Microchips subsidies: Protectionism, not security

The political popularity of the European Chips Act does not necessarily make centrally planned investment in chip manufacturing a great idea.

In a nutshell

- The EU is about to invest in local chip manufacturing to spurt innovation

- The hefty public investment is also supposed to increase Europe’s security

- The cutting-edge industry is unlikely to meet technocratic expectations

According to the press and people deemed experts, a microchip war is going on. China, the United States and the European Union are each setting up production clusters for semiconductors, the chips that process digital information. The justification for these industrial policies is improving national security. In predictable reality, however, the expensive process will produce opposite results.

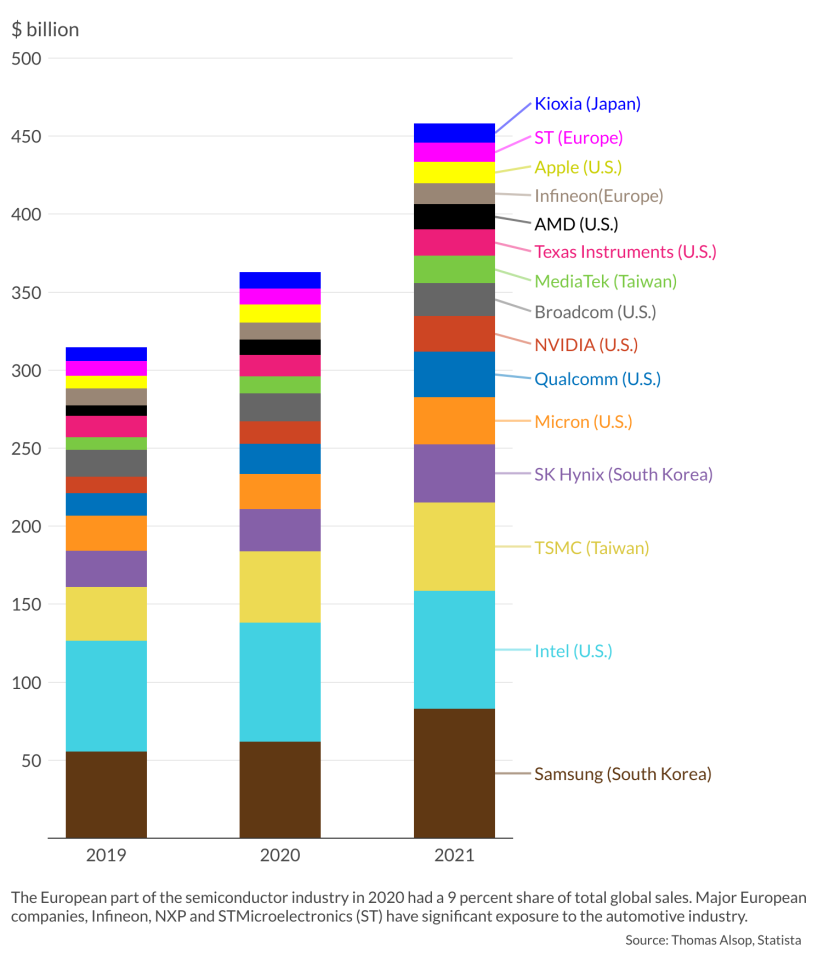

The demand for semiconductors has surged over the last decade in quantity and quality – unsurprising since they run virtually every advanced electronic device. In contrast, the microchip supply is concentrated in very few nations – including the U.S., Taiwan, South Korea, Japan, some EU countries, and increasingly, China. Notably, Taiwan accounted for more than 63 percent of total semiconductor manufacturing revenue in 2020.

Because of this concentration, microchip supply chains are subject to high interdependencies and exposed to security risks and trade wars, among other risks. Also, the more geopolitical friction, the higher the risk levels affecting those supply chains.

The lure of industry policy

Now, the story turns to political marketing – or even science fiction. Several governments, notably in Europe and the U.S., claim that after the experiences from the Covid pandemic and the war in Ukraine, they need to repatriate chip manufacturing. This claim is based on a loosely constructed link to security, innovation and job creation. It does not seem pertinent that these arguments all fail. The more they do, the more enthusiastic their political defense becomes.

The European Chips Act still needs full approval, but the political enthusiasm is already there.

The U.S. has been discussing massive investments and incentives – almost $53 billion under Congress’s bipartisan CHIPS and Science Act to support homegrown manufacturing, research and development and supply chain resilience. The EU also aims to establish global leadership and make similar investments: during the 1990s, the bloc had over 40 percent of the chips market, but by the early 2000s, this figure had fallen to 24 percent. It barely reaches 10 percent today.

The European Chips Act still needs full approval, but the political enthusiasm is already there. With the Act, the European Commission promises to finance innovation and to industrialize processes “to bring the lab to the fab.” The Commission wants to create new applications, including connected and automated vehicles (CAVs), telecommunications, the digitization of the health sector and significantly increase security and defense.

The EU aims to reduce its dependence on international markets because, as the Commission puts it, “The chip industry is one element in the competition for technological supremacy between China and the United States.”

An investment package of around 11.3 billion euros has been pooled from existing EU instruments. These include the research program Horizon Europe, the coronavirus recovery fund and national government budgets. The European bloc aims to mobilize more than 44 billion euros of public and private funds in the hope of doubling the EU’s market share of the semiconductor market by 2030.

Pitfalls of the Chips Act approach

The EU’s plan is so full of problems that it amounts to fiction. They are, for one, the difficulties inherent to industrial policy, but the EU still manages to give them an even more problematic spin.

The first problem is simple: There is no market for the EU’s chips. At least, not in the way the multibillion dollar-package estimates it. That means the EU’s push does not come out of a changing pattern of world demand but only from some politicians’ minds. And since this demand does not stem from markets, there is also no feedback mechanism informing the central planners how to distribute the allocated money. Even if European or U.S. manufacturers welcome the package, this is not a sign coming out of actual market feedback. Most firms obtaining free money welcome it.

The second problem is that there is no unified production of microchips. The link between research in new technologies and materials, their adaption to marketable products, and their manufacture is not easy to establish. Also, the EU package does not address this problem, presupposing the existence of a seamless supply chain that can be onshored frictionlessly into the EU. The task becomes even more questionable in the absence of the feedback mechanism of markets.

The third problem is balancing the EU’s stated aims of decreasing dependence on foreign producers – whatever that means – on one side while continuing to work with international partners on the other. Strictly European solutions to secure semiconductor supplies risk reinforcing autarkic tendencies and creating additional inefficiencies and duplications in value chains. It also risks alienating countries such as the U.S., South Korea and Taiwan.

Under such a scenario, microchips would become pricier due to the EU’s higher production costs and taxes.

The additional EU-specific problems are twofold: smaller EU countries fear that bigger states, such as France and Germany, will outbid them for chip investment. This fear is exacerbated by the new EU-U.S. tech alliance, the Trade and Technology Council, in which France is expected to take control of the semiconductors negotiations.

And finally, the EU’s funding is conditioned upon member states’ funding, which is everything but secured.

Scenarios

How is this new attempt at industrial policy going to play out? It is practically certain that the proposal will pass. Even if it is somewhat re-dimensioned, the EU decision makers will be on board since industry policy is one of the core political demands of the time. So, if the question is not “if,” it must regard the results.

Europe’s success

In the first scenario, the EU manages to relocate and integrate the chip supply chain. The likelihood of this happening is less than 10 percent. If its policy is successful, the EU will become one of three to four top places globally for manufacturing microchips. That outcome would enhance the transatlantic trade links – that is, with the U.S., one of the biggest markets for microprocessors, and South America, the source of raw materials.

That would lead to a diplomatic shift and increased confrontation of the Atlantic alliance with the Far East. The change could make Taiwan less resilient toward China. Under such a scenario, microchips would become pricier due to the EU’s higher production costs and taxes. Which, in turn, would slow the diffusion of European electronics on the world market.

Partial implementation

The second scenario has a likelihood of around 60 percent. Some companies in the EU, notably those in France and Germany, will use the money to their advantage. They will be able to integrate parts of their supply chain and expand their production. To some degree, they will also be able to innovate.

That, however, will not be enough to divert global trade patterns or break the market position of manufacturers in Taiwan or South Korea. Global trade flows and supply chains will resist fundamental change. The recipients of EU money will prefer to sell their chips in the global market where they can capitalize on the EU’s provenance, therefore integrating the EU even more in international trade. In this scenario, the EU’s push has no consequence for its security and global trade position but has an effect inside the Union. Most member countries will end up financing a few firms in a small group of producer countries.

Race to the bottom

The third scenario has a likelihood of around 30 percent. In this version of the events, the problems of industrial policy come to light. To continue the political commitment to its Chips Act while avoiding backing up relatively efficient and innovative manufacturers in France or Germany, the EU decides to subsidize industries equally in all its member states. Or worse, to distribute funding with a priority to inefficient, backward places within the Union.

In this case, instead of building supply chains, the EU would be just distributing money with little impact on the production of microchips. Moribund industries would compete for financing in this race to the bottom while turning out marginal volumes of poor-quality chips. As a result, the EU would crowd out true innovation based on scarcity, market signals, and feedback loops.

On the other hand, since these policies have no impact on the global market, agents outside of the EU would not be affected by them.

Collateral damage

All these scenarios share a threat: The EU might be unleashing yet another trade war. This one would, however, target its partners, especially those in Asia. This collateral damage is, at present, not factored into the EU’s thinking.

What looks to be a chip war for the sake of security is actually a mundane push for industrial policy. The EU’s Chips Act is primarily an exercise of protectionism. It bears the risk of unleashing a trade war.

If the policy fails economically, it will be merely expensive and inefficient for the EU member states themselves. However, if it succeeds economically, it also risks isolating the Union’s partners in Asia, even giving China a more significant role in the East.

Geopolitically, the former is less troublesome than the latter, but it remains a nuisance. Industrial policies tend to overpromise and underdeliver. With the Chips Act, it will most likely be no different.