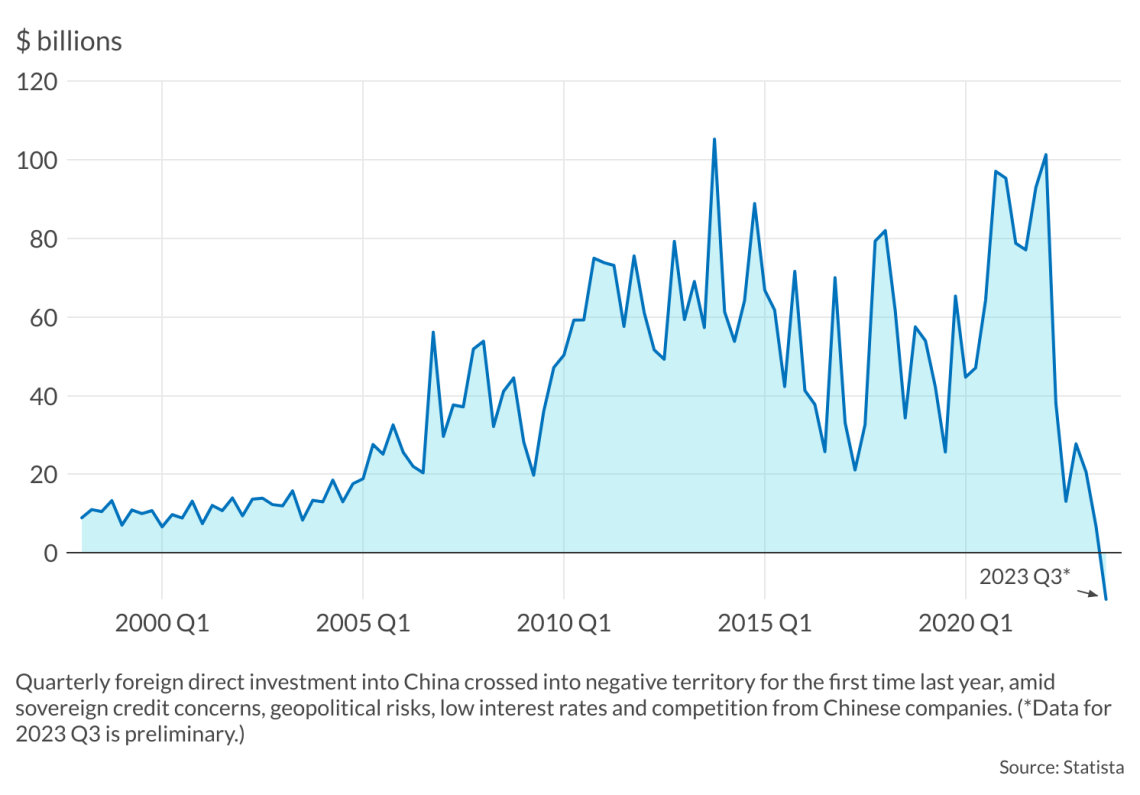

For the first time since records began in 1998, the third quarter of 2023 saw more foreign direct investment (FDI) flowing out of China than in. The official figure was -$11.8 billion. Foreign companies withdrew profits from China for six consecutive quarters through the end of September 2023, totaling more than $160 billion in outflows. The decline in China’s FDI is a symptom of the country’s economic downturn. At the same time, a struggle continues between Chinese leader Xi Jinping and American President Joe Biden over harnessing the flow of Western capital.

China faces several structural economic problems that are becoming increasingly salient, including high local government debt, a sluggish and partly bankrupt real estate market, low consumer confidence and high youth unemployment. The Biden administration announced in August 2023 that it would limit U.S. capital investment in China’s sensitive technology sector, extending the competition between the two powers into the arena of investment controls.

In view of geopolitical tensions and the current Chinese downturn, Moody’s rating agency lowered its outlook for China’s credit from stable to negative, while maintaining its A1 investment-grade rating on the country (which has not changed since 2017). Foreign companies in China have withdrawn earnings or downsized accordingly, and the Wall Street financial community has also changed its tune, no longer singing Beijing’s praises.

Explaining the FDI flight

Responding to Moody’s decision, China’s Ministry of Finance said it was “disappointed” and called the agency’s concerns “unfounded.” It argued that the country’s real estate and fiscal problems were “manageable,” and that the government was working to “deepen reforms and address risks and challenges.”

A closer look at the phenomenon of foreign capital withdrawal and the FDI slump in China reveals several developments.

Sean Stein, president of the American Chamber of Commerce in Shanghai, recently spoke about the pressures on American companies coming from the Chinese side. The U.S. political community often discusses strategic competition with China around the four dimensions of military, economic, technology and political values. But, he argued, the biggest pressure on American firms is a fifth dimension: the tough competition presented by Chinese companies.

“China’s small and medium-sized enterprises … with their clouds of smart employees working late nights and overtime, can affect U.S. companies’ business at any time,” Mr. Stein said. “Chinese companies are faster than U.S. companies in responding to the market, they are better at using digital strategies, they can quickly adapt and use emerging technologies, they are better at marketing and they are better at applying for license permits.” Competing against Chinese electric vehicles, even the vaunted Tesla might someday face threats to its survival.

A second factor driving out foreign capital is China’s revised Anti-Espionage Law, which came into effect in July 2023. The policy expanded the definition of espionage and prohibits the transfer of “information related to national security and interests.” This ambiguous provision led some foreign executives to worry that certain business activities and topics of conversation in China may become off-limits. Even Moody’s advised its Chinese employees to work from home after making the rating change, and its Hong Kong analysts were warned against traveling to the mainland for fear of possible retaliation by Chinese authorities. U.S. pollster Gallup has decided to pull out of the country because of the law.

With current interest rates in China much lower than in most of the world, foreign companies are not reinvesting the profits they have made in the country, but are rather remitting them elsewhere where they can earn a higher return. Furthermore, companies are increasingly shifting investments from China to other countries to diversify against intensifying geopolitical risks.

Offering another perspective, Zhang Jun, professor of economics at the Fudan University, argues that it is no longer appropriate to focus on China’s economy in terms of traditional FDI flows; what matters most is FDI in competitive high-tech areas. While at the beginning of 2023 Fitch Ratings projected that China’s FDI would continue to decline amid weak foreign investor sentiment, FDI in high-tech manufacturing was thought to be more resilient.

The developments in China last year have borne out this forecast. High-tech manufacturing investment has been growing faster than total FDI and total high-tech FDI since 2021, and remained resilient in 2023 – up 25.3 percent year-on-year in the first half of the year, following 49.6 percent annual growth in 2022. Whether this situation is sustainable, however, is unclear.

Chinese response

In some ways, this argument reflects President Xi’s economic goals: China is trying to retain foreign capital generally, but FDI in high-tech is more relevant. After Beijing recognized the scale of the FDI problem last year, Mr. Xi and his government made a heavy-handed statement to foreign business leaders, promising to improve mechanisms for protecting the rights and interests of foreign investors. This turned out to be just lip service.

Mr. Xi has rather focused on FDI in high-tech areas. His notion of “high-quality development” means relying on the country’s own innovation but also on foreign technology and capital, so that China can take the lead in the fourth industrial revolution (which includes artificial intelligence, life sciences, industrial materials and renewable energy). The key to this revolution is advanced microchips.

The Chinese leader’s trip to the U.S. in October was not so much about easing relations with Washington as about competing for U.S. capital, especially capital related to chip production. Beijing understands that the U.S. is not a monolith, but a system sensitive to many different interest groups. China hopes to use the conflict within the American business community, especially among chip companies, to mitigate the Biden administration’s ban. In arranging President Xi’s schedule during his stay in San Francisco, Chinese officials initially requested that a planned dinner with business executives be held before the Biden-Xi meeting, a clear indication of their real priorities. Of course, the White House rejected this request.

President Xi’s advisors had prepared three versions of his speech for the dinner with business leaders; after the meeting with President Biden unfolded, Mr. Xi picked the friendliest version of his remarks. In a 30-minute address to top executives, he declared that China wants to be a “partner and friend” of the United States. But even then, the effect appeared to be limited.

Biden’s challenges

The world’s top five chip manufacturing equipment vendors received more than 40 percent of their revenue from Chinese customers in the third quarter of 2023. California-based Lam Research drew nearly half of its revenue from China. According to Nikkei Asia, the Chinese market contributed 62 percent, 27 percent, 22 percent and 18 percent of last year’s revenue for Qualcomm, Intel, Tesla and Apple, respectively.

This data shows clearly why U.S. chip companies are trying so hard to retain the Chinese market. Nvidia chief executive Jensen Huang said in Singapore on December 6 that the firm is cooperating with U.S. government regulators to remain in compliance while providing alternate, less powerful AI chips to Chinese customers, which are set to be marketed this year. Even if the claims of cooperation are exaggerated, the company’s ambition to win Chinese business is genuine. Nvidia accounts for over 90 percent of China’s AI chip market, according to Reuters, and before the export controls relied on China for about a fifth of its revenue. But the company’s attempt to abide by U.S. restrictions while offering lower-level chips to meet Chinese demand will likely not satisfy the ambition of China’s AI industry.

Read more by Junhua Zhang

The Gordian Knot of China’s EV subsidies

Intel CEO Pat Kissinger is also increasing pressure on the Biden administration, claiming that the government risks jeopardizing one of the administration’s key policies of bringing chip production “back to the U.S.” Without orders from Chinese customers, he warned, Intel will have less reason to advance planned factories in Ohio and other domestic projects.

Last July, the U.S. Semiconductor Industry Association released a statement calling on the White House to not impose more semiconductor export restrictions on China – arguing that it could weaken the competitiveness of the American semiconductor industry, disrupt the supply chain and jeopardize the government’s massive new investment in domestic chip manufacturing.

Companies in other countries have also been eager to break or work around the controls. Japan’s Nikon is considering tapping into mainland China’s chip lithography market to expand its current global market share of 7 percent, which ranks third.

Nevertheless, the Biden administration seems to be determined to ban China’s advanced chip exports and investments, even if enforcement will not be easy.

“High-quality development”

The U.S.-China Economic and Security Review Commission (USCC), authorized by the U.S. Congress, acknowledged in a recent report that American controls on Chinese exports of advanced chip equipment have not fully worked. There are still loopholes around the policy.

The ban has certainly caused a lot of trouble for China. But the White House seems to be quite busy trying to close these loopholes to make the policy effective. In this tug-of-war for U.S. chip capital, Commerce Secretary Gina Raimondo has repeatedly warned American companies (especially Nvidia and Intel) not to sell AI-enabled chips to China in the name of national security. But the question of whose arm will ultimately be twisted – that of chip capital or the U.S. government – is so far unanswered.

In the face of China’s myriad economic problems, President Xi is banking on what he calls “high-quality development” rather than political and institutional reform. During his recent visit to Shanghai, Mr. Xi rehashed his so-called “reform and opening up” platform, but he has never really acted on that promise. For Mr. Xi, “reform” has become history.

China hopes to use the conflict within the American business community, especially among chip companies, to mitigate the Biden administration’s ban.

The prominent Chinese sociologist Sun Liping has warned that if the Chinese Communist Party (CCP) does not carry out deep political reforms within some five years – including on issues such as separating the party from the government, establishing the authority of the courts and freedom of speech, publication and press – the consequences will be unimaginable. Noted economist Wu Jinglian recently made a similar statement.

There is no sign that Xi Jinping will listen to such voices. Instead, he is determined to realize his own concept of high-quality development – which requires a push for Western capital, especially American capital in the chip industry. This is a last shot at his “Chinese dream.” It remains to be seen whether this approach will repeat the mistakes of his Made in China 2025 campaign. The CCP is not only competing with the U.S. for capital, but also racing against time.

Scenarios

There are two possible outcomes to this tug-of-war.

Less likely: Circumvention

Under one scenario, U.S. chip capital insists on evading Washington’s restrictions, providing strong conditions for Chinese high-tech development while maintaining their own corporate profits. At the same time, with China’s own research and development (R&D) capabilities, China might be able to take five or 10 years to surpass the U.S. in areas like artificial intelligence, and indeed play a pivotal role in the Fourth Industrial Revolution. It would also use this success to alleviate its own economic problems. Bearing in mind the warnings of Professor Sun Liping on China’s institutional and political challenges, this scenario today does not look especially likely, due to the U.S. government’s determination to limit chips and high-tech investments.

More likely: Slowing economy

Alternatively, the U.S. government is largely able to keep chip capital from circumventing the China controls, creating other markets in India, Southeast Asia and elsewhere. Meanwhile, China’s own R&D capabilities seem to reach their limits, precisely because of an incapacity in producing high-value chips – such that President Xi’s “high-quality development” plan will largely not be realized. This might force Beijing to make some concessions on political reforms. In the long run, China risks falling into the “middle-income trap.”

For industry-specific scenarios and bespoke geopolitical intelligence, contact us and we will provide you with more information about our advisory services.

Sign up for our newsletter

Receive insights from our experts every week in your inbox.