Energy megatrends and the challenges of decarbonization

Despite increasing support for net-zero emissions targets and the rapid development of green technologies, global temperatures are still likely to rise. Countries worldwide are struggling to accelerate the switch to green energy – and the pandemic is not helping.

In a nutshell

- Governments rolled back green targets during the pandemic

- Emissions could rise once the economy recovers

- Developing countries will struggle to finance energy transitions

This GIS 2021 Outlook series focuses on the opportunities that stem from the upheaval of the past year.

The transition from fossil fuels to renewable energy will pose several challenges and create new vulnerabilities in the forthcoming decades. The process will particularly affect the global electricity sector, which is currently being transformed by the so-called “3D” strategic trends – decarbonization, digitalization and decentralization.

The transition to renewable energy is highly dependent on modernizing energy infrastructure (especially electricity grids) and reforming regulatory frameworks to accommodate shifting energy supplies. Societies and states are becoming ever more dependent on the stable functioning and resilience of critical energy infrastructures against increasingly sophisticated cyberattacks. But political decision-making and regulators often adapt too slowly to be able to benefit from new options arising from disruptive technology.

The economic impact of Covid-19 is threatening the investments needed to achieve global carbon neutrality by 2050.

Given the electrification of end uses and the proliferation of low-cost renewable power generation technologies, electricity is emerging as the strategic energy carrier of the 21st century.

Meanwhile, the worldwide quest for decarbonization is creating new supply chains from unfamiliar sources, including internet giants such as Facebook, Amazon, and Google. Supply chains will increasingly shift toward decarbonization and include hydrogen and batteries for electric vehicles, which will also increase the global dependence on critical raw materials.

Energy post-Covid

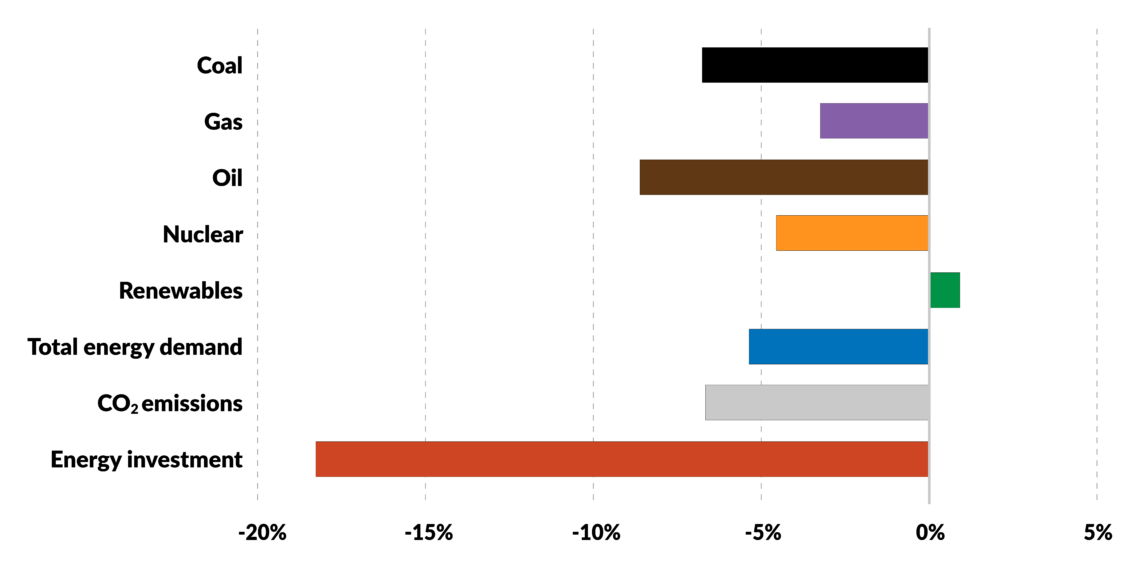

The Covid-19 pandemic has caused more economic disruption in the energy sector than the 2008 financial crisis, the 1930s economic crash, or any other peacetime event. In May 2020, the International Energy Agency (IEA) was already warning that the “energy sector will never be the same.”

Facts & figures

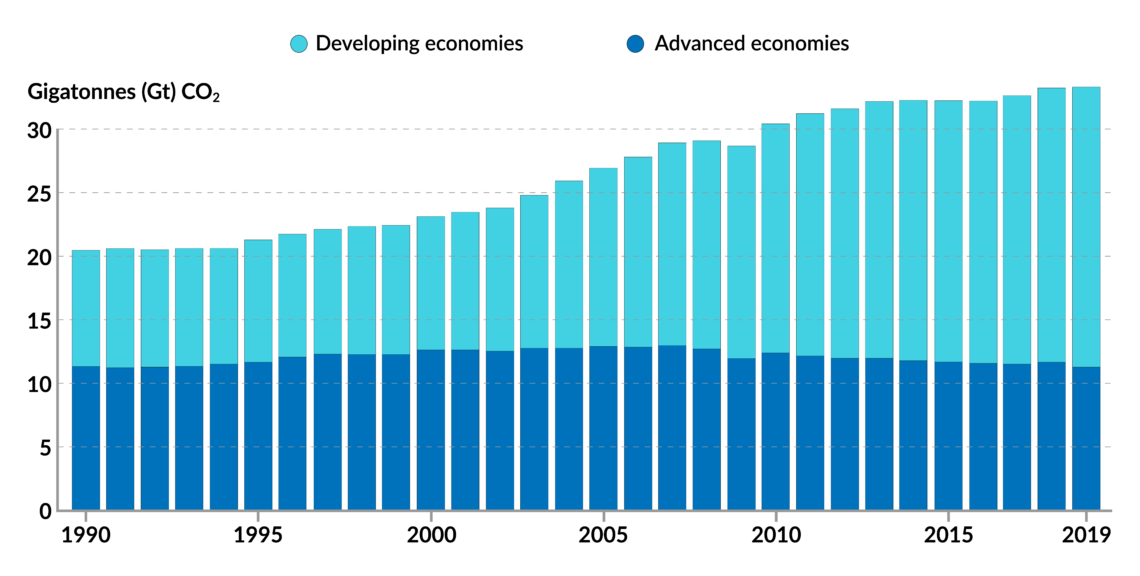

It is unclear how long the pandemic will last, and its impact will vary between countries and regions, as well as within societies. Financial fragility is already on the rise in high-income economies, but even more so in emerging and developing countries. The worldwide reduction of CO2 emissions that took place in 2020 could reverse once the world economy recovers.

In 2019, total energy-related CO2 emissions fell by 3.2 percent after having risen for several years. In 2020, greenhouse gas emissions decreased by 7 percent. But methane emissions still rose by nearly a third due to leaks from the oil and gas industry in the first eight months of 2020, despite reduced economic activity. Global emissions may not peak before 2030. But greenhouse gas emissions still need to fall by 7.6 percent every year between now and 2030 to stay below the 2 degree Celsius increase in temperature from preindustrial levels that scientists say could lead to extreme climate events.

Facts & figures

The economic impact of Covid-19 is threatening the massive investments needed to achieve global carbon neutrality by 2050. The IEA warns that without radical changes in energy consumption and production, as well as in consumer behavior, global temperatures will increase by another 1.65 degrees Celsius. Around 40 percent of cumulative emissions reductions needed to reach the net-zero goal by 2050 still rely on large-scale industrial technology that is not commercially available, like hydrogen, batteries, and carbon capture, use and storage (CCUS).

In 2020, major emitters such as China, India, Russia, and the United States poured more than 50 percent of their new investments into fossil fuels as part of pandemic rescue packages. Many other governments bailed out their fossil fuel industries and rolled back environmental regulations during the pandemic. The health crisis has widened, not narrowed, the gap between reality and the ambitious goals of the Paris Agreement.

Facts & figures

Bridging the gap

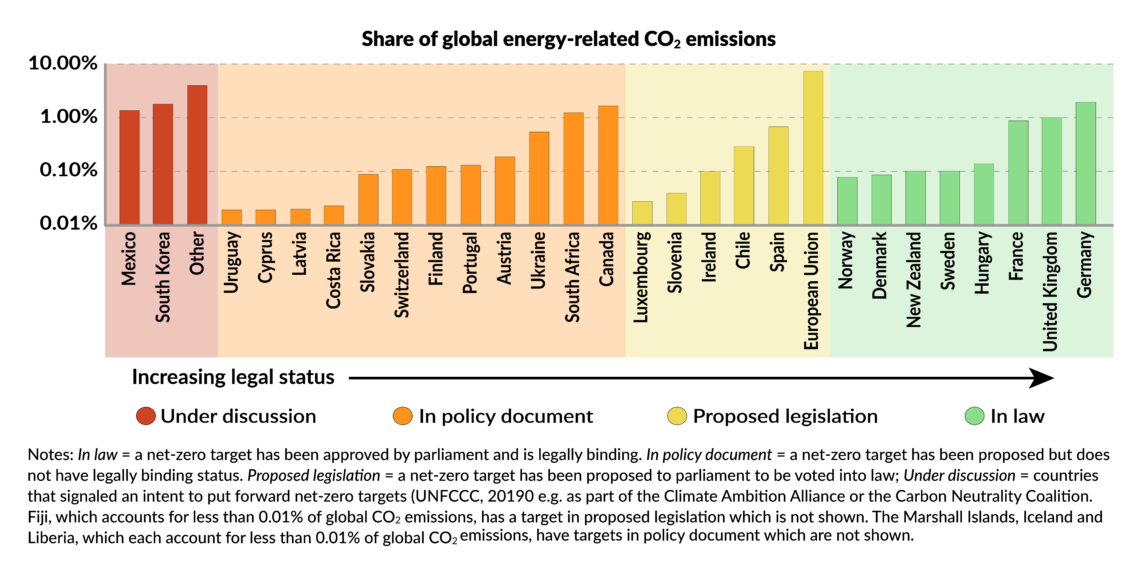

In Europe, efforts toward decarbonization have intensified with the European Union’s new “Green Deal” and its ambitious emissions reduction target of 55 percent by 2030 – previously 40 percent. The Biden administration has announced it would spend over $2 trillion to decarbonize the U.S. energy mix and make its industry greener. China is also expected to accelerate its energy transition with more ambitious targets – also to keep up with the U.S. green technology revolution in the context of their geo-economic rivalry.

Despite China, Japan and South Korea recently setting carbon-neutral targets, they have yet to announce commitments to stay below the 2 degree threshold by the mid-term perspective 2030 like the EU. On one hand, advanced economies – including China – will need to set examples that developing countries can follow. On the other, emerging economies will need to aim for even more ambitious policies to catch up. But with population growth and improving living standards making the challenge increasingly difficult, they might need more international support to reach these goals.

More than ever, hopes are turning to China. But in 2020, the country began operating an additional 38.4 gigawatts of coal-fired capacity. It also approved the construction of another 36.9 gigawatts last year, totaling 88.1 gigawatts. In total, it has 247 gigawatts of coal power under development – more than the entire installed power capacity of Germany (214 gigawatts in January 2021). Its coal output is at its highest since 2015. China’s total renewable energy additions declined by 40 percent in the first half of 2020, although for the first time, renewables also accounted for more than coal in Belt and Road investments.

Facts & figures

In parallel, the rapid rise of disruptive and energy-intensive innovations like cryptocurrencies, blockchain, smart homes, the Internet of Things and cloud systems could derail many forecasts. The worldwide introduction of 5G could dramatically increase network electricity needs, like with the 3G and 4G deployments. This could even double the energy consumption of communication service providers.

For all countries, but especially emerging economies, finding new ways of financing faster decarbonization and clean energy will be critical in the coming decades.

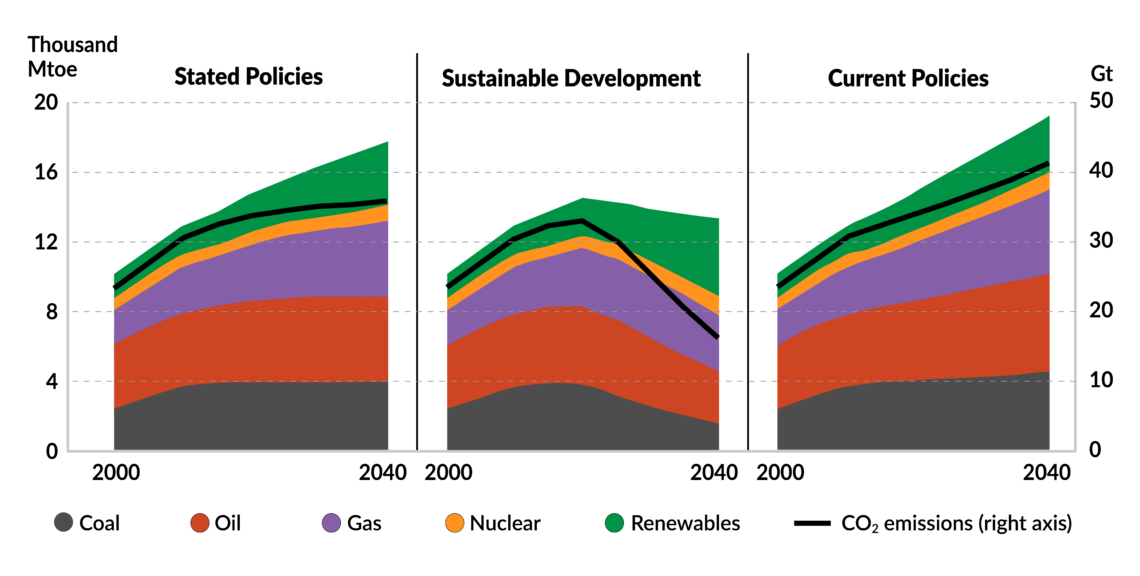

Scenarios

Scenario 1: Slower decarbonization

In 2019, the IEA’s forecast for the 2040 global energy mix included between 50 and 70 percent fossil fuels, depending on various scenarios. China was considered likely to remain the world’s largest energy consumer, with the largest energy demand growth in India. Some aspects of the situation are more uncertain: the future U.S. shale revolution; the evolution of fossil fuel consumption – particularly in Asia; the speed of the global energy transition; future climate change mitigation policies; and energy efficiency gains.

In the IEA’s new scenario, by 2040 global oil output still rises by around 10 percent and natural gas production by almost 40 percent. Over the past 20 years, Asia accounted for 90 percent of all coal-fired capacity. Worldwide coal production might further decline, though a higher output in India and some other countries could offset reductions elsewhere. In an alternative, more optimistic IEA scenario, however, coal production in 2040 could fall more than 60 percent as renewable energy sources would challenge coal in Asia’s power sector (even in China and India). CO2 emissions could also be significantly reduced by retrofitting, repurposing, or retiring coal plants in a cost-effective way. But global coal demand is expected to rise by 2.6 percent in 2021, after a record decline of 5 percent last year.

Already in 2019, the IEA had noted an alarming gap between expectations of a fast transition to renewable energy and the reality of today’s fossil fuel-reliant systems. It forecast a 30 percent increase in global energy consumption by 2040 – the equivalent of adding the present consumption of China and India to current global demand. Worldwide electricity generation was projected to increase by 60 percent and make up 40 percent of final consumption in 2040. This was in line with the slower energy efficiency improvements of 2018 (only 1.2 percent, half of the average rate since 2010).

The declining price of renewable energy often hides many additional systemic costs for the modernization of grids and grid interventions. Also, because renewables face intermittency problems, conventional power plants often need to be subsidized as backups for grid stabilization.

The pandemic could affect the energy sector more than initially anticipated and have more long-term implications. In this scenario, the global oversupply of oil, gas, and coal could last longer than expected. “Peak oil demand” would not be reached before 2030 since oil would remain inexpensive and developing countries would not have the financial resources to afford decarbonization and a rapid transition to green energy systems.

Scenario 2: Faster transition

Last year, Japan and South Korea – following suit after China’s 2060 pledge – declared they would become net-zero emission countries by 2050. Japan, the world’s third-largest economy, gets a third of its energy from coal. Tokyo is considering shutting down or mothballing 100 aging coal power plants in the next decade or so. It will also stop – with some exceptions – its much-criticized financing of new coal power plants in developing countries. South Korea has announced it would close 10 coal plants by 2022 and 30 more by 2034.

Worldwide, renewable sources have grown in popularity due to their dramatically shrinking costs. Since 2010, the price of solar photovoltaic systems has decreased by 70 percent, wind energy by 25 percent and batteries for electric vehicles by 40 percent. Renewables now account for 25 percent of global electricity generation. By 2040, this could reach at least 34 percent, up to 50 percent by 2050. Solar and wind costs have been forecast to drop by an additional 71 percent and 58 percent respectively by 2050.

So that this scenario can come to pass, the expansion of renewable energy would have to keep up with electricity demand growth and the coal phaseout. The largest ever single-year increase so far in global renewable electricity generation was about 440 terawatt-hours, in 2018.

Currently, electricity makes up 20 percent of final energy demand, but this could rise to 70 percent by 2050. Investment in the power sector could nearly triple from $760 billion in 2019 to $2.2 trillion in 2030. The level of investment in renewables, rising to $1.1 trillion in 2030, is worth three times the largest amount earmarked in the past. Investments in nuclear power could also rise by nearly 80 percent.

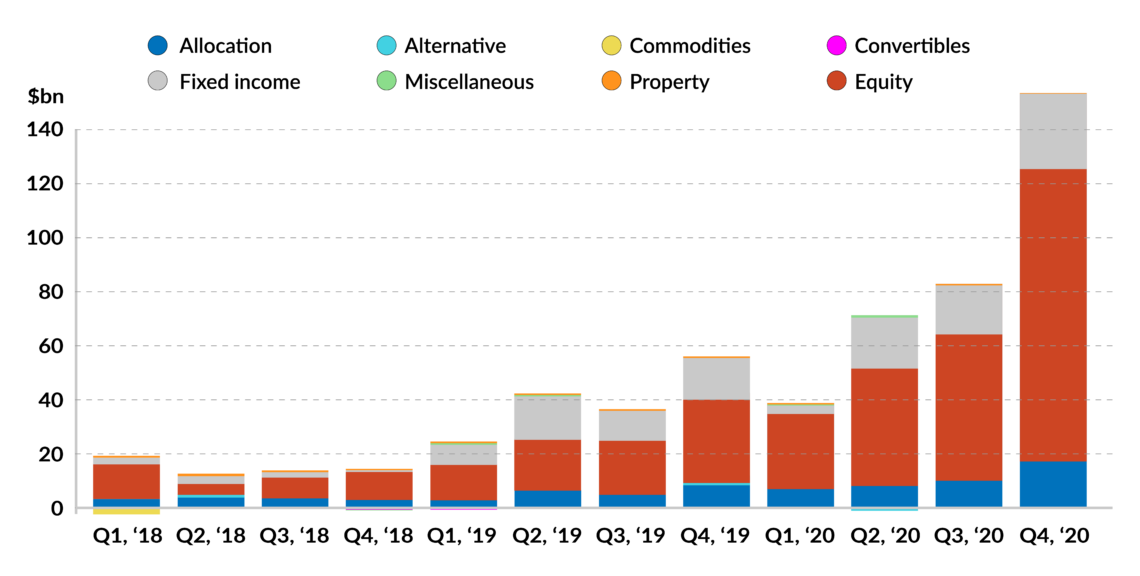

Energy markets are already undergoing a tectonic shift toward clean energy sources. In 2020, the green energy market was valued at nearly $350 billion, compared to $165 billion in 2019, and companies, governments, and households spent $500 billion on renewable energy and electric vehicles.