Prospects for two-tiered banking regulation in Europe

Complex and lengthy banking rules in the EU are putting a burden on small lenders. Some propose a two-tiered system in which the large banks must follow the most stringent regulations, while simpler, less complicated rules apply to the smaller players. Such a system is already being used in the United States. Could Europe follow?

In a nutshell

- EU banking regulations are complex and expensive to comply with

- This situation inherently favors large banks, which can absorb the costs

- Some regulators argue for a second, lighter set of rules for smaller lenders

- Creating such a framework would challenge the push for a “unified” system

Over the past two years, European Union authorities have begun considering the issue of “proportionality” in banking regulation and supervision. The question is whether to continue the current one-size-fits-all approach. Should regulators impose the same rules across the entire spectrum of financial institutions or adapt rules to the specifics of banks – their size, complexity and relevance for financial stability? The idea is that smaller, less risky banks should be subject to simpler rules than the large, globally active, systemically important ones.

U.S. initiative

This new debate gained traction in Europe after the Trump administration announced the introduction of a two-tiered regulatory system in the United States. Under this system, big and small banks play by different sets of rules. The purpose of the federal government is to alleviate costly regulatory burdens, especially for community banks.

Such institutions provide essential services to small businesses, consumers and the local economy in general. Their viability is threatened by many of the restrictive provisions of the Dodd-Frank Act, passed by the Obama administration in 2010 in response to the financial crisis of 2008.

Dismantling this largely unfavorable banking regulation is the goal of the Financial CHOICE Act. Signed into law by President Trump in May 2018, the legislation is supposed to provide regulatory relief to small American banks (those holding assets below $250 billion).

It is too early to tell whether, like their U.S. counterparts, EU policymakers have come around to the idea of easing financial regulations for small banks. But by simply getting off the ground, the debate indicates that at least some understand that the regulatory overdrive of the past decade might have done more harm than good for a key part of the banking sector.

Launching a two-tiered system would be a big step forward in addressing some of the most obvious adverse effects.

Launching a two-tiered system of banking regulation in the EU would be a big step forward in addressing some of the current regime’s most obvious adverse effects. Doing so, however, would pose major challenges in terms of both theoretical justification and practical implementation.

‘Single rulebook’

Many obstacles stand in the way. First, the proportionality argument seems at odds with the EU’s basic regulatory logic, according to which all policy actions should have the goal of ensuring the system’s “uniformity.” EU banking regulation, in particular, has from the start aimed to create a unified regulatory framework that would complete the “single market” in financial services.

The backbone of the (still not entirely finalized) Banking Union is the so-called “single rulebook,” which is supposed to assure a uniform application of international standards, such as the Basel guidelines, to all banks, in all member states of the EU.

Facts & figures

The ‘single rulebook’: key elements

The most relevant legal acts that constitute the single rulebook are the Bank Recovery and Resolution Directive (BRRD), the Capital Requirement Directive (CDR IV), the Capital Requirement Regulation (CRR) and the amended Deposit Guarantee Schemes Directive (DGSD). It is up to the technocrats of the European Banking Authority (EBA) to ensure that homogeneous interpretations are given to this body of legislative texts and that the same methodologies are applied. The EBA provides a myriad of “binding technical standards” (BTS), which are legal acts in their own way, specifying or clarifying aspects of the various directives and regulations that make up the single rulebook.

The single rulebook architecture builds on three institutional pillars, of which only the first two are fully operational so far: the Single Supervisory Mechanism (SSM), the Single Resolution Mechanism (SRM) and, still under construction, the European Deposit Insurance Scheme (EDIS).

Supervisors across the EU are trained by the European Banking Authority (EBA) to create a common foundation and culture for supervision. The underlying philosophy is that only if all actors speak the same language, use the same methods, understand rules in the same way and cooperate among themselves, can the European regulatory and supervisory process move toward the desired unity. For this purpose, the EBA annually publishes guidelines on common procedures and methodologies for the “supervisory review and evaluation process” (SREP).

By this, authorities want to avoid misunderstandings or discretionary interpretations of EU law by member states, and even more, the inclusion of vague provisions, exemptions, exceptions or other forms of special treatment that could distort the rules. Their aim is to reduce the number of regulatory loopholes that financial institutions could exploit.

Taking regulations further

The original Basel requirements, at the basis of the EU’s single rulebook, had been designed foremost for large, internationally active and systemically important financial institutions. The Basel Committee on Bank Supervision (BCBS) therefore acknowledges the principle of proportionality.

By choosing to apply the Basel rules to each and every European bank, no matter its size, complexity or systemic relevance, EU legislators deny this principle, in hopes of providing certainty and stability for the benefit of the “whole” banking sector.

The unified regulatory framework for the EU financial sector appears to privilege particular types of business models.

Similarly, the common international standard on total loss-absorbing capacity (TLAC), designed by the Financial Stability Board (FSB) in cooperation with the BCBS, only applies to the 30 financial institutions worldwide identified as “Global Systemically Important Banks” (G-SIBs). The idea is that, if one of these big banks were to fail, it could rely on an adequate amount of liabilities earmarked for loss absorption and recapitalization, which can be rapidly converted into equity, so that the continuity of the bank’s critical functions can be assured and a systemic crisis avoided. TLAC is to be phased in this year.

Moreover, in 2014 European regulators introduced (as part of the Bank Recovery and Resolution Directive) a minimum requirement for eligible liabilities (MREL). Here again, the EU is going further than the international standard-setters, by imposing MREL on each of the approximately 6,250 credit institutions currently operating in the EU.

Subsidizing ‘too big to fail’

Deliberately or not, the unified regulatory framework for the EU financial sector appears to privilege particular types of business models: namely large, international, shareholder-based commercial banks – precisely those that were at the epicenter of the global financial crisis 10 years ago.

These banking groups have the pecuniary and human resources necessary to adapt to the increasingly complex and stringent requirements of postcrisis regulation. They can afford large compliance departments, with sometimes several hundred highly specialized officers, solely dedicated to this task. They have the means to develop sophisticated strategies in financial engineering or to acquire so-called RegTech (regulatory technology) solutions, allowing them to minimize compliance costs. If necessary, they can relocate their headquarters to parts of the world where regulatory obligations are less severe. In any case, their lawyers can help them circumvent the most unfavorable provisions, by exploiting the loopholes that persist in the regulatory system.

Smaller, regionally-based banks cannot do any of this. They do not have nearly as much time and resources to dedicate to conformity assessment. Whether they hire dozens of additional employees for dealing with compliance, invest in high-level IT infrastructure or simply outsource parts of the work to expensive consultants, the result is the same: their fixed costs rocket, as regulations become more and more voluminous and complicated. As pointed out by the RegTech Council, the EU’s MiFID II alone (coming into force in January 2018) has generated approximately 30,000 pages of related texts in 1.5 million paragraphs, and has already cost the industry over 2.5 billion euros to implement.

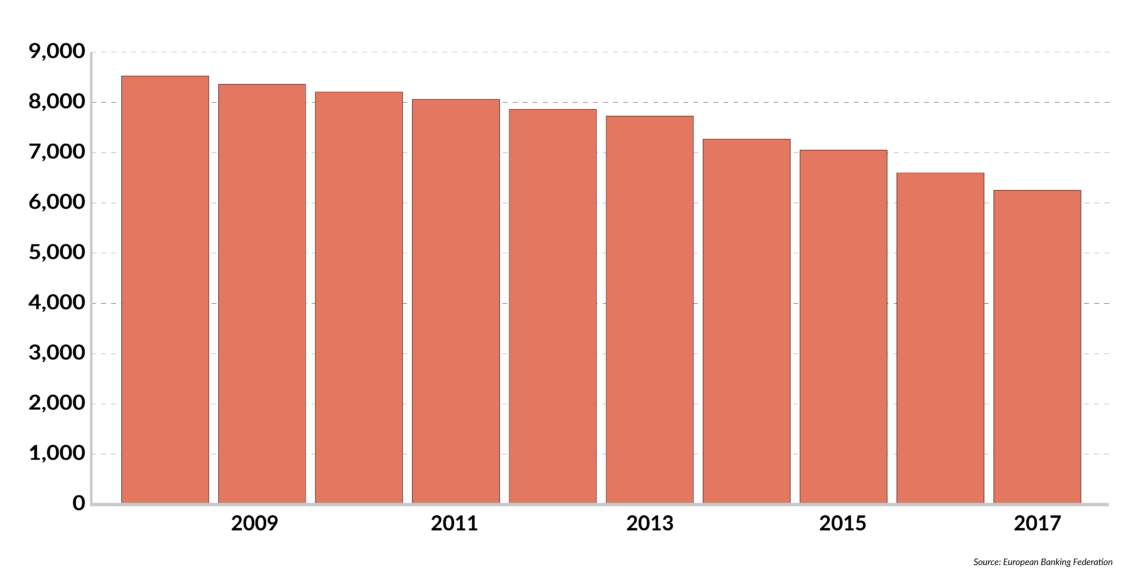

Facts & figures

Shrinking market

Number of credit institutions in the EU

(including those based inside and outside the bloc)

Financial professionals estimate that, on average, compliance costs will rise from 4 percent currently to 10 percent of banks’ revenue by 2022. For the smallest banks, the percentage is likely to be significantly higher, as they cannot benefit from economies of scale. Much of their compliance budgets is spent on merely understanding and interpreting the constantly changing rules; more goes into monthly reporting to supervisors, not to mention stress testing and regular recovery and resolution planning (requiring the elaboration of so-called “living wills,” “playbooks” and “dry runs”). All this constitutes a tremendous workload, especially for ordinary bank employees who are not necessarily qualified to undertake these complex tasks.

Unsurprisingly, many small banks crack under the regulatory burden. In Germany alone, up to 70 banks close down or disappear through merger each year. During the past decade, the number of banks throughout Europe fell by almost 27 percent. Small banks’ share of the industry’s assets is shrinking by a similar proportion. Already today, the 120 major European banking groups have captured a combined 82 percent of euro area banking assets.

Even though regulation’s role in these trends has not been formally calculated, it is certainly significant. It is no exaggeration to presume that the unitary regulatory approach implicitly favors (or, one might say, “subsidizes”) banks with large, international organizational structures, while it clearly penalizes the small ones.

For many years, small lenders have formed the backbone of banking in most European countries.

Yet, for many years, the latter have formed the backbone of banking in most European countries. Notably in Germany, small cooperative and savings banks have always played a key role in financing local and rural economies. Their long-standing relationships with customers and companies, based on trust and confidence, constitute a valuable asset that is simply ignored by the EU’s strict, one-dimensional regulatory rulebook.

Worse, as German central banker Andreas Dombret warns, the EU’s one-size-fits-all regime “threatens the healthy diversity of the European banking landscape.”

Small banking box

Mr. Dombret is one of the most fervent advocates of the proportionality principle in Europe right now. Too much is asked of the small regional banks and it is time to relieve some of the pressure on them, he insists. Above all, the competitive disadvantage that regulation creates for these institutions must be taken seriously, before it irreversibly damages the European economy. As a potential solution, Mr. Dombret proposes a three-tiered approach, modulating regulation in proportion to the size and systemic relevance of banks.

First, for the (comparatively small number of) large, systemically important, international financial institutions, the constraining requirements of Basel II and III should remain fully applicable.

Second, the medium-sized and relatively low-risk banks should remain under the same regulatory framework but see a few of its key measures relaxed. Mr. Dombret recommends that they be required to report less frequently (say, quarterly instead of monthly) and provide fewer data points (by making the data less granular, or allowing the banks to use simplified templates, for instance).

Third, the small and noncomplex institutions – those that suffer most under the weight of EU banking regulation – should receive special regulatory treatment. In addition to easing their reporting procedures, small banks could be exempted from recovery and resolution planning and face reduced disclosure requirements. They should be subject to a completely separate set of rules, tailored to fit their needs, says Mr. Dombret, who dubs this new framework the “small banking box.”

Small and simple

Sometimes, “less is more.” Mr. Dombret tirelessly hammers home this message in his talks at EU regulators’ meetings. When applied to banking regulation, this slogan seems to make sense. Nonetheless, the small banking box comes with its own share of problems. How should regulators establish the threshold at which a bank is small enough to be included in the small banking box? What criteria should come into play: volume of total assets, market share, number of customers?

Also, size is not all that matters. Small banks too can become systemically relevant, if a large group of them joins together, for example, via holdings or cooperative structures. Risky activities can be conveniently hidden behind such frameworks. “Too many to fail” may be a problem of no less importance (at least on a national scale) than a few banks “too big to fail.”

To benefit from the special rules, banks must be “small and not too complex,” Mr. Dombret would respond. But then again, what are the criteria for evaluating the degree of a bank’s complexity? Obviously, the answer is not easy. In the end, it should “always rest with supervisors,” deciding on a case-by-case basis, Mr. Dombret suggests. The question is whether such a system is too discretionary for EU regulators to stomach.

Red lines

Another critical question is: What exactly is meant by “simpler rules” for smaller banks? Is it just about lessening their paperwork and administrative burdens? Or can it include a reduction of capital and liquidity requirements? More crucially, can we expect a two-tiered regulatory framework, similar to the one recently introduced in the U.S., to become reality in Europe sometime soon?

Sabine Lautenschlaeger, vice chair of the ECB’s executive board, concedes that there is “a strong case for proportionality” in Europe. A few measures in that direction have even been implemented at EU level over the past few years. For example, small banks now report “only” about 600 data points to supervisors, whereas larger banks have to report more than 40,000.

Whether such measures are a first step in the direction of a two-tiered regulatory system in Europe or merely the expression of a certain supervisory fatigue (supervisors also struggle with the huge volume of information reported to them by banks on a regular basis) is difficult to say.

In any case – and Ms. Lautenschlaeger is very clear about this – making rules less stringent, or allowing banks to hold less capital or liquidity, is a red line that she is not ready to cross. From the ECB’s point of view, easing financial regulation can only be a matter of practical details within the existing single rulebook, whose unitary thinking should not be compromised.

What the EU authorities really want is to keep pushing the consolidation trend in the European banking industry that started some 30 years ago and accelerated after the 2008 crisis. Europe is desperately “overbanked,” it is said in ECB circles, and the sector needs to shrink considerably more, either through merger or bank failure. The idea is to promote a robust banking sector with a few large, powerful, resilient players, operating under the strict oversight of the ECB. Needless to say, that increases the already enormous power in supervisors’ hands.

Eventually, Mr. Dombret’s biggest fear might come true: in 20 years, Europe’s economy could be “served by 50 ‘megabanks’ – all of them much too big to fail,” and certainly not interested in financing local development.

By then, a “small banking box” would no longer be necessary.