Examining Latin America’s ‘puzzle’ of low growth

Why does Latin America’s economic growth remain so sluggish? Economists have addressed the question with reams of analysis, but the answer is simple: low productivity. That, in turn, has been caused by government involvement that has stifled competition and innovation.

In a nutshell

- Latin America’s economies lag other developing countries

- High-spending policies have hampered productivity

- Encouraging the region to spend more will continue to hold it back

One of the most curious policy developments of the coronavirus pandemic was the radical change the International Monetary Fund (IMF) made to its recommendations. The organization abandoned its decades-long stance that austerity, fiscal orthodoxy and structural reforms are the best economic medicine. Instead, the IMF began encouraging countries to increase public spending to fight the downturn caused by the disease, even if it meant risking fiscal stability.

The main reason for the change, according to IMF Managing Director Kristalina Georgieva, is to avoid the “scarring” that comes with collapse and to thereby preserve productivity. The IMF has told countries to “spend and keep the receipts.” Even though it was qualified with the advice to do so “wisely,” some joke that the instruction sounds like “jump off the roof but count the floors as you are falling.” This interpretation rings especially true for Latin America.

According to IMF data, over the past five years, the region’s real gross domestic product (GDP) grew at an average annual rate of 0.46 percent, compared to 3.36 percent for all emerging market and developing economies combined. With the pandemic came the prospect that Latin America could see the worst recession of the group. Collectively, the region’s economy was projected to contract by 8.1 percent in 2020, while together, developing economies were expected to shrink by 3.3 percent.

Income growth is so slow that it will take the region more than a century to close the income gap with developed countries.

In 2021, Latin America is expected to recover less than half of 2020’s losses, growing at 3.6 percent. Its peers in Asia, Europe, Africa and the Middle East are likely to recover faster. Under normal circumstances, a healthy growth rate for Latin America would be above 4 percent per year, making the underperformance that much more problematic.

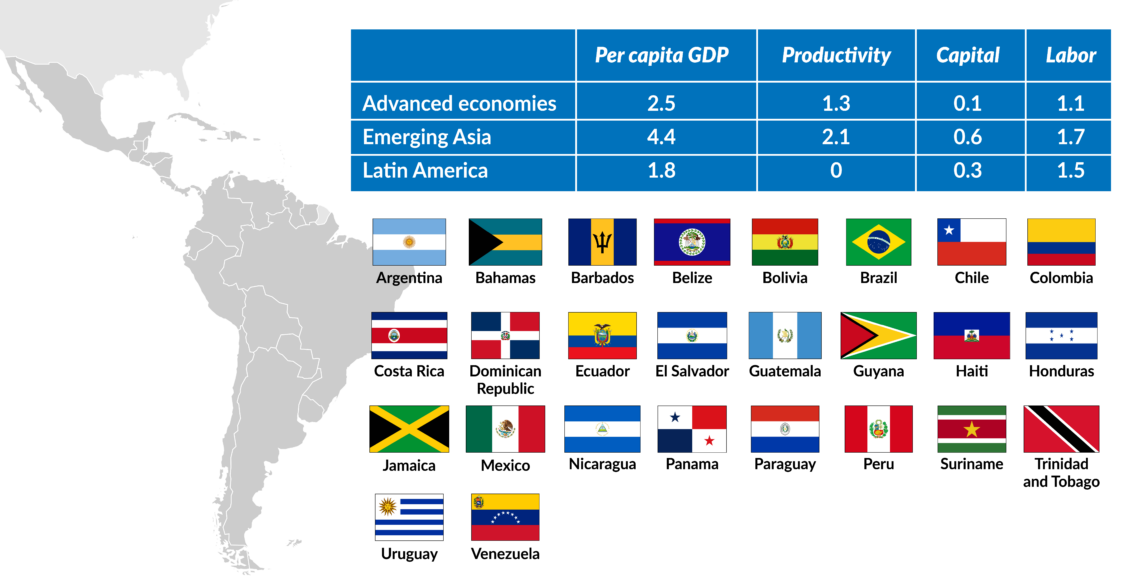

Per capita income growth in the region is even more disappointing. Inter-American Development Bank (IDB) data shows that from 1960 to 2018, Latin America’s GDP per capita grew only 1.8 percent annually. In developed economies the figure was 2.5 percent and 4.4 percent in Asia.

In a 2001 report, the IDB pointed out that Latin America’s income growth was so slow that it would have taken the region a full century to close the income gap with developed countries. Now, it will take longer.

‘Puzzle’ pieces

The IDB calls the pattern by which the region’s economies consistently grow slower than in the rest of the world a Latin American “puzzle.” Numerous economic studies have examined the phenomenon. They conclude that the root of the problem is low productivity and stagnant productivity growth.

In Latin America, investment in capital, labor and education over the past 60 years has been much smaller than those in Asia’s fastest-growing emerging economies, but bigger than in advanced economies. Yet while productivity in emerging Asia grew at an average annual rate of 2.1 percent (and at 1.3 percent in developed countries), for Latin America, the figure was zero. Productivity there remains the same as it was 60 years ago.

Facts & figures

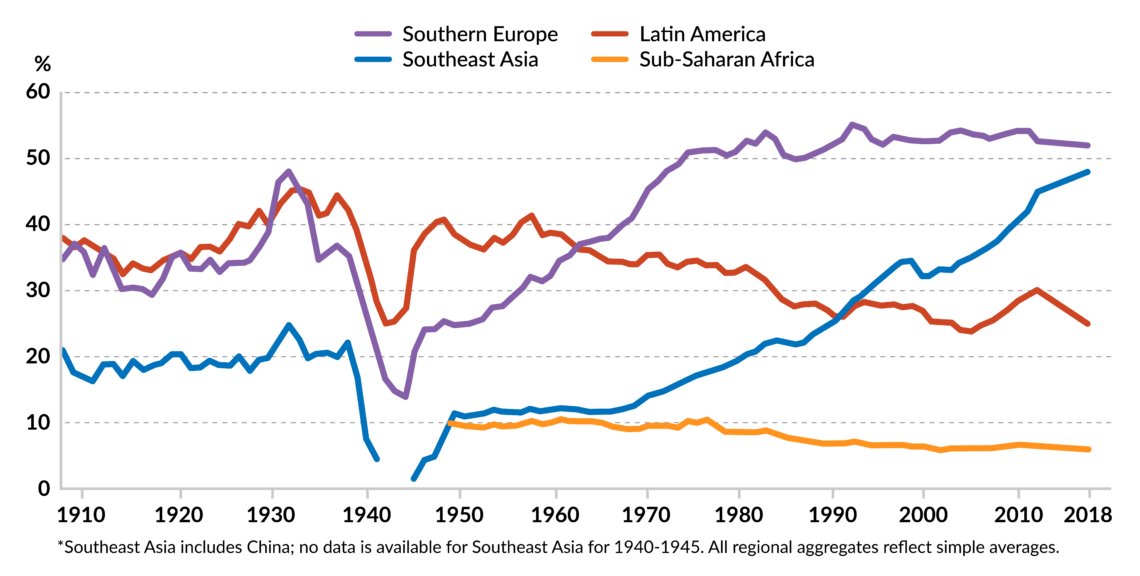

Because of these differences in productivity, the gap in the standard of living between rich countries and Latin America is even greater than it was a century ago. Poverty in the region has fallen substantially, but the richest 10 percent earn 22 times more than the poorest 10 percent, compared to just nine times more in the developed economies of the Organisation for Economic Cooperation and Development (OECD). The erosion of the middle class makes it tougher to adopt political and economic reforms that are necessary to promote growth.

Lack of competition

Why has productivity not advanced? Nobel laureate Joseph Stiglitz once wrote that well-functioning economies require a balance between government and markets. In Latin America, the balance is off: governments typically play an outsized role in the economy.

Innovation and the creation of new knowledge, which are essential for productivity growth, are driven by competition. For decades, Latin American governments favored the expansion of the public sector and an increase in the number of state-owned enterprises. Industrial policies have provided subsidies and incentives to specific economic sectors and promoted national champions. Such policies, along with import substitution, protectionism and restricting foreign investments, prevented healthy competition.

In domestic markets, excessive regulations, bureaucracy, deficient capital markets and financial systems, as well as rigid labor laws that keep workers from moving to more productive companies or sectors, have created high entry costs for new firms. The World Bank’s Doing Business 2020 report, which compares business regulations in 190 economies, lays bare these barriers to competition: no Latin American economies rank in the top 50 in its index for ease of doing business. Brazil, the region’s largest economy, ranks 124.

Instead of competing with better goods and services, these companies exploit their economic power by rent-seeking.

Income in the region is concentrated in the hands of a few large companies that have a monopoly or dominant position in particular economic sectors. They are often fully or partially state-owned; many of them are utilities or exploit natural resources. These companies usually have privileged access to low-interest financing and various tax incentives and are not interested in innovating or having more modern and efficient management.

Instead of competing in the market with better goods and services, these firms exploit their economic power by rent-seeking, charging prices well above costs and taking advantage of the lack of competition. Such companies usually have a close relationship with the political class and block policy changes.

Other Latin American firms are mostly small. Very few have more than 50 employees. A large portion of the labor market is made up of self-employed professionals or individual microentrepreneurs. Nearly half of the people in the workforce have informal jobs, with no safety net and little access to financing. Only 40 percent of people in Latin America have a bank account, compared with more than 90 percent in the OECD.

The result is a lack of economies of scale and of scope. There is no incentive to innovate and apply new technologies or learning by doing, which is normal for large competitive companies. Most micro and small businesses have very low productivity and are not integrated into international trade and global value chains.

Premature deindustrialization

Small firms in Latin America do not have many incentives to grow. On the contrary, there are various policies that encourage them to remain small: microcredit, tax incentives and other special tax regimes, as well as the minimum wage and social benefits for low-income families. Such policies do little to improve income distribution, which exacerbates inequality, unemployment, insecurity and grows the shadow economy.

The countries produce less, but government spending increases, leading to unsustainable public debt.

The mortality rate of micro and small companies in Latin America is extremely high. But when these firms die, they are replaced by others of a similar size and with the same low productivity.

As a result of all of these dynamics, the region’s large economies like Brazil, Argentina, Chile and, to some extent, Mexico, are going through a process that economists call “premature deindustrialization”: they start to lose their manufacturing jobs without getting rich first. Specialization rises in commodities, natural resource exploration and low productivity services.

This tendency, in turn, is leading to boom-bust cycles of economic growth and fiscal volatility caused by dependence on commodities. The countries produce less, but government spending increases, leading to unsustainable public debt. Even during the boom phases, governments have been unable to reduce public debt and spend more rationally.

Scenarios

The Covid-19 pandemic brought additional challenges to Latin American countries. Brazil, Argentina, Mexico, Chile and Peru are among the nations most affected by the outbreak, suffering significant economic harm. Argentina is on the brink of fiscal collapse, Venezuela’s political and humanitarian crises worsened, and Peru is in grave political turmoil.

Brazil presents an interesting case for examining the scenarios that could stem from these circumstances. Before the outbreak, the Brazilian government was implementing economic reforms to promote trade openness, reduce public spending and increase the private sector’s participation in the economy. It was a difficult political road to travel – such policies often met opposition even within the government itself.

The pandemic took the focus off economic reforms, as the administration engaged in emergency spending to mitigate the negative effects of the pandemic. Government outlays have skyrocketed, further destabilizing the country’s finances.

Moreover, there is mounting political support to break the existing cap on public spending and broaden expansionary policies. If Brazil were to follow the IMF’s recommendation to further increase public spending, it would result in catastrophe. The century-long stagnation in Latin America shows how government intervention and excessive, inefficient spending impede competition and productivity growth.

Implementing orthodox macroeconomic policies would prove a much better strategy: promoting economic openness, competition and private investment, while slashing regulations and addressing social dysfunctions. The pandemic makes it difficult to do this in the short term, but it would be the most optimistic medium-term scenario.

The most likely scenario is one in which the government implements some reforms, but not all of those that it originally promised and which the country needs to return to growth.

For the rest of Latin America, the short and medium-term scenarios look more pessimistic. It is likely that most of the countries will maintain the status quo, avoiding necessary but unpopular reforms. Mexico and Argentina are moving further away from the orthodox model, expanding policies of economic nationalism. After its recent social upheaval, Chile is rewriting its constitution to include more interventionist government policies.

Without reforms and with public spending on the rise, Latin American countries will remain poor. That is something for the IMF to consider.