GameStop and the future of financial markets

The story of what happened with GameStop shares in January is simple: certain investors made the wrong bet and lost. The market worked just as it should have. Regulators and many established financial players do not see it that way, though.

In a nutshell

- Regular investors took risks on GameStop shares and won

- Regulators and powerful investors now feel threatened

- Both may try to limit regular investors’ freedom

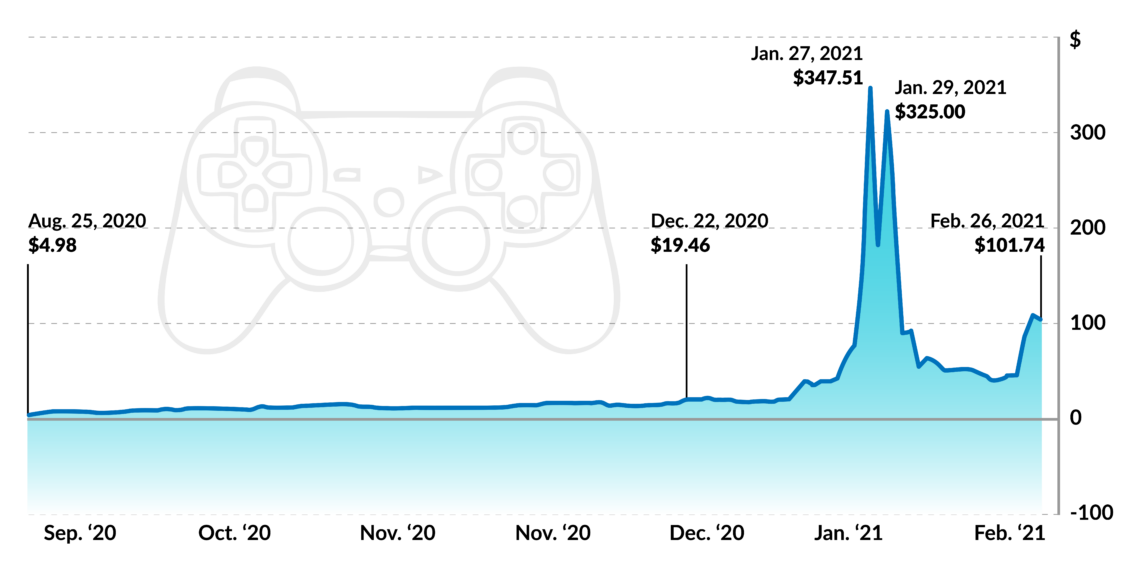

What happened with GameStop shares earlier this year is a simple story. In 2020, the United States-based video game retailer was considered a weak company with a bleak future. A small number of powerful investors thought that its shares, selling for about $19 apiece in late December that year, were overpriced. The company’s shares had cost about $27 in early 2016, from whence they steadily fell to about $4 in mid-2020.

The powerful investors expected GameStop shares to resume their trend downward soon and increasingly sold them short. In other words, they speculated that the GameStop share price would fall and acted accordingly, hoping to reap large profits. The strategy was not unreasonable, since GameStop was indeed a troubled company: it was on the verge of bankruptcy, and it seemed there was no company willing to act as the white knight, to buy it or invest in it, injecting new funds into the beleaguered firm.

Facts & figures

Short selling

Short selling is an investment strategy in which a trader expects a stock or other security to decline in price. Typically, the traders commit themselves to selling shares of the asset to buyers at the current market price. Yet, delivery takes place in the future and the sellers buy the shares they must deliver sometime before the agreed deadline. Thus, the trader is betting that before the shares must be given to the buyers, the price will decline, allowing for the asset to be purchased at a lower cost and providing the trader with a profit.

Then something unexpected happened. A few people noticed that the short selling had reached enormous proportions and that many of the investors betting against GameStop would soon have to buy the shares they had promised to deliver. This information circulated on social media and people began acquiring those shares, waiting for the short sellers to enter the market, buy, and drive up the share price.

Those who ambushed the short sellers were rewarded for their patience: prices started rising as the short sellers rushed to cover their positions. By the end of January, GameStop shares were trading for $482. It was a financial bloodbath for those who had bet against the company, while those who predicted that the short sellers would panic buy reaped gains.

However, those who bought GameStop shares near their meteoric highs at the end of January also took heavy losses. They forgot or were unaware that the company was troubled. By mid-February, GameStop shares had fallen back to about $50. Yet the volatility continued, and they rose to about $100 by the end of the month.

Nonexistent problem

This episode has no normative implications. The fact that the short sellers thought that GameStop shares were overpriced is neither good nor bad. Individuals are free to make their own judgments about a company and to make mistakes in doing so. Moreover, as long as people are not engaging in a criminal enterprise, they can do what they want with their own money.

Facts & figures

This applies to everyone: not only the seasoned market players, but also those who rightly believed that the short sellers had gone too far. That some of these people were novice traders and knew little or nothing about GameStop and financial markets is irrelevant. People should not need a PhD to engage in such transactions, nor should they have to have a high IQ to act as they deem fit.

This is not how regulators and policymakers see the picture. Two lines of thinking have gained traction with them over the past few weeks.

First, many officials believe that paternalistic regulation should intervene whenever there is a shock or prices oscillate significantly, as if the ideal economy were one in which everything moves at a snail’s pace. It is the rhetoric of equilibrium, which ultimately claims that the ideal world is frozen. In this worldview, investors are considered stupid if they make mistakes (for example, if they believe that a stock is overpriced), other investors are deemed ignorant if they have divergent opinions, even when they are right (like the “novice” traders in this story), and those who made the initial mistakes are irrational if they act to limit the damage. All this is patent nonsense, but it also happens to be the driving ideology behind financial regulation. This is not just bad economics. Shaping policies based on these claims benefits certain groups and harms others.

Second, some academics argue that all these alleged problems result from financial illiteracy and that more public money should be devoted to educating prospective investors. That is a fair enough point. Many people do not know much about the mechanics of compound interest rates, let alone derivatives. But it is worth wondering whether the difficulties in dealing with percentages and compound interest need new government programs or simply reveal the shortcomings of educational systems. It is also worth asking whether these deficiencies have really prevented people from understanding what they were doing when taking out a mortgage or asking for a consumer loan.

Certainly, what people knew was enough to ensure they would eschew negative-interest rate treasury bonds and understand that the main alternatives to a manipulated bond market are remaining liquid or taking chances in the stock market. Once again, this concern for literacy may be less innocent than meets the eye.

Positive role

The second topic raised by the GameStop episode regards the virtuous role that large numbers of “illiterate” traders and investors will play in the future. Absent government intervention and manipulation, financial markets are vital in two respects: they allow companies to borrow and develop their business, and they are the instrument through which information is created and circulated. For example, the rise in the price of stock X signals that people believe that company X is on track to improve its profitability, while a decline in price signals concern about the company’s prospects.

Nobody knows the future, and nobody knows how much a company is worth. One can guess or follow those who guess, but all accept that they are taking risks. If GameStop shares were to stabilize at their end-February level (about $100), most of those who sold their shares short when they were quoted at $100 or lower will have lost. The same applies to those who bought the stock when it was above that price – and they were many.

In this case, ‘illiterate’ traders turned out to be smarter than professional, highly specialized asset managers.

The story is simple: massive short selling at 10-18 dollars drew attention to the fact that a few large operators – possibly a cartel of operators – might have gotten it wrong and that money could be made by trusting other evaluations. Incidentally, the assessment was timely because GameStop was, in fact, about to announce major changes (new strategies and possibly new partners). Social media therefore allowed “illiterate” traders to make an impact and spread useful information. In this case, many such traders turned out to be smarter than professional, highly specialized asset managers.

Squeezing the middleman

The GameStop saga also sheds light on the future of asset management. There is a bevy of vastly overpaid financial “experts” who take pride in not falling too far behind their benchmarks: financial promoters, passive fund managers, dull-minded advisors, traders who simply operate computer programs but do not bother with the details. A new, polarized business environment could threaten these people’s positions.

If the GameStop story is the beginning of a new way of doing business, future investors of all sorts (both the financially sophisticated and the unskilled) will acquire the information they need and operate on the internet, while suppliers will be under severe pressure to do well and offer high-quality insight, lest they lose their reputation.

The winners will be the public at large, and the relatively small number of professionals who do their research properly, looking at the true-life of industries and companies, rather than just contenting themselves with leafing through reports while at the office or playing around with technical analyses.

Scenarios

The losers will be those who enjoyed a monopoly-like market dominance guaranteed by regulation, like banks and asset managers. Those actors for whom collusion is an opportunity to make easy profits, for example by driving stock prices up or down through long or short selling, will also lose out.

Pressure groups will dig in and encourage regulators to maintain or expand appropriate barriers to entry and keep competition at bay. Regulators will be happy to oblige, expanding their own power in the process and justifying their position.

The rhetoric of financial literacy may also serve regulators by leading to financial licensing. Individuals would be required to obtain such licenses just to make their own financial decisions. All this would create jobs for teachers and regulators. It would also reduce competition. Yet this nightmare could be not that far away.