The global battery race: Europe’s strategic perspectives

Slow at first to pick up on the disruptive nature of battery technology, Europe is now aiming to give the industry a boost. The U.S. and Asia, especially, have a head start. The stakes are high: if Europe loses out, not only could it suffer economically, but it could also lose its geopolitical influence for the benefit of China.

In a nutshell

- Asia and the U.S. are outpacing Europe in the battery industry

- The European Commission has put in place a strategy to narrow the gap

- Businesses, however, remain reluctant because of costs and other uncertainties

- Allowing China to dominate the European market will have severe geopolitical consequences

Europe was slow to discover how geopolitically disruptive the revolution in battery technology could become. Now, however, the European Union has identified batteries as the “heart of the ongoing industrial revolution,” playing a strategic role in the world’s transition to clean mobility and energy systems. Still, the European auto industry has been reluctant to get behind calls to create an “Airbus for batteries,” largely due to uncertainties surrounding the future of lithium-ion batteries, costs for manufacturing batteries in Europe and the possibility for overcapacity in the industry by 2021.

Critics of making a more strategically focused industrial/battery policy in Europe say that global markets and free trade will solve the challenges – but their assumptions are based on best-case scenarios. The global economy’s rising dependence on critical raw materials (CRMs) and battery cell production controlled by China, however, could shift economic power, change the rules of trade and rebalance geopolitical influence.

In October 2017, the European Commission launched the European Battery Alliance, a platform for cooperation between key stakeholders, member states and the European Investment Bank to create a competitive, sustainable battery-manufacturing industry. By last year, Europe had only one factory producing battery cells for electric vehicles (EVs) – located in the United Kingdom.

The EU wants to avoid a repeat of what happened in the solar panel industry, when it overlooked China’s policies.

The EU hopes to capture a global market share of 250 billion euros a year by 2025 through building between 10 and 20 large plants where battery cells will be mass produced. The idea is that these factories would both satisfy EU demand and maintain the bloc’s competitiveness in the industry against Asian and American manufacturers. The EU wants to avoid a repeat of what happened in the solar panel industry, when it overlooked China’s long-term strategic policies. Beijing used generous subsidies and loans to overtake Europe as the largest manufacturer and technological leader, while European solar-panel makers went bankrupt.

The future of the European Battery Alliance is closely linked with the EU’s Clean Mobility Package, a set of legislative initiatives to lower carbon dioxide (CO2) emissions from vehicles. Within the package, the EU approved new, lower emissions standards in December 2018. The target is for a reduction of 37.5 percent, based on 2021 levels.

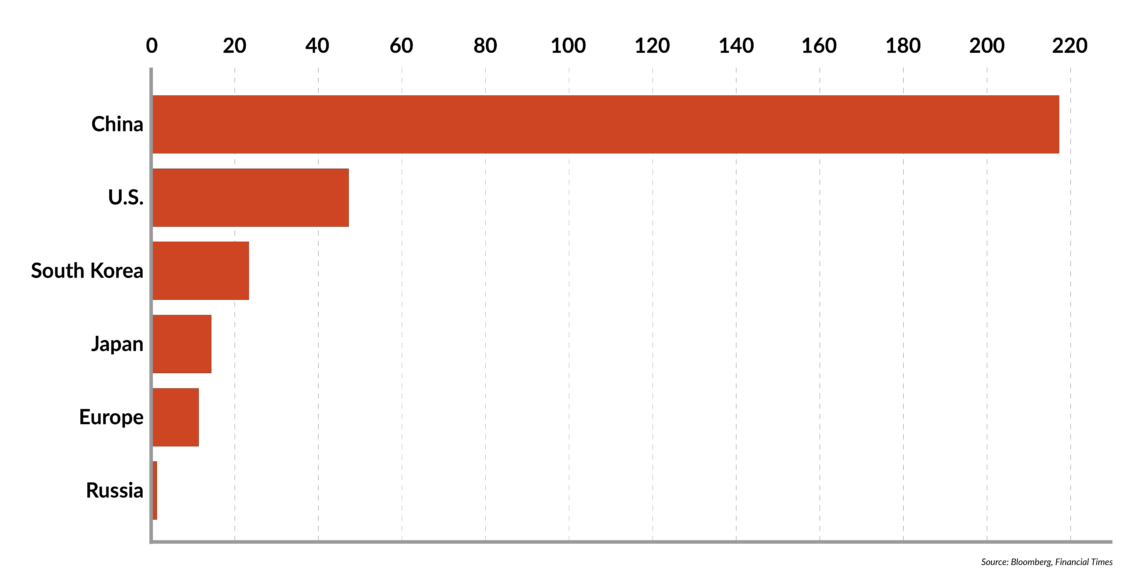

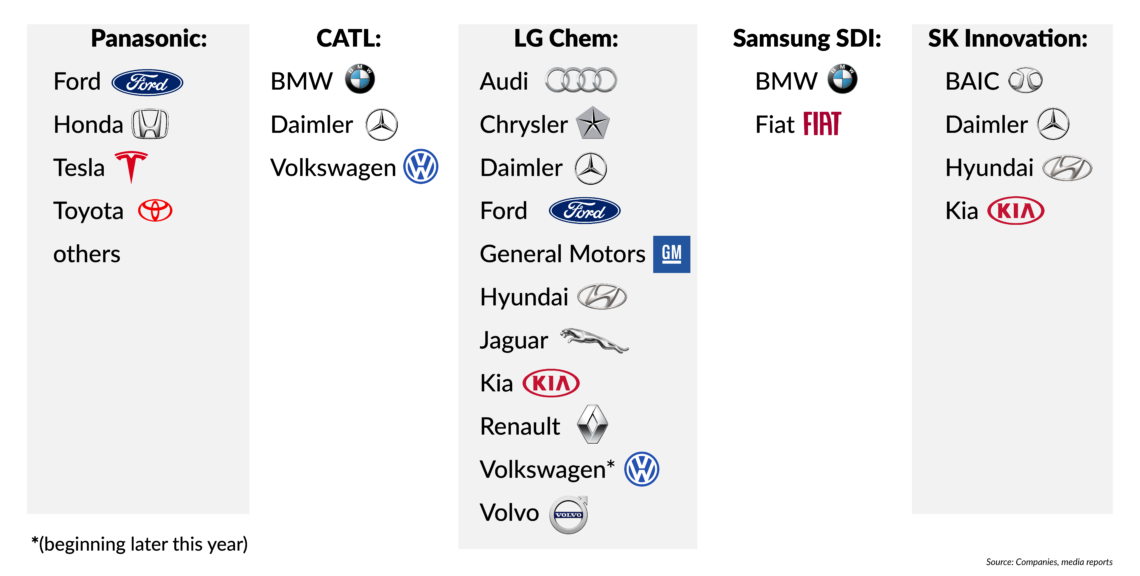

While 90 percent of a German car’s value is produced in Germany and other European countries, in the future 40 percent of the value chain could be located in Asia. Without any significant battery cell production in Europe, its companies must import batteries from China, South Korea and Japan. The Japanese firms Panasonic and NEC, South Korea’s LG and Samsung, China’s BYD and CATL, and American manufacturer Tesla dominate the global battery industry. Between them, they account for almost 80 percent of worldwide production. Due to breakneck growth and generous state subsidies (as part of its “Made in China 2025” program), China alone accounts for 69 percent of global battery cell production. The United States accounts for 15 percent and the EU some 5.3 percent. As the industry consolidates, it is estimated that by 2025 only seven to 10 of the 30 manufacturers operating today will survive.

Facts & figures

Battery manufacturers and the automakers they supply

European strategy

With its Asian and U.S. competitors in mind, the European Commission has developed an integrated, cross-border European approach for the entire battery value chain. Aside from battery cell production and design, its “Strategic Action Plan for Batteries” also addresses the challenges of extraction, processing and securing access to raw materials. The initiative tackles battery reuse, recollection, recycling and disposal, aiming for the smallest possible environmental footprint. It sets regulatory frameworks aimed at allowing the best industry strategies, research agendas and ideas to flourish.

Facts & figures

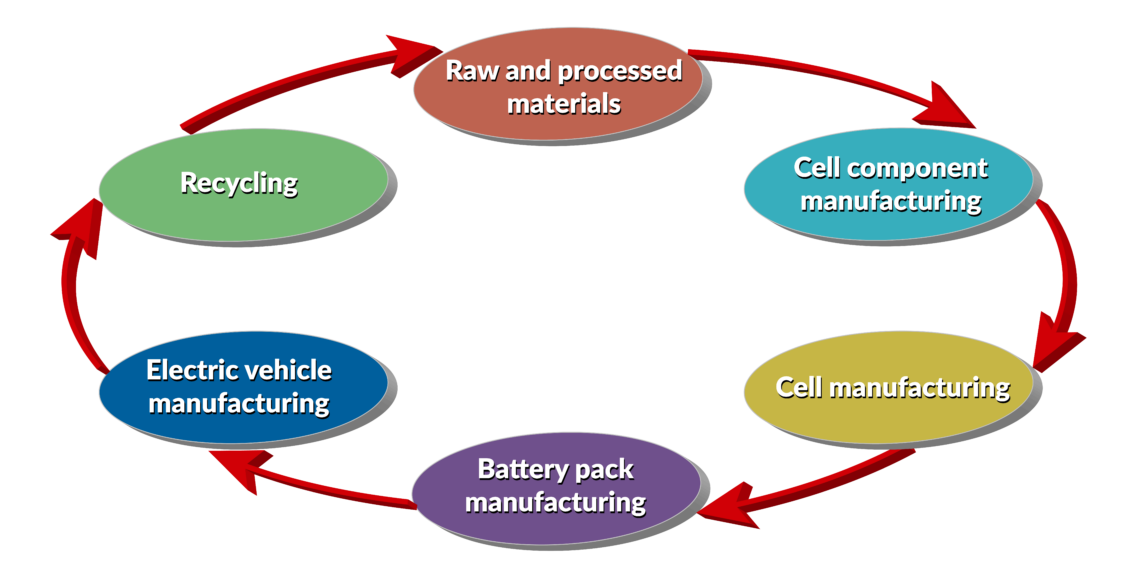

The battery value chain

The European Institute of Innovation and Technology has already built up a network of more than 260 participants from throughout the value chain. They cooperate on second-life batteries, labeling, carbon-footprint reduction, recycling, vehicle-to-grid communication systems, as well as education and training programs.

Without a battery cell manufacturing industry in the EU, Asian manufacturers could dominate the market, setting up shop in Europe to benefit from lower transportation costs and better-quality control. Meanwhile, Chinese President Xi Jinping’s nationalist economic policies have put numerous restrictions on foreign companies doing business in China, and domestic battery cell producers are likely to get preferential treatment. Beijing has reportedly already drawn up a “white list” of Chinese battery manufacturers with which carmakers are “encouraged” to do business.

If it does not begin producing batteries, the EU will lose jobs and its industrial prowess. The European auto industry employs some 13.3 million people, 6.1 percent of the workforce – 820,500 of them in Germany alone. About 600,000 of those jobs in Germany could be at risk. In 2018, only 4 million EVs were on the road worldwide, with nearly 40 percent of those in China. There are several reasons all this could change more rapidly:

- The price of lithium-ion batteries declined by 80 percent between 2010 and 2017. On the other hand, worldwide annual demand for battery capacity is set to increase from 70-gigawatt hours (GWh) in 2017 to 900 GWh in 2030

- An increasing number of countries have decided to phase out gas- and diesel-powered cars between 2025 and 2040 due to much more restrictive emissions targets in Europe, the U.S. and China

- From 2025, many European cities will only buy electric buses. Europe’s five biggest bus manufacturers (Daimler, Scania, MAN, IVECO and Volvo) have sped up their efforts to develop and build electric buses. Battery prices for e-buses are forecast to decrease by 9-12 percent annually on average to 2030, translating into a 75-83 percent decline in cost per kilowatt hour (kWh)

- Twenty-nine global automakers are investing more than $300 billion combined to develop and procure batteries and EVs over the next five to 10 years

- Of the 110 million new cars sold in 2030, as many as 40 million could be EVs. According to a new analysis from the International Energy Agency (IEA), the total number of EVs on the road could even top 1 billion by 2040

- By 2025, the global battery market could be worth as much as 250 billion euros, rising to 300 billion euros between 2030 and 2040. Battery sales could increase from less than $10 billion last year to $60 billion by 2030

- Lithium-ion batteries are not only used in the transport sector. They are increasingly being used for energy storage in electricity systems, the building sector and energy-intensive industries to cope with intermittency problems

- Their growing popularity is due to a dramatic fall in prices from almost $1,000 per kWh in 2010 to less than $230 per kWh in 2018. According to Bloomberg New Energy Finance, the capital costs of a utility-scale lithium-ion battery storage system could fall another 52 percent by 2030

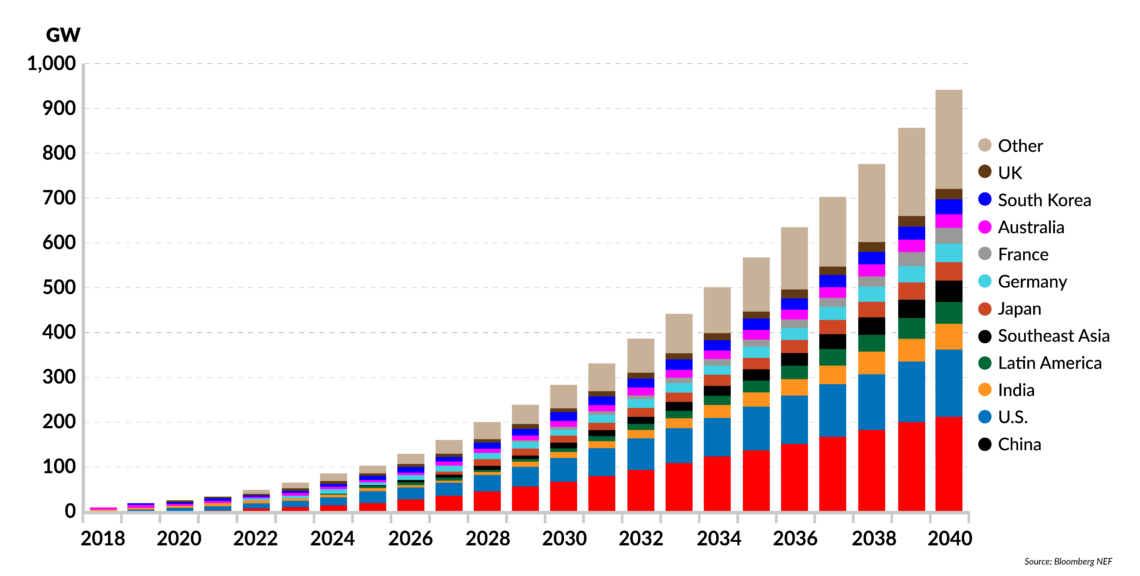

- By 2040, energy storage could grow to a point where it is equivalent to 7 percent of the total installed power capacity worldwide. Most storage capacity is expected to be utility-scale until the mid-2030s, when behind-the-meter applications could overtake it

Facts & figures

Global cumulative storage deployments

- Falling battery costs could fuel the expansion of renewables even faster than expected. A battery boom could increase the shares of solar and wind power to 50 percent of global energy demand by 2050. The amount that will be invested worldwide in battery capacity by 2050 has been estimated at up to $620 billion – two-thirds of that in grids and one-third by households and businesses

In 2018, plans for building battery cell production in Europe gained momentum and results are beginning to materialize.

Challenges ahead

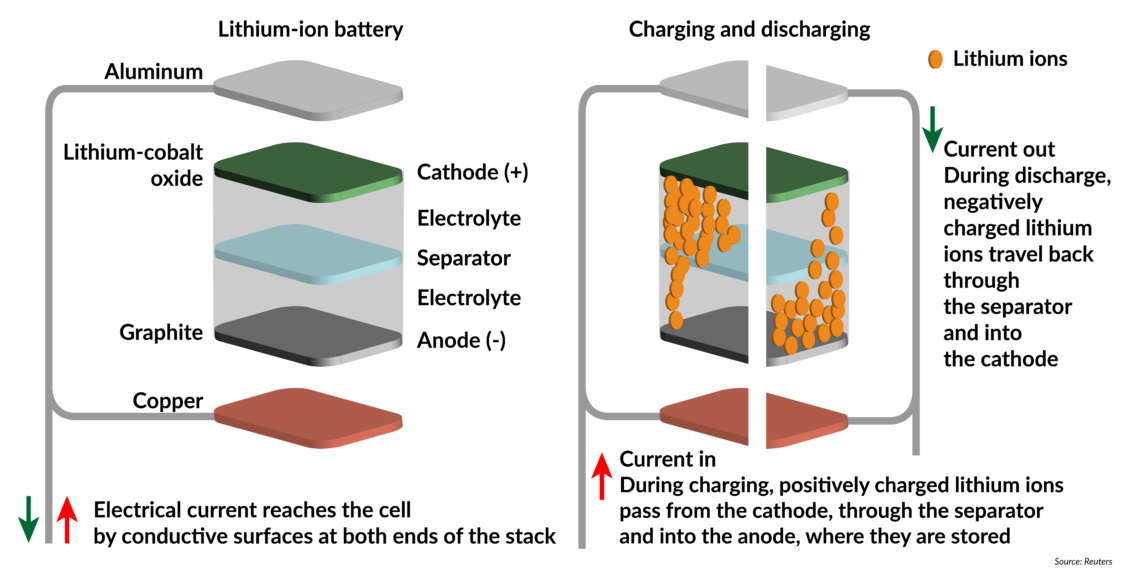

The battery industry in the EU is strong on the downstream side of the value chain (from battery modules up to pack assembly and system integration). Battery cell manufacturing, however, is almost entirely taking place in Asia. In 2016, China, South Korea and Japan together represented 88 percent of global lithium-ion battery cell manufacturing and were the home to the dominant suppliers of cell components such as cathodes (85 percent), anodes (97 percent), separators (84 percent) and electrolytes (64 percent).

Facts & figures

Inside a lithium-ion battery

Despite initiatives by the EU and various member states to encourage investment in battery cell factories, the industry remains reluctant to make such costly outlays (these facilities can cost as much as $30 billion) for several reasons:

- Though labor accounts for only about 10 percent of the entire cell manufacturing cost (production is already highly automated), skilled industrial engineering workers and specialists are often hard to come by in Europe

- Manufacturing battery cells is very energy intensive, with high CO2 emissions. Europe, and in particular Germany, has some of the highest electricity costs in the world. Without subsidizing the energy costs, Europe-made EV batteries will be far more expensive than those produced in Asia. BMW, for instance, has said it does not see the need for a European solution as long as there is plenty of competition between the Asian manufacturers

- The next generation of batteries – solid-state batteries – will be developed within the next five to 10 years (though widespread commercialization is not expected before 2030). In comparison with lithium-ion batteries, they weigh less, take up less space and have double the energy density. They are smaller, safer and offer a much greater range for EVs

Some forecasts have concluded that overcapacity in battery cell manufacturing could (temporarily) reach 40 percent worldwide and even to 60 percent in China by as early as 2021.

China has become the world’s largest and most dynamic EV market, with an estimated 140 million on the road by 2030.

- China has become the world’s largest and most dynamic EV market, with an estimated 140 million on the road by 2030. This raises questions about whether European carmakers will shift much investment from China to Europe. So far, they have invested seven times more in EV production in China than at home. In 2017, China secured 21.7 billion euros worth of investment in EV manufacturing, compared with only 3.2 billion euros invested in Europe

- In the face of fierce global competition, China has strengthened its efforts to maintain its technological lead by heavily investing in new generations of batteries with massive state-funded support. Beijing has shifted its focus from quantity to quality and has already stopped providing financial support for purchases of low-performance EVs with short ranges and eased some restrictions on market access for foreign companies. Between February and June this year, such subsidies will be further cut by 30 percent and from July by another 50 percent

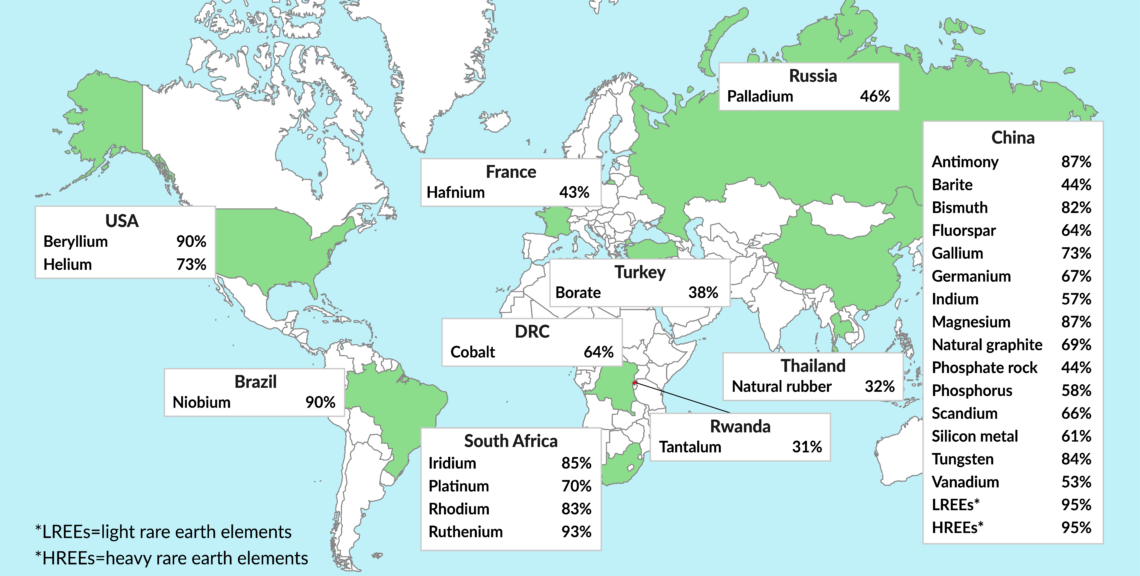

Europe’s capacity for manufacturing batteries also depends on securing continued access to the various metals and CRMs required for their production. Here, Beijing has a huge advantage. For years it has had a robust strategy for securing access to such materials, many of which are mostly found in China itself. Chinese firms can obtain lower prices from suppliers due to their much higher purchasing volumes and their preferred status over foreign companies.

China accounts for between 85 and 90 percent of worldwide production and exports of rare earth minerals. Outside its borders, it is working to acquire control of mines and reserves of materials such as lithium and cobalt. While the currently available materials might be sufficient for the next wave of EVs, concerns have increased about a shortage of lithium, cobalt and nickel that could occur after 2025. There are plenty of uncertainties about when the next generation of batteries will enter the market, the mix of chemicals the cells will require, how much recycling could ease demand pressure and whether the life of EV batteries could be extended beyond the current average of eight years.

Facts & figures

Countries accounting for the largest share of global CRM supply

Scenarios

Europe has to cope with five major interrelated geoeconomic trends with wide-ranging effects: the revolution in the transport sector, the intensifying battery “arms race,” China’s rising technology know-how, the global shift in trade dynamics and the growing global competition for access to CRMs.

If the EU and its member states can get up to 20 large battery factories constructed across Europe, its global market share could rise from 5.3 percent today to almost 20 percent by 2028. It is estimated that Germany would be the leader, with 5.9 percent. On the other hand, China’s share would decrease from 60 percent today to 53.8 percent.

Nevertheless, since China will have the largest EV market, remain strong in battery manufacturing and research, and will benefit from its policy to secure supply of CRMs, the future of the industry will certainly lie in China. The question is to what extent. In this regard, the EU’s proactive policies for building battery cell factories, supporting research and development for a “circular” battery economy and securing CRM supplies will gain utmost strategic importance.

Some players in Europe’s battery industry say they prefer to rely on market forces and free trade to solve the region’s challenges. That approach may prove shortsighted. It requires a best-case scenario, which looks unlikely. Geopolitical factors have already undermined free-market assumptions and might erode them even more as the race for CRM supplies heats up. The demand for lithium is set to triple by 2025, while China dominates the rare earths, lithium processing and battery precursors supply chains, among others. In the face of the geopolitical risk this dominance presents, the U.S. signed a memorandum of understanding last year with Australia, the world’s largest lithium mining country, to work jointly on “strategic minerals exploration, extraction, processing and research.”