Peak China

China’s military buildup and drive for economic self-sufficiency are signs that Beijing sees a near-term conflict, likely over Taiwan, as advantageous.

In a nutshell

- China’s declining population and economic slowdown create potential dangers

- Xi Jinping’s grand ambitions include relying less on foreign direct investment

- Beijing’s aggressive moves signal that it may seek to reunify Taiwan by force

The greatest geopolitical misfortunes occur at the intersection of ambition and desperation. In 2023, President Xi Jinping’s China is governed by both. This has heightened the risk of Chinese Communist Party (CCP) bellicosity and the prospect of war in the Indo-Pacific, most immediately over Taiwan.

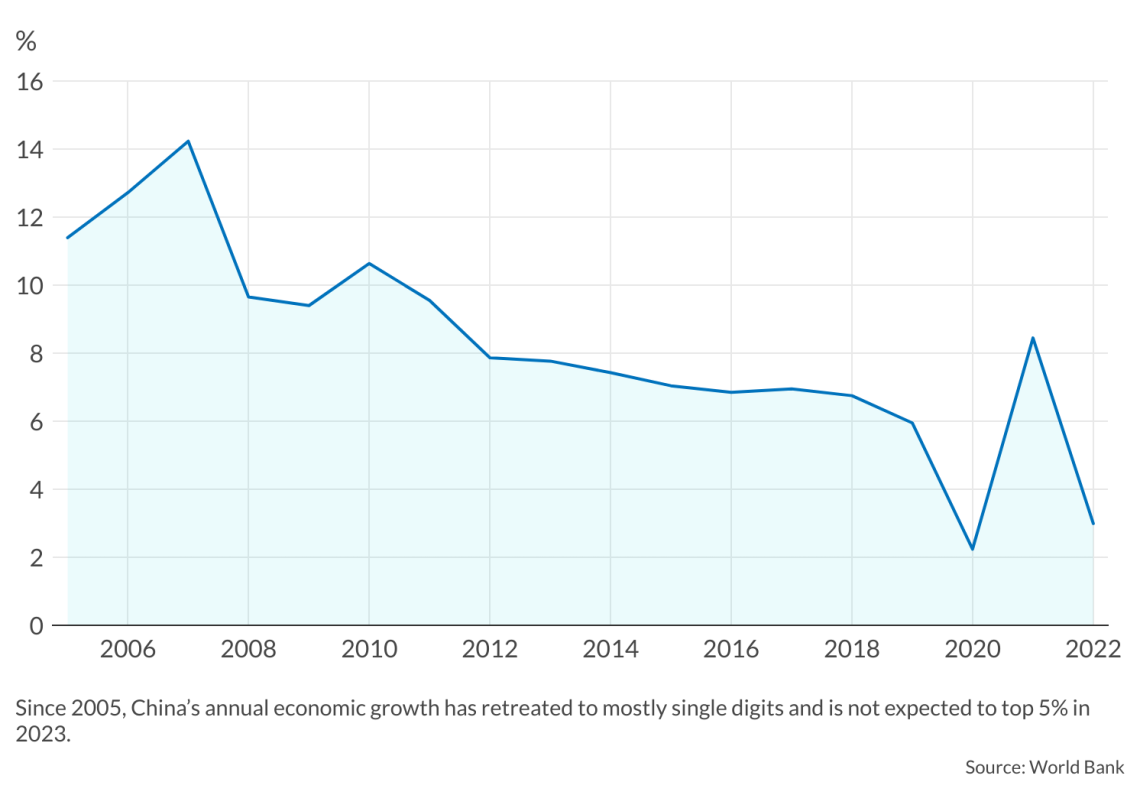

China’s economic growth has been tapering off for more than a decade. Today, this slowdown is compounded by a protracted real estate crunch, shaky local government finances, declining exports, insufficient consumer demand and unprecedented foreign outflows. Meanwhile, China’s demographics have gone from bad to worse, with its population expected to decline throughout the rest of the century.

Its youth unemployment rate is so dire that the CCP has stopped publishing the numbers. At the last measure, the official rate was 21.3 percent – the unofficial rate is now likely higher. The old equation was that Beijing retained legitimacy through prosperity. That has now been rescinded.

Over the last decade, too, President Xi and the CCP have been ratcheting up a new Cold War against the West. The contours of this struggle have been enumerated in party documents and directives. All point to the CCP’s ambition of upending the Westphalian global order and remaking it in accordance with its governance model. This is President Xi’s dream of “national rejuvenation.” It is also what he meant when, at the 19th National Party Congress in October 2017, he said that China is now “moving toward center stage.” As an internal CCP textbook explains, “A new world order is now under construction.”

Since 2013, China’s economic troubles and President Xi’s growing ambitions have prompted Beijing to adopt policies that have now been accelerated. Some of them make conflict more likely, including military modernization and a deliberate economic decoupling from developed global markets. China’s defense increases and upgrades have arguably given the People’s Liberation Army (PLA) a relative military edge over the United States, such as in Indo-Pacific naval power. The economic distancing from the West has allowed China to become comparatively self-sufficient and likely able to withstand the risks of economic isolation or sanctions in a wartime scenario.

A cynical read would suggest Mr. Xi has been preparing China’s current path since he assumed the party chairmanship in 2012. Aware that the old equation would at some point no longer hold, the Chinese leader and the CCP have been laying the foundations for a new equation, in which their legitimacy is derived from forceful actions aimed at realizing China’s national rejuvenation.

Whether President Xi believes conflict could bolster the CCP’s legitimacy, or whether he sees a closing window of opportunity to take Taiwan, is unknown. Yet the status of the PLA’s military preparedness and China’s growing independence, coupled with persistent economic difficulties, could affect President Xi’s calculus. Changing geopolitics could also make the opportunity cost of a delayed conflict too high.

More from Aleksandra Gadzala Tirziu

Rising tensions along the Indian-Chinese border

China, Latin America and the new space race

A giant military buildup to what end?

A country’s military power is often proportionate to its economic strength: more growth and prosperity generally mean more – and more sophisticated – weapons production. The reverse is also true. Yet when China’s growth began to slow more than a decade ago, the CCP made the decision to accelerate its rapid military modernization and buildup. Rather than an economic solution to the downturn, Beijing opted for a military one.

It has since continued to demonstrate a marked reluctance to any kind of large-scale financial stimulus. This is understandable: Healthy private enterprise and consumer welfare are incompatible with the CCP’s Marxist-Leninist philosophy in which state enterprise and objectives are paramount. The party might well try to buttress short-term growth through unproductive output and activity, yet this is unlikely to alter its long-term economic trajectory. China’s annual economic growth is forecast to slow to 3.5 percent by 2030 and to merely 1 percent by 2050 as its population shrinks.

In other words, President Xi and the CCP could soon be unable to finance their war machine at the same scale and scope as they have to date. Mr. Xi could decide that China has reached a point beyond which its ability to manufacture advanced weaponry could be constrained and that its relative comparative advantages are sufficient for its military success.

Between 2015 and 2019, Beijing undertook the largest peacetime military buildup since the 1930s. During this time, the CCP’s military spending grew nearly twice as fast as China’s official gross domestic product (GDP) in real terms. Following a brief downturn in investment at the height of the Covid-19 pandemic in 2020, spending increases appear to have resumed. Official Chinese data points to an annual 7.2 percent defense budget increase in 2023, to $224 billion. Yet official Chinese defense disclosures are narrow in detail and only catalog spending across three categories: personnel, equipment and training and maintenance. The PLA’s entanglement in China’s domestic economy through the CCP’s policy of military-civil fusion further obfuscates the data. Unofficial estimates, including from U.S. intelligence sources, suggest the factual size of Beijing’s defense budget is closer to $700 billion – some $200 billion shy of the U.S. defense budget in nominal terms.

Since 2013, the focus of Beijing’s military investments has been on expeditionary capabilities rather than traditional homeland defense. Most significant has been the PLA’s naval expansion. Sometime between 2015 and 2020, the PLA Navy (PLAN) surpassed its U.S. counterpart in the number of battleforce ships – that is, ships that are counted toward the quoted size of the U.S. Navy. As of July 2023, the PLAN had 340 platforms while the U.S. has 299. The PLAN’s battle force is projected to increase to 400 ships by 2025. According to the U.S. Navy’s Force Design 2045 plan, the U.S. anticipates 373 ships by 2045, including 150 unmanned surface and underwater vehicles.

President Xi could decide to capitalize on this relative advantage and initiate a war; after all, an assault on Taiwan would likely be amphibious. Over the last five years, the PLA Air Force has also increased its production and procurement of advanced aircraft. Its inventory of advanced J-20A stealth fighters is likely to overtake that of the U.S. Air Force this year. In its current state and configuration, the Taiwanese Air Force would be unlikely to repel a Chinese attack. China’s Army Rocket Force has also embarked on a significant nuclear expansion and, in 2022, China launched the most defense-related satellites, outpacing the U.S.

Granted, weapons wielded by the U.S. and its allies remain in many respects superior to those of the PLA. In a conflict scenario, Beijing would then likely attempt to overwhelm quality with quantity. China’s manufacturing is equivalent to that of the U.S. and Europe combined. For the CCP, a wartime manufacturing boon could also have the added benefit of providing needed fiscal stimulus – and one that would not jeopardize its statist economic model. A protracted economic slowdown could, however, minimize this gap and limit such possibilities.

An economic hardening

The Chinese economy is not an island unto itself. It is, however, more self-sufficient than it was even just a few years ago. Part of this is a product of the current economic slowdown, yet much is due to a deliberate CCP policy of decoupling from developed markets globally. In 2013, around the time that China’s economy began to slow and the PLA began its military expansion, President Xi established “Made in China 2025” as China’s official industrial policy. From it, much has followed. A year later, President Xi introduced China’s counter-espionage law – the revised, more stringent version of which came into effect this July.

These policies, among others, have had the effect of decreasing China’s dependence on foreign investment, global markets and external sources of resources and technologies. That means that, today, the CCP has less to lose from assuming a more confrontational stance toward the U.S. and the West.

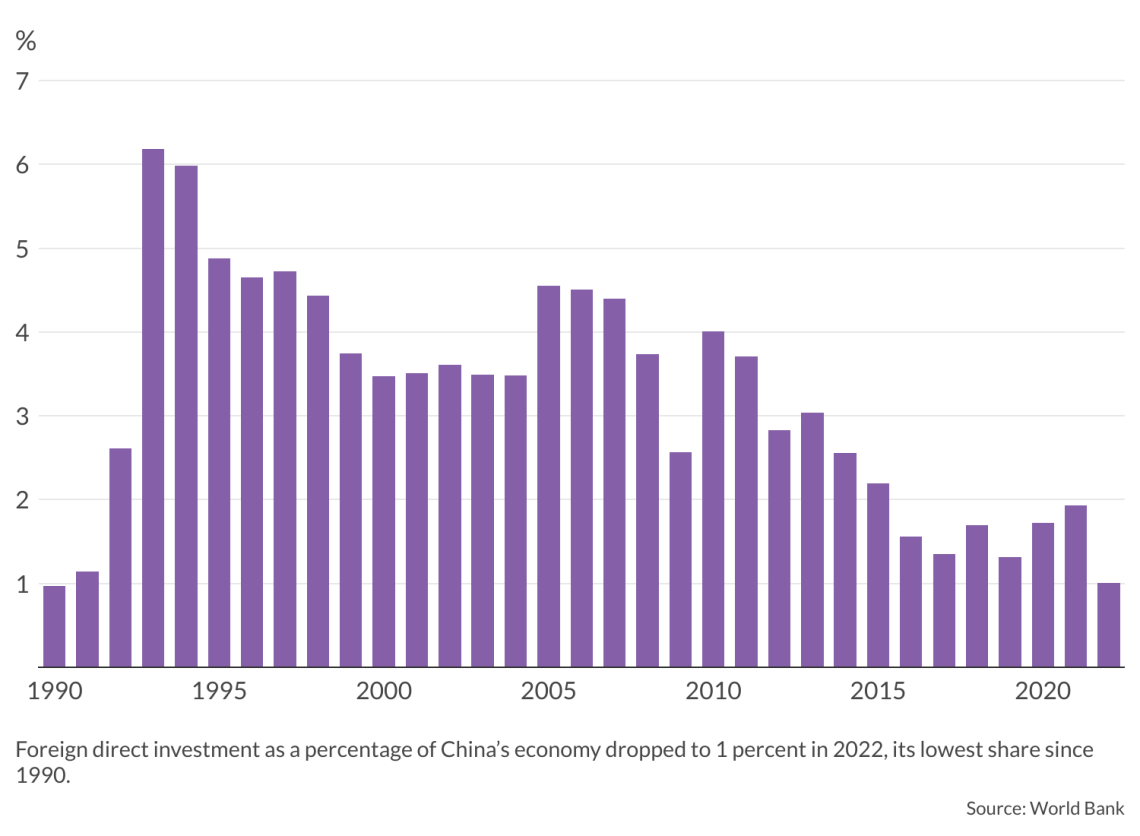

For example, foreign direct investment (FDI) – which had been a key element of China’s growth story, having provided capital, jobs and know-how – accounted for 1 percent of China’s GDP in 2022. In the second quarter of 2023, foreign investment into China declined another 2.7 percent over the same period in 2022, suggesting China’s role as the world’s preferred investment destination is ostensibly over. While this circumstance will likely compound China’s economic crisis, it is also one less dependency the CCP would have to worry about in a conflict scenario. Chinese FDI into the U.S. has also been notably reduced. In 2022, it was the smallest amount since 2009.

For China, developed markets have also become less important on the margins as its trade relations with the Global South have increased. For example, amid a protracted trade slump, Chinese exports to Southeast Asia jumped 24.1 percent between January and April of 2023 from the year-earlier period. Its shipments to Africa and Latin America grew 36.9 percent and 11.2 percent, respectively. The recent expansion of the BRICS bloc of nations to include Saudi Arabia, the United Arab Emirates, Iran, Ethiopia, Egypt and Argentina will also likely increase China-Global South trade. All BRICS countries boast significant trade influence in their respective regions by dint of their membership to regional free trade agreements and trade corridors.

Some of China’s trade with the Global South and BRICS nations is in intermediate goods – countries like Vietnam and Mexico import and assemble Chinese components into finished products to be sold to developed markets. But much of it is not. For example, Chinese exports to Southeast Asia are predominantly in consumer goods. Chinese exports to Russia have grown 153.1 percent since April 2022. The top export item is vehicles.

Beijing’s courtship of emerging markets has also yielded outsized control over global critical minerals supply chains. Today, China controls 60 percent of worldwide critical mineral production and 85 percent of processing capacity. For example, in the Democratic Republic of Congo, Beijing owns 15 of the country’s 17 cobalt mining operations as part of President Xi’s Belt and Road Initiative. In Argentina, which has the world’s second-largest lithium reserves, Chinese companies have exclusive rights to two lithium salt lakes.

No doubt, in wartime Beijing could find itself cut off from these and other overseas production facilities. Yet such a risk is difficult to mitigate as no country retains all the minerals required to sustain an advanced industrial economy. President Xi and the CCP have likely priced this possibility into their calculus. In the event of war, their efforts would then likely orient around denying the U.S. and its allies a competitive advantage. As an ostensible step in that direction, China’s Ministry of Commerce in July imposed export controls on germanium and gallium. Both minerals are critical for modern military systems. Between 2018 and 2021, 53 percent of U.S. gallium imports came from China. As of 2020, China supplied more than 50 percent of its germanium.

The risks of biding time

It is unclear for how long such favorable circumstances might last. In June 2022, the U.S. and key allies including India, Japan, South Korea and the European Union established the Minerals Security Partnership to develop and secure critical mineral supply chains. In part as a response to increased CCP bellicosity, too, countries in the Indo-Pacific have begun to strengthen their military capabilities and coordination efforts.

For example, Japan has broken with decades of pacifism to assume a more assertive military posture. Its new national security and defense strategies call for an unprecedented defense buildup that includes a 60 percent defense budget increase by 2027. If realized, that would put Tokyo’s annual defense budget third in line after Beijing and Washington. Tokyo’s recently appointed defense minister is a pro-Taiwan politician. South Korea, too, has also recently emerged as a militarily capable ally.

In September, Vietnam upgraded its relationship with Washington to a “comprehensive strategic partnership” – the same designation it uses for its ties with China, Russia, India and South Korea. The classification bears notable economic implications and also opens the door to likely military cooperation. Australia, the U.S. and Indonesia are now cooperating militarily. The U.S. and the Philippines are again strengthening their military ties after a period of strained diplomacy. Manila and Washington have signed agreements that will lead to the largest American military presence in the Philippines in 30 years. All the while, India has become globally resurgent and Europe increasingly skeptical of China’s economic forays. Across the Taiwan Strait, too, the Democratic Progressive Party appears poised to secure a third consecutive electoral victory in January.

For President Xi and the CCP, these developments are unlikely to present a near-term risk. Yet President Xi might conclude that they could evolve in a manner that would render the CCP’s envisioned “new world order” more difficult to establish. Over time, China’s current relative advantages could erode, closing the window of opportunity.

Scenarios

At a top-level national security meeting in May, President Xi advised his team to “be prepared for worst-case and extreme scenarios.” On a visit to the PLA’s 78th Group Army in September, he called for “combat readiness.”

More likely: China starts a conflict soon

The likely consideration, then, is when and not if Beijing initiates a conflict, such as a forced reunification with Taiwan, to seize its advantages. Predicting an exact time is a fool’s errand. Still, all major indicators suggest a near-term conflict would be on the margins less risky for China than a delay. It would be prudent for the West to prepare for increased risk.

Less likely: Beijing rejects military confrontation

There is a chance that President Xi and the CCP might assess the risk of confrontation with an eventual U.S.-led global coalition to be too high. After all, the party’s legitimacy would suffer from a military defeat. In this less likely scenario, the CCP would then likely persist with its gray zone activities against Taiwan and the West. Yet Beijing has pursued such tactics for more than a decade. So far, they have not yielded the desired results. History has also shown that national leaders are not always risk-averse, or their assessments of risk follow a different logic. President Xi has been laying the groundwork to bring Taiwan back under the mainland’s control since 2013 and he may see no more reasons to wait.

For industry-specific scenarios and bespoke geopolitical intelligence, contact us and we will provide you with more information about our advisory services.

Sign up for our newsletter

Receive insights from our experts every week in your inbox.