Asia’s push in international trade

The 2020 proportional decline in trade was twice as large as the decline of world GDP – but as Asia leads the post-pandemic recovery of trade flows, a strong rebound can be expected.

In a nutshell

- Asian trade flows will grow faster than anticipated

- Policymakers have begun to remove some roadblocks to trade

- Europe will face new opportunities for trade and growth

This GIS 2021 Outlook series focuses on the opportunities that stem from the upheaval of the past year.

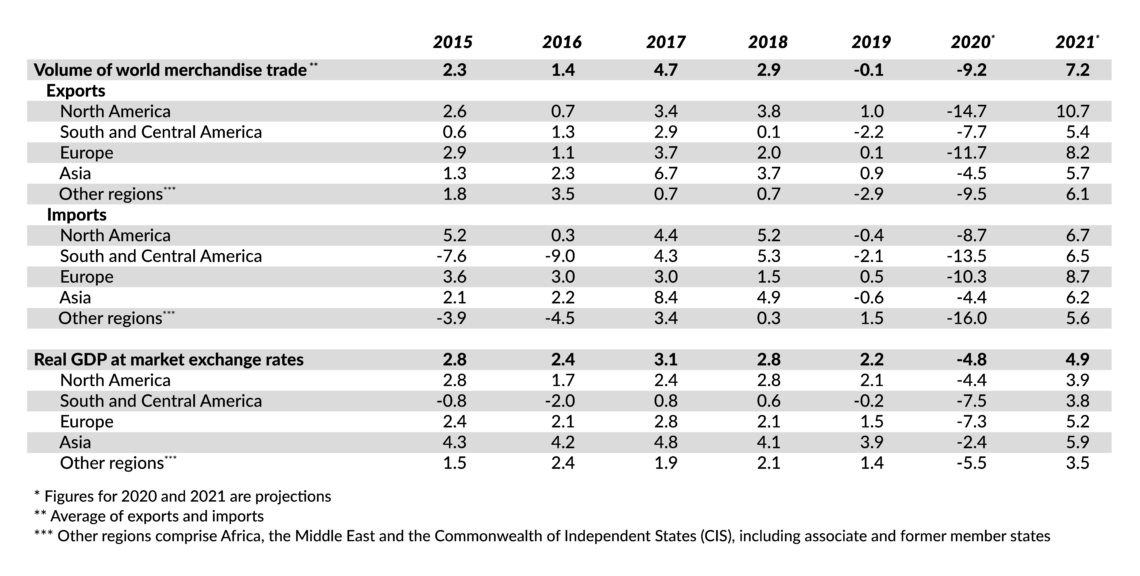

International trade in 2020 took a hit. According to World Trade Organization (WTO) estimates, global merchandise trade has dropped by about 9 percent and will “only” increase by about 7 percent in 2021. In other words, the 2020 decline in trade was twice as large as the decline of world gross domestic product (GDP), while the rebound will be only 50 percent stronger than that of GDP. As expected, the 2020 fall is steeper in the West than in Asia, but the rebound is also expected to be stronger in the West than in Asia.

All this data invites various “what if” exercises, most of them based on how trade reacts to GDP changes. This report takes a different view in two respects.

First, it assumes that GDP will not pull trade, but the other way around: international trade will drive (or slow down) post-pandemic global growth. Hence, we posit that Asian trade flows will grow faster than anticipated. Second, much will depend on how Western policymakers and entrepreneurs react to the pandemic’s challenges. The emphasis is on trade policy, delocalization and supply chains. Let us examine these two sets of issues in turn.

Potent engine

Economics is about exchange. As Max Weber wrote some 100 hundred years ago, communities always try to improve their material well-being, regardless of culture, geography and race. The key to success and higher living standards is exchanging and meeting other people’s needs. In particular, trade opportunities expand the range of potential buyers, smooth local shocks and reduce uncertainty. In this light, exchange encourages individuals’ efforts to increase education, specialization, productivity, long-term investments and wide-ranging cooperation.

A worldwide business environment is required to turn a crisis into a fresh start.

Economic growth occurs if producers believe that they are confronting a broad market consisting of millions of people who do their best to engage in production and expand their purchasing power.

In healthy economies, a crisis provokes a unique drive to start again, factoring in new knowledge of what it takes to succeed. A worldwide business environment is required to transform a crisis into a fresh start. It consists of such components as free trade, large companies, long-term commercial and engineering projects, stable and, if possible, light rules of the game (regulation and taxation). Of course, the barriers that prevent the world of business from taking advantage of 2021’s opportunities must be removed and the spirit of unfettered competition must prevail.

Removing roadblocks

Trade offers opportunities and incentives. As such, it is a necessary condition for recovery. But it will not suffice if people consider trade flows a potential threat. From this viewpoint, the good news is that policymakers have taken steps to undo at least some of the trade restrictions that have piled up over recent years. They are not always breakthroughs. For example, it will take time before the African Continental Free Trade Area, effective as of January 1, 2021, generates results. Yet, the project signals a shared acknowledgment that the way out of the crisis is not local self-reliance but tighter interdependence on a broad scale.

Likewise, the recent Brexit deal is far from perfect, as it does not shield the service sector – including banking and finance – from discriminatory treatment. However, it secures free trade in merchandise between the United Kingdom and the European Union and allows the UK to develop new free-trade arrangements with the rest of the world.

Facts & figures

China has gone much further. Last November, Beijing sealed the largest free-trade agreement in decades, including China and 14 other economies in Asia. Moreover, at the end of December, China’s President Xi Jinping signed a groundbreaking agreement that makes it easier for EU entrepreneurs to set up new companies in China, including in high-tech industries. In exchange, the EU will lower barriers against China in the energy sector. Ratification will take place in 2021.

Opportunities emerge

If this pro-trade trend is confirmed, growth will gather speed in China, and opportunities will open up for Europe. The new American administration, too, will be facing novel and partially unexpected choices. Former President Donald Trump’s trade policy did not achieve much, and his crusade against unfair trade practices added to unnecessary tensions with America’s European allies. It will be interesting to see how the new administration responds to the current prevailing pro-trade wave.

China has shown its global commitment and cold-shouldered American requests for a radical bilateral deal, while the Europeans have ignored the U.S. call for more cooperation in tackling global trade issues. In other words, Washington has lost the initiative, and this plays in favor of post-pandemic global trade-led growth.

Asian economic growth has been faster than in the rest of the world.

A different set of issues regards the likely forms of future trade. This report emphasizes the role of foreign direct investment (FDI) and supply chains. This kind of investment will intensify, and the range of opportunities will expand.

Last year taught business many lessons about production and consumption. The Covid-19 pandemic has disrupted freight transportation, and rates have soared, especially for air transport. It pays to develop production capacity close to consumers. Decisions along such lines will take into account economic growth prospects, distance, input costs and the scope of specialization (the fragmentation of the production process). For now, Asia seems to be a likely winner on all accounts.

During the past decade, Asian economic growth has been significantly faster than in the rest of the world. Also, the region’s ability to react to crisis has been vastly superior. In the West, regulation, tax regimes and ideological biases against large corporations have become a heavy burden. Extensive bailout policies have prevented bad companies from going broke and made it difficult for more efficient producers to see the light and expand their market shares.

Producers strategies

This situation explains why post-pandemic global growth will be led from the East: producers will probably strive to enhance their facilities in Asia. That means more investment, of course. It also means more trade, as those new production facilities will be primed to meet global demand. The cost of inputs will also encourage relocation toward Asia. The rise of labor productivity there has been fast enough to compensate for the increase in wage rates. The supply of more and more qualified workers is expanding relatively fast. China’s continental infrastructure-building program has elicited the participation of nearly all significant players in the region. This massive project will likely translate into fewer disruptions and lower transportation costs.

Ramping up innovation requires deregulation and a less hostile attitude toward big business.

Given this large picture dominated by global investment strategies designed to deliver more and more final goods to local consumers, new patterns in supply chains could bring about new trade opportunities. Nobody knows yet what kind of approach to industry and trade the new U.S. administration will take. Lack of a clear strategy and ongoing rhetoric from Washington that emphasizes heavier taxation, “sustainable” growth and environmental concerns mean that producers will bide their time. In contrast with the Trump years, therefore, America is unlikely to take the lead soon. On the other hand, Germany and the EU have taken a more active stance: the December quasi deal opens up some avenues.

Scenarios

Flows in fixed investments (facilities) will be one of these. Yet, it is easy to predict that enlarged markets for reliable, high-quality suppliers to Asia-based plants will open up. This amounts to a new source of trade flows. In partial contrast with the past, when Western producers were looking for cheap Asian suppliers, in 2021, we could start having Asia-based producers looking for critical suppliers in Europe and, to a lesser extent, in the U.S.

Call for innovation

These trade patterns will present new challenges and confirm old bottlenecks. For example, European producers need to be more innovative: their competitiveness depends increasingly on their ability to develop new technologies and business models. The current pro-trade environment will make their efforts more profitable than in the past and ease the transition toward new patterns of cooperation with trade partners.

However, ramping up innovation requires deregulation. And it also calls for a less hostile attitude toward big business and the dynamics of large companies (mergers and acquisitions). The key to European competitiveness will be speed and flexibility. The Europeans will not ignore the new U.S. administration’s concerns, but they will not let them become a straitjacket.

Call for a stable financial sector

Of course, the forthcoming rise in trade flows will also affect services like banking and finance. Ongoing cooperation – free trade – in financial services between the EU and the UK will play a crucial role. Brexit has left ambiguities in this area.

There is no doubt that successful trade depends on efficient banking and that the fast reshaping of selected industries needs innovative financing and pioneering financial entrepreneurs. That is why a pro-trade Brexit solution in financial services is vital. It will help dismantle excessive regulation and technocratic illusions in this critical industry and expand the opportunities that the new, bold, post-Covid political attitude is creating.