What’s wrong with the renminbi exchange rate?

Even before the most recent disagreement, the U.S. had already begun drawing attention to a new question: whether China had been engaging in protectionism by manipulating its currency. The argument reveals confused ideas about what the U.S. wants: a dominant role for the dollar or an renminbi to please American producers.

In a nutshell

- The Trump administration is criticizing China for exchange-rate manipulation

- The yuan, however, has not depreciated significantly against the dollar

- The West also engages in monetary policy that affects exchange rates

- Washington seems unsure whether it wants a strong or weak yuan

History will probably remember United States President Donald Trump’s current term for three reasons: an unprecedented bullish stock exchange that silenced all doomsayers, his drastic cuts in corporate taxation and his aggressive approach to trade policy that eventually made a significant breach in the Chinese wall.

The trade dispute between Washington and Beijing is not over, but most observers believe that a satisfactory compromise is not impossible. This would be good news for the entire world – so good that fears about a global slowdown have receded and optimism has been prevailing until very recently. Consistent with Mr. Trump’s pragmatic, comprehensive approach to trade matters, the administration has also devoted considerable attention to exchange-rate policies, a strategy that the Chinese are supposed to have used and could perhaps use in the future to mitigate the consequences of lower (traditional) trade barriers.

In simple terms, the economics of exchange-rate manipulation could be described as follows: By issuing and selling on the foreign-exchange markets large quantities of its own currency, the authorities of a given country weaken the domestic currency (depreciation). A depreciated currency cuts the purchasing power of domestic consumers but makes exporters happy (their goods become cheaper in terms of foreign currency). Domestic producers competing with importable goods are also better off, since the goods produced by foreign producers become more expensive when priced in the domestic currency.

If countries want China to finance their debt, they must accept that China buys dollars and euros to do so.

A depreciated currency therefore benefits both domestic exporters and import-competing producers. It does not need specific legislation, does not break any free-trade rules and is easy to justify by hiding behind the shield of a country’s undisputed right to monetary sovereignty, which includes the freedom to print money. Furthermore, depreciation results from an expansionary monetary policy, a choice that the international community has often recognized as appropriate as the least painful response to a country’s structural problems.

Difficult argument

If one accepts that the central bankers in Beijing (or Frankfurt) resort to money printing to keep the economy going, it is difficult to object when part of that new money reaches the foreign exchange markets and the currency weakens. It happened to the euro during the past year, as the single currency depreciated almost 10 percent against the dollar. Why should one object if it happens to the renminbi? Moreover, the renminbi is issued by the only country that today can finance large amounts of public debt created by the rest of the world, including the U.S. If the rest of the world wants China to finance its growing indebtedness, it must accept that China buys dollars and euros to do so – and this could require sales of renminbi.

So, what can we expect? Will the Chinese taint President Trump’s victories on trade matters by engaging in exchange-rate protectionism? Or will they give in to American pressure and either refrain from carrying out an expansionary monetary policy or break the mechanism that transforms money supply increases into a depreciating currency? And what will be the consequences?

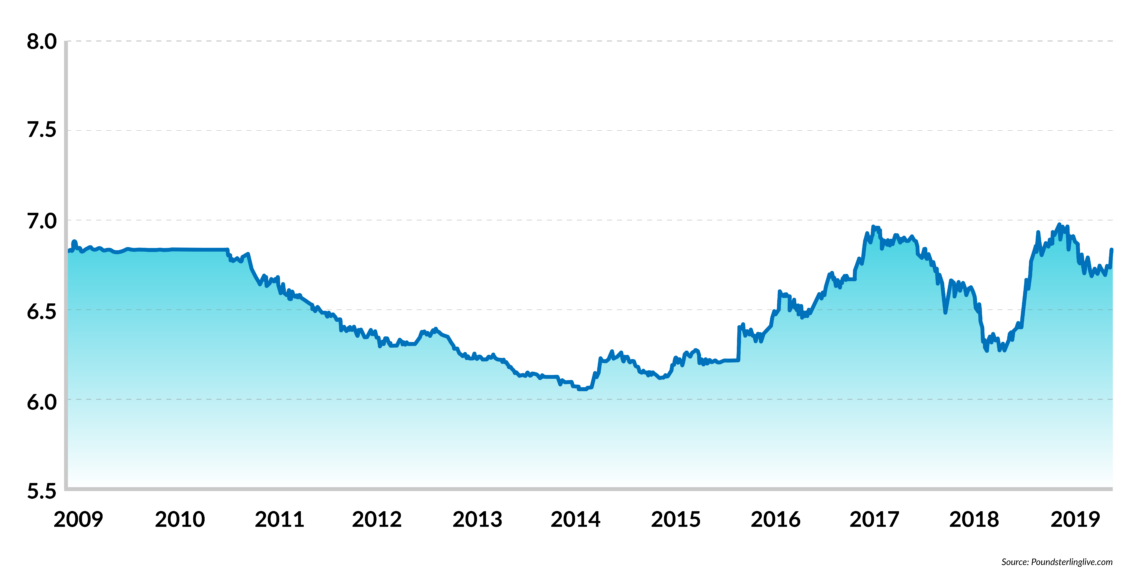

The data show that over the past decade, exchange-rate protectionism has been rather limited. Manipulation did not necessarily mean depreciation. At the end of April 2019, one U.S. dollar cost about 6.72 yuan. Ten years ago, it cost 6.82 yuan; five years ago, the renminbi was actually stronger (6.25 CNY to the dollar) and a year ago one needed about 6.30 yuan to buy a dollar.

Facts & figures

Long-term stability

Chinese yuan-U.S. dollar exchange rate, 2009-2019

In other words, the long-run trend of the dollar-yuan exchange rate shows stability, and the weakening registered during the past 12 months – about 6.7 percent against the dollar – is far from dramatic (less than the euro’s weakening). Put differently, the West cannot complain about deliberate devaluations. If anything, the European Union and the U.S. can complain because the Chinese do not let the renminbi appreciate. But of course, nobody can tell the Chinese how much money they can print; nor can anyone force the Chinese to stop resorting to the currencies they want to finance infrastructural projects around the world. The rhetoric about exchange-rate manipulation is an excuse.

Any future scenarios therefore depend on what the American administration is really asking the Chinese to do (or not to do). Monetary neutrality is not an issue. In recent decades, both the U.S. and the EU have been promoting aggressive monetary policies to stabilize their macroeconomic contexts. Although the outcome is questionable, they cannot reasonably ask the Chinese to refrain from doing the same thing.

Rather, it may be interesting to examine two different options, which lead to two sets of consequences. Under both scenarios, the name of the game is not stopping manipulation of the renminbi, but rather steering the renminbi in given directions, and serving new goals.

Global currency

The main scenario focuses on the possibility that the renminbi becomes a major global reserve currency. At the end of 2018, the dollar and the euro together accounted for over 80 percent of world reserves. The renminbi accounted for less than 2 percent. Yet, the situation could change if the Chinese insisted on handing out loans denominated in renminbi and possibly asking their trade partners to pay for Chinese goods in Chinese currency. Having a more balanced currency distribution of global reserves is not necessarily undesirable. However, the international demand for greenbacks would drop, and this would limit the Americans’ ability to pay for some of their imports with paper (dollars), rather than with their exports.

The debate on the strength of the renminbi is really a debate between the two souls of the American administration.

Within this context, the concern with the renminbi would have little to do with so-called “competitive devaluations,” but rather with the various roles played by the renminbi on global markets. It would be a problem not of devaluation but of prestige (and appreciation). Consistent with this perspective, we can expect the Chinese to put up face-saving opposition to Washington’s requests not to let the renminbi slide, and eventually give in to the American pressures – which is exactly what the Chinese meant to do in the first place. Of course, the other side of the coin is that this is bad news for countries burdened with renminbi-denominated debts. Most exposed would be some African and Asian countries, and also those more heavily involved in the Belt and Road Initiative – Italy and Peru being the latest members to have joined the club.

U.S. debt

A second scenario would draw attention to the American need to finance growing public debt, which is currently more than $22 trillion – over 105 percent of gross domestic product (GDP). China holds $1.13 trillion, about a quarter of the amount held by non-American creditors. However, Chinese holdings of U.S. debt are declining, and the Treasury Department may have begun to worry. If China stopped buying treasuries, America should look for other buyers and presumably offer them higher interest rates, much to President Trump’s dismay. Of course, the fewer treasuries the Chinese are buying, the weaker the dollar against the yuan: this is good news for American exporters, but bad news for those who fear the Chinese currency could have a major role in international markets.

The upshot is that the debate on the renminbi’s strength (and currency manipulation) is really a debate between the two souls of the American administration: one would like to help American exporting and import-competing industries, and one worries about financing the U.S. public debt and the global role of the dollar.

It is hard to predict how much the rhetoric of manipulation will make headlines. It is easy to foresee, however, that as long as the West insists on blaming the Chinese for currency manipulation, Beijing is free to focus on dealing with competition from the new, low-cost producers. These producers will determine where the renminbi will be going, not the complaints raised by the West.