Is the European Central Bank still in control?

As eurozone inflation plunges citizens into a cost-of-living crisis, the ECB is sticking to its policy of cheap credit and adding a new bad-debt incentive for reckless governments.

In a nutshell

- The ECB can no longer deny that inflation in the euro area is a serious problem

- As interest rates rise, the bank’s leaders fear another sovereign debt crisis

- To fend it off, the ECB has rolled out a very controversial bailout program

Responding to rising eurozone inflation, the European Central Bank has designed (ECB) a new policy tool. Innocuously called the Transmission Protection Instrument (TPI), it is supposed to enhance the ECB’s ability to intervene when a widening disparity in borrowing costs between the eurozone’s most stable and most indebted countries threatens a fragmentation of the euro system.

The instrument is, in essence, a bond-buying scheme targeted to aid individual countries that the central bank deems at risk. This has advantages. However, by introducing TPI, the ECB is violating a fundamental principle of the European Monetary Union and may end up stoking up inflation rather than dousing it.

The reckoning

It took the ECB a year to acknowledge that the current high inflation is not just a “transitory” episode. For months, the institution tirelessly repeated that inflation would return by itself to the 2 percent target and even fall below it, once the problems of pandemic-related supply-chain bottlenecks and war-related energy shortages are sorted out.

However, euro area inflation keeps climbing, breaking record after record and plunging Europeans into the worst cost-of-living crisis in a generation. Meanwhile, annual inflation rates are creeping toward double digits and show no sign of peaking.

The negative rate policy, long celebrated as an anti-crisis wonder weapon, is increasingly seen as a monetary aberration that did more harm than good to the eurozone’s economy.

The ECB has had no choice but to follow the lead of other major central banks, such as the United States Federal Reserve (Fed) and the Bank of England, which started on the path of monetary policy normalization months earlier.

ECB’s hawkish talk

On July 21, 2022, for the first time in 11 years, the ECB announced it would raise its key interest rates by 50 basis points (0.5 percent) instead of 25 (0.25 percent), as initially indicated. Rates were increased once again on September 8, this time by an unprecedented 75 basis points. Further hikes can be expected in the coming months.

Even dovish central bankers now say it was high time to take rates out of the negative territory in which they had been stuck since mid-2014. The negative rate policy, long celebrated as an anti-crisis wonder weapon, is increasingly seen as a monetary aberration that did more harm than good to the eurozone’s economy.

ECB policymakers have started to acknowledge their failure to predict the upsurge of post-pandemic inflation, even though they contributed to its cause. To rebuild their credibility, they recently decided to break free from “forward guidance.” This monetary policy tool, introduced in 2013 by then-ECB President Mario Draghi, revealed itself as a straitjacket that, as ECB officials now admit, considerably limits their margin of maneuver if unpredictable situations occur.

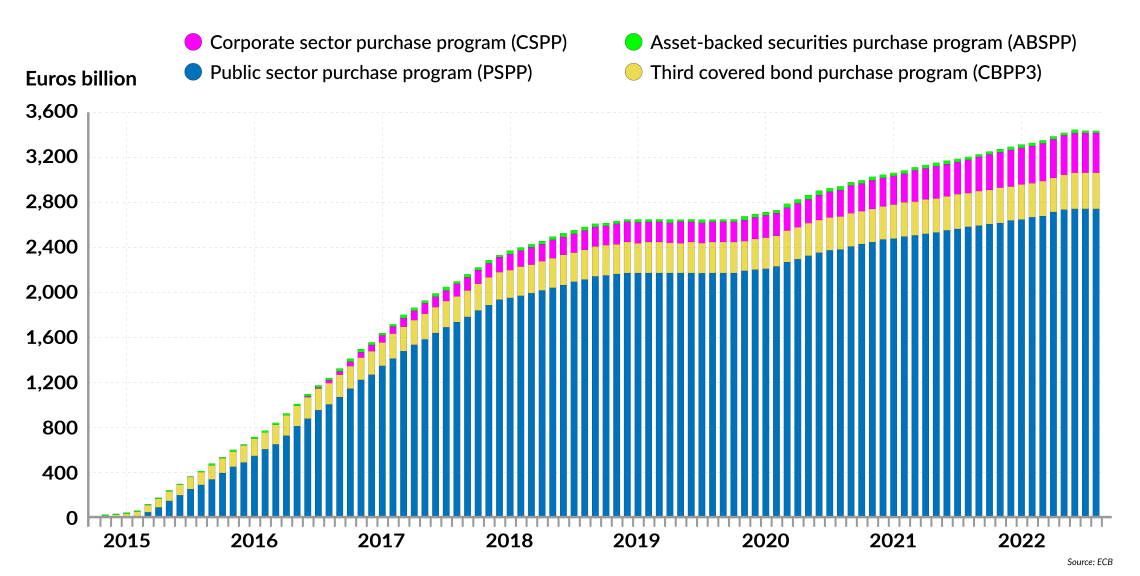

Facts & figures

APP cumulative net purchases, by program

The ECB has also adopted an almost hawkish stance by announcing the end of its long-running Asset Purchase Program (APP), launched under Mr. Draghi. In March 2022, the ECB’s other massive liquidity injector, the Pandemic Emergency Purchase Program (PEPP), launched two years earlier and scaled up to 1.85 trillion euros during the first year of the pandemic, came to an end, too. Moreover, the terms of the Targeted Longer Term Refinancing Operations (TLTRO) recently changed, making them less attractive for banks and leading to more credit-tightening in the eurozone.

Cheap money policy is not over

Slowly but surely, the process of normalizing the ECB’s monetary policy stance seems to have started. Does this imply that the era of cheap credit is over in Europe?

Not really. Net asset purchases under APP and PEPP may have ended, but reinvestment of these bonds will go on when they reach maturity. At the end of August 2022, the stock of Eurosystem bonds stood at 3.436 trillion euros. That is still plenty of money to keep monetary policy ultra-loose for a long time.

More importantly, for the reinvestment of PEPP proceeds (which will continue until the end of 2024 at least), the ECB is not bound by capital keys. In a press conference last December, ECB President Christine Lagarde suggested that “under stressed conditions,” her institution can freely decide when, where and how to reinvest the colossal treasure of government bonds it owns.

This positive discrimination could exacerbate tensions between peripheral and core eurozone nations.

“Flexibility” has become the new magic word, which allows the ECB to continue to cap spreads on the debt of certain, well-chosen eurozone sovereigns. Greece, Italy, Spain and Portugal could be in the lot.

This flexibility opens the door to a two-speed monetary policy. For member states that perform well and control their debt, the monetary policy screw will be tightened, whereas, for those that spend beyond their means, the money tap will remain open.

Put differently, those who play by the rules are punished, while those who do not are rewarded. This positive discrimination could exacerbate tensions between peripheral and core eurozone nations.

There is a reason why, two decades ago, the EMU architects insisted so much that all eurozone countries play by the same rules and be treated in the same way. Monetary policy should not deal with regional differences, it was stated. Rather, it should be applied to the eurozone as a whole. The ECB is breaking with one of the EMU’s core principles by introducing regional differences.

Containing bond market stress

The ECB’s biggest fear is that over-indebted sovereigns will end up facing exorbitant borrowing costs. That can happen when bondholders lose trust in a government’s ability to pay back its debt. When, as a result, a massive bond sell-off occurs, bond prices fall, and yields shoot up. The concerned government finds itself under even more pressure.

In the past decade, there were several occasions when the eurozone saw that investors’ fears could become self-fulfilling. One such episode led to the multiyear European sovereign debt crisis almost bringing down the euro in 2012.

Another happened on March 12, 2020, the day after the World Health Organization declared Covid-19 a pandemic. President Lagarde had sent European sovereign debt markets reeling back then with the words: “We are not here to close spreads. This is not the mission of the ECB.” Ms. Lagarde was referring to the suddenly widening gap between Italian and German 10-year government bond yields – a closely watched gauge of investor confidence.

During the Covid-19 outbreak, Italy’s debt suffered a rapid sell-off in key European markets. Investors feared that the pandemic could undermine what little was left of the creditworthiness of the already debt-stricken government. In this context, Mrs. Lagarde’s remark was interpreted as a refusal of the ECB to stand ready as a lender of last resort to Italy if the worst arrived, which triggered panic.

The ECB thinks that we could be heading toward situations in which bond reinvestment might not be enough to contain episodes of acute bond market stress.

For many observers, the ECB chief’s words augured a breach of the “whatever it takes” commitment to save the euro, famously uttered by her predecessor Mr. Draghi during the eurozone crisis.

In March 2020, what had started as a fire on eurozone bond markets could have turned into an uncontrollable inferno had Ms. Lagarde not rapidly backpedaled and presented her apologies for a “mistake” or, rather, a “communicational blunder,” apparently due to fatigue. Markets eventually calmed down, not least because, a week later, the ECB unveiled the most generous stimulus package in its history, the PEPP.

TPI copy and the original

Now the PEPP is gone – at least the net purchases part of it. Yet, the ECB thinks that we could be heading toward situations in which bond reinvestment might not be enough to contain episodes of acute bond market stress.

That is why a new anti-crisis tool, TPI, has recently been designed. It will take the form of a specific bond-buying scheme.

The ECB closely watches the gaps in borrowing costs between the euro area’s strongest and weakest countries. In case spreads widen “dangerously,” the bank stands ready to buy unlimited amounts of debt of the country whose servicing costs are rising.

Shortly before the TPI was unveiled, President Lagarde declared, “We will not tolerate fragmentation that would impair monetary policy transmission, and we will determine on the basis of circumstances, of countries, how and when that risk is likely to materialize, and we will prevent it.”

The TPI is reminiscent of the Outright Monetary Transactions (OMT), created by Mr. Draghi in 2012. Under that emergency program, the ECB agreed to act as a market maker of last resort by buying the debt of a country that is facing exorbitant servicing costs.

However, strict conditions and fiscal responsibility rules were attached to that constraining “macroeconomic adjustment” program, which can be seen as a bailout procedure in all but name. The OMT involves not only the ECB but also the European Financial Stability Facility/European Stability Mechanism (ESFS/ESM) and the International Monetary Fund (IMF). The OMT was never implemented, but it backed Mr. Draghi’s famous “whatever it takes” statement.

Moral hazard

President Lagarde wants the TPI to know the same fate. She said she hoped it would never be used. The idea of creating a facility that allows the ECB to act as a buyer of last resort when market liquidity is drying out in sovereign debt markets makes sense. But why create a new one when the OMT is still part of the toolkit?

Italy may be the first test case for the TPI. The country’s future looks deeply uncertain after Prime Minister Draghi’s government collapsed in July 2022.

The answer is that the TPI comes with much looser conditions than the OMT. Virtually every eurozone government is eligible for the TPI. That could be advantageous. For instance, rapid action and intervention flexibility can reduce situations of acute sovereign risk.

The downside is that it encourages fiscally fragile governments to continue on the path of excessive debt without engaging in structural reforms.

Facts & figures

The OMT’s eligibility conditions are strict

- A necessary condition for OMT is strict and effective conditionality attached to an appropriate European Financial Stability Facility/European Stability Mechanism (EFSF/ESM) program.

- Such programs can take the form of a full EFSF/ESM macroeconomic adjustment program or a precautionary program (Enhanced Conditions Credit Line), provided that they include the possibility of EFSF/ESM primary market purchases.

- The involvement of the [International Monetary Fund] shall also be sought for the design of the country-specific conditionality and the monitoring of such a program.”

TPI conditions are easily fudged

The TPI’s eligibility requirements do not mention the IMF or the need for conformity with an appropriate EFSF/ESM program. It has only three main criteria, pointed out Willem H. Buiter, a former member of the Bank of England’s Monetary Policy Committee in a comment titled, “Will Europe’s New TPI be an ATM?”

- The member-state government must be in compliance with the EU fiscal framework, meaning that it is not subject to an excessive-deficit procedure and has not failed to take effective action in response to an EU Council recommendation.

- The government must exhibit an absence of severe macroeconomic imbalances, meaning that it is not subject to an excessive-imbalance procedure and has not failed to act on an EU Council recommendation.

- And it must demonstrate fiscal sustainability, based on debt-sustainability analyses by the European Commission, the ESM, and the IMF, among others.

“The problem with these conditions is that they are easily fudged,” cautioned Mr. Buiter. His conclusion: “[F]iscally fragile eurozone governments have been reluctant to submit to the OMT’s eligibility conditions. The TPI offers superior financial support with minimal conditionality. Guess which one will prevail.”

In the end, it does not even matter whether the TPI is used or not. The fact that it is there, backed by the ECB’s promise to be the buyer of last resort, is enough to create bad-debt incentives. Worse, it can lead reckless governments to put the ECB under pressure simply by taking on unsustainable debt.

In short, the TPI can come at the cost of fiscal capture. Ultimately, the ECB’s independence is at stake. Italy may be the first test case for the TPI. The country’s future looks deeply uncertain after Prime Minister Draghi’s government collapsed in July 2022. Since February 2021, the man who once “saved the euro” and put an end to Europe’s worst sovereign debt crisis incarnated trust in Italy’s capacity (and willingness) to find ways to pay back its 2.75 trillion euros debt pile.

Now that he is gone, Italy’s creditworthiness could be over the cliff sometime down the line, notably if some post-fascist/populist party gains power. Allowing an irresponsible government to pursue reckless fiscal policies would also end up crippling the credibility of the ECB. If the TPI was about preventing sovereign debt crises, it could fall short. Creating incentives for governments to fiscally misbehave inadvertently produces new conditions for a sovereign debt crisis.

Scenarios

Eroding the euro

There may be a case for using QE tools in ultra-low inflationary or deflationary contexts, which was the situation over the past decade. But in the current environment of high and persistent inflation, introducing a new net bond-buying scheme that comes on top of flexible (or, rather, discretionary) bond reinvestment to support ailing eurozone governments adds fuel to the fire, as such policies are inherently inflationary.

Over the past 10 years, the ECB has been criticized for overstepping its price stability mandate. Each time, however, the issue has been discarded or downplayed by the European Court of Justice. It always sided with the ECB.

Now it has become blindingly obvious that the ECB’s job has changed along the way. It is more about financing fiscal policy than preserving the euro’s purchasing power.

The TPI could become the perfect instrument for ensuring (and at the same time hiding) that incompetent states can pursue the path of public debt.

Watch your wallets

Spanish economist Daniel Lacalle has noted that denouncing this shift in the ECB’s mission is not anti-European. It is all the opposite; indeed, pursuing a policy of inflation in a persistent inflationary context is a way to weaken the euro.

The ECB’s new toolkit risks undermining what Mr. Lacalle calls “the greatest monetary success of recent history, the euro.”

The EMU system was designed precisely to avoid any forms of debt monetization. By law, the ECB is not allowed to directly purchase the debt of governments or directly lend to them. The monetary financing prohibition (or the so-called “no bailout clause”) should encourage markets to sanction governments that engage in fiscally insane policies. This pressure was vital to preserve the value of the euro.

Considering that the ECB increasingly breaks with the EMU’s core principles, Europeans have reason to worry about their purchasing power.