Squaring the circle of the EU’s fiscal rules

The European Union’s fiscal rules have been inactive for years. While reforms have been proposed, their success is yet to be seen.

In a nutshell

- The EU’s budgetary policies have failed its 27 member nations

- New rules are being considered but will likely never be enforced

- Ultimately, fiscal discipline will be up to national governments

For more than three years now, all the basic rules of budgetary responsibility in the European Union have been effectively switched off.

In March 2020, at the beginning of the Covid-19 pandemic, the EU activated the so-called general escape clause from the application of budgetary rules. But let us not be fooled. It has been years since the basic canons of responsible fiscal management have been applied and enforced. And, at least until the end of this year, nothing will change.

Right now, the question is what happens next. What kind of fiscal rules will we wake up to on January 1, 2024? Will we return to the existing rules or create new ones?

For an unprecedentedly long period of time, all the common European principles of sound fiscal policy have been virtually nonexistent, and yet there is no major political debate about it. No one is criticizing their switch-off and calling for a return to responsibility, and the fact that many of the more enlightened commentators have not even noticed the shift says a lot about the budgetary rules themselves. They were soft from the start and have been further softened by long-term use. Why?

First, a bit of history. As I have explained elsewhere, at the beginning of deeper European economic and monetary integration, the prospective members of the single European currency area adopted a set of principles designed to curb the budgetary profligacy and irresponsibility of national politicians. Discipline was supposed to be ensured by upper limits on annual public budget deficits (3 percent) and maximum levels of public debt (60 percent). It was also stipulated that a country exceeding these levels for at least three consecutive years must make corrections and could be fined up to 0.5 percent of gross domestic product (GDP). These relatively simple rules were laid out in 1997 and have been fully operational since 1999, the year the euro was launched. They are called the Stability and Growth Pact and are an integral part of the European legal order.

Their main purpose was to ensure the dominance of monetary policy: a situation in which decisions on interest rates or exchange rates by the central bank are not hostage to irresponsible budget management by governments. In such a situation, debt problems in one part of the EU do not prevent stabilization in another part, and do not spill over to neighboring countries. In short, the rules were meant to be a barrier to simple cross-border free riding, where irresponsibility in one state becomes a financial problem for all the others.

The evolution of the Stability and Growth Pact

Right from the start, however, the Pact seemed to be failing. For how to enforce such strict and highly restrictive policies among sovereign countries? In hindsight, rather disheartening analyses from EU core institutions show that compliance with the budgetary rules between 1998 and 2019 occurred only about half the time.

The big blow came in 2003, when France and Germany, two key EU countries, both broke the rules but were not punished. Unlike earlier cases involving smaller countries, Paris and Berlin were not even threatened with sanctions. The European Commission did not have the courage to punish two large EU countries at once. Everyone else, however, interpreted this to mean that the rules are both unfair (because they do not apply evenly to big and small) and unenforceable, because even a small country cannot be threatened with an armed intervention to revert fiscal discipline.

More by Mojmír Hampl

To adopt or not to adopt? Pondering the euro question

Post-globalization: The West’s strategy options

All that is left now is the obligation for each country to submit the parameters of its budget in the spring of each year to the European Commission for evaluation and recommendations, which are then generally ignored.

Over time, the rules have thus become general theoretical guidelines, and have been further modified and made more complex. In 2005, for example, the so-called medium-term objective (MTO) rule was added. In order to allow budgetary policy to take into account the business cycle, the so-called “cyclically adjusted deficit” should not exceed one percent of GDP in the medium term. Simply put, in bad times the deficit could be higher and in good times it should be lower. Again, there are corrective measures in the event of a series of noncompliance with this rule and a mandatory return trajectory. The problem from the outset has been that this rule is based on a marker called potential output, which cannot be directly measured, only estimated. To make things worse, estimates can change significantly over time. How do you design a good forward-looking policy when you are aiming at a moving target?

After the eurozone fiscal crisis in 2009 – a result of disrespect for the rules mentioned above – further adjustments and modifications were made. In 2011, the so-called six-pack reform was adopted, which was meant to address not only budgetary irresponsibility, but generally all macroeconomic imbalances in EU member states, such as real estate bubbles or large surpluses or deficits in foreign trade. It has not succeeded. The subsequent two-pack reform, applied exclusively to the euro area, was in turn supposed to put more control on the growth rate of public spending. The most recent reform, in 2015, then gave the European Commission the power to assess and recommend structural changes in individual countries more rigorously. The goal was to ensure their return to sustainable levels.

The whole series of adjustments, flattening and decluttering was really just an admission of the obvious: a common monetary policy without a single fiscal policy is difficult by definition. (The rules of sustainable fiscal management apply of course to all EU countries, even those that do not pay the euro; every EU country can theoretically adopt the euro at some point, and economic policy is a matter of common interest for all members.) Some pipe construction and design faults cannot be repaired even by very determined plumbers. This was rightly feared by many of the eurozone’s architects, especially in northern countries.

Enforcement challenges

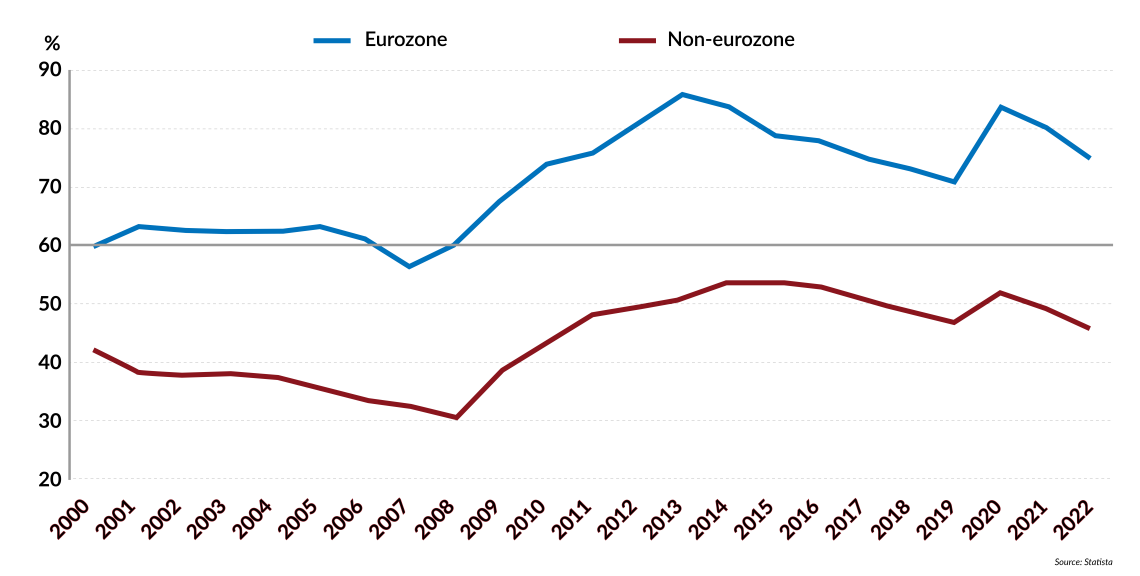

So what are the end results of more than 20 years of EU and eurozone life with fiscal rules? A sobering summary is provided by the chart below.

Facts & figures

Government debt levels to gross domestic product

The rules are more complex and opaque than ever, while governments continue, with honorable exceptions, to accumulate new debt. Debt-to-GDP levels are higher today than they were when the euro project was launched. And, paradoxically, it is euro countries that have, on average, higher debt levels than those that have retained their own currency.

The euro area, for which the rules were primarily designed, has a long-term debt-to-GDP ratio above the 60 percent ceiling set in the Stability and Growth Pact. It is therefore confirmed that a national currency can be a stronger shield against profligacy and overspending, as it does not allow easy free riding and transferring the costs of irresponsible policy across borders.

Except for a small group of countries such as Bulgaria, Denmark, Sweden or Malta, EU states are generally more indebted today than they were in 1999. And it seems that life in the EU, especially since the great financial crisis of 2008, has become an endless series of successive crises that always provide a good rationale for why the rules do not have to be respected.

Upcoming proposal

In this dismal situation, the EU has recently begun to debate how to reform and change the fiscal and economic rules again. In April this year, after a lengthy debate, the European Commission published a set of proposals for a major reform of the Stability and Growth Pact. The reform is intended to change both the rules for preventing fiscal crises and the ways in which past breaches are corrected. At the same time, they are to increase the weight and power of the so-called Independent Fiscal Institutions (IFIs), which are independent public bodies in each country that provide a politically unencumbered picture of the state of public finances and their longer outlook (the author of this text leads just such an institution in Czechia).

According to the new proposal, member states should regularly submit national medium-term plans based on a single indicator, namely the limit for net spending. This refers to the total amount that a government can spend in each period to achieve the planned objectives. In simple terms, the plan should ensure that debt is on a downward trajectory over the next four to seven years and the deficit is below 3 percent of GDP. Deviations from the planned net expenditure will then be assessed each year. Member states will effectively be redefining the rules on their own to achieve the fiscal sustainability objective. This would shift the focus from the short to the medium term and strengthen national ownership of stability. It would entail a fair acknowledgment of the fact that previous enforcement of the rules has failed, because the substantive decisions on budgets are made at the national level anyway.

The new rules are still being cooked and seasoned, so there are still many uncertainties. For example, under what conditions will a member country be able to request that the correction period of its budget exceed the basic four years? And also, how exactly will net expenditure be defined, meaning which expenditure will not count toward the limit? (Decarbonization costs, or one-off expenditure on defense?) The scope for budgetary creativity could be large.

However, the basic lesson remains the same. In principle, the rules of budgetary policy, which underpin any national political process, cannot be effectively enforced among sovereigns. There is no substitute for a country consciously pursuing fiscal responsibility at the national level. Nor will the creation of new institutions bring about better public finances. Genuine fiscal rectitude is the greatest virtue in a club that shares a currency and an economic destiny. But that is exactly what is critically lacking in the EU these days.

Scenarios

Reverting to stability

The first scenario assumes that the new rules, once up and running, will bring about a marked reversal in the budgetary policies of individual EU countries and help bring the debt burden, especially in the eurozone, back to 60 percent of GDP, as envisaged in the original Stability and Growth Pact. The new rules will work in such a way that a greater sense of ownership at the national level will also mean a greater willingness to comply with them. The probability of this scenario is 20 percent.

Continued uncertainty

A second scenario assumes that even the next modified version of the economic and fiscal rules will not ensure stability and stop the unsustainable accumulation of public debt in bad times and good. As in the past, budgetary policy will always depend on the sheer will and discipline of politicians in each country. In this respect, the differences between countries may even increase further. The probability of this scenario is 80 percent.

Sign up for our newsletter

Receive insights from our experts every week in your inbox.